GBP/USD reversed directions last week, shedding about 150 points. The pair closed the week slightly above the 1.66 line. This week’s highlight is Second Estimate GDP. Here is an outlook for the main events moving the pound, and an updated technical analysis for GBP/USD.

British CPI came in just under the 2.0% inflation and Claimant Count Change continues to impress. US releases hit some turbulence this week, as the Philly Fed Manufacturing Index and Existing Home Sales slipped badly in January.

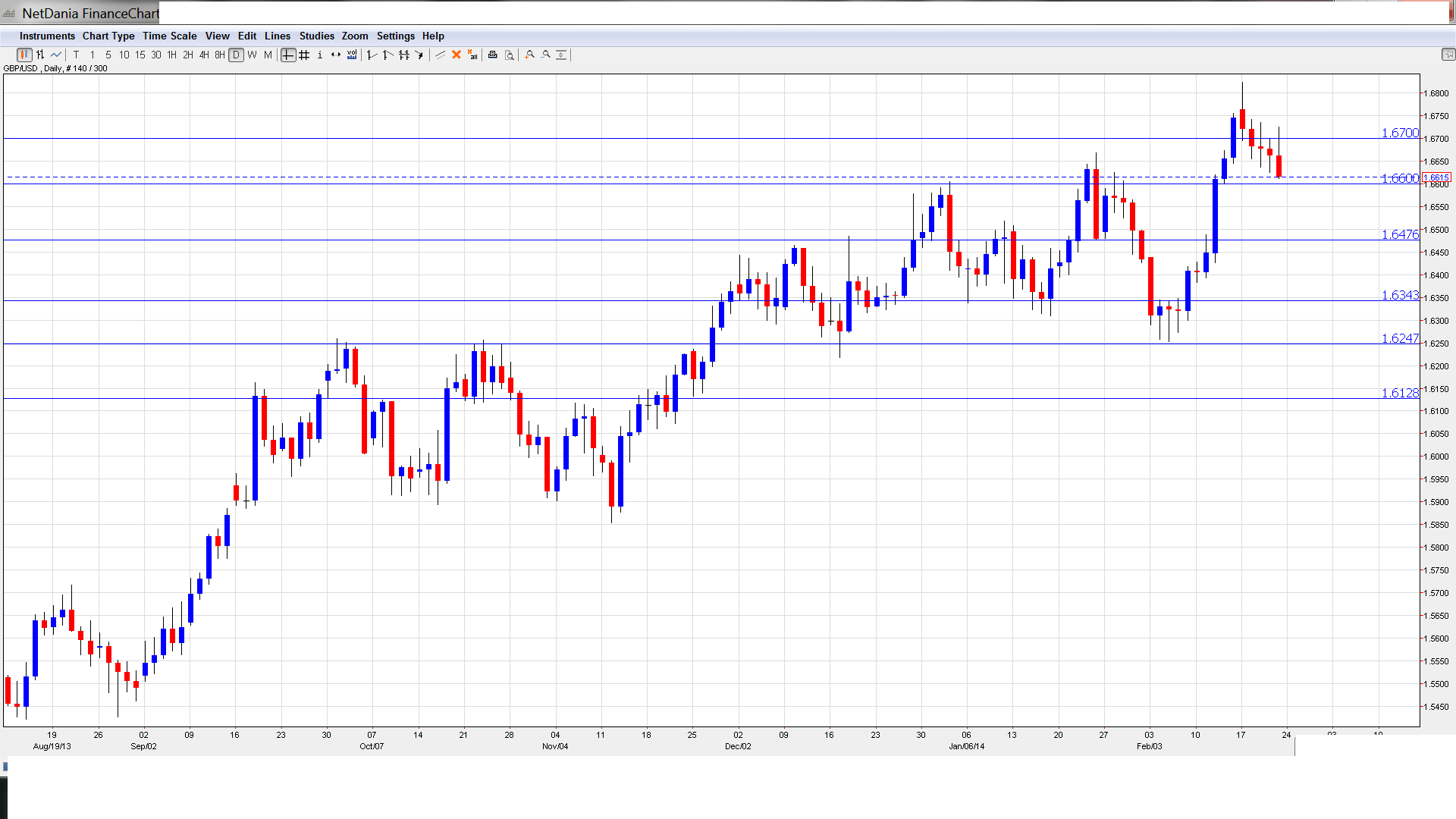

[do action=”autoupdate” tag=”GBPUSDUpdate”/]GBP/USD graph with support and resistance lines on it. Click to enlarge:

- Nationwide HPI: Tuesday, 25th-28th. This house inflation indicator posted a gain of 0.7% last month, matching the forecast. Little change is expected in the upcoming release, with the estimate standing of 0.6%.

- BBA Mortgage Approvals: Tuesday, 9:30. This indicator has been moving up steadily, hitting 46.5 thousand in December. The upswing is expected to continue, with a forecast of 47.9 thousand.

- CBI Realized Sales: Tuesday, 11:00. Realized Sales dropped sharply last month, coming in at 14 points, compared to 34 in the previous release. This was well of the estimate of 28 points. More of the same is predicted, with an estimate of 15 points.

- External BOE MPC Member Ben Broadbent Speaks: Wednesday, 9:25. Broadbent will deliver a speech in London. Analysts will be looking for hints as to the BOE’s plans regarding future monetary policy.

- Second Estimate GDP: Wednesday, 9:30. GDP is one of the most important economic indicators. It is released each quarter, magnifying the impact of each release. The indicator came in at 0.8% in Q3, and the estimate for Q4 stands at 0.7%.

- Preliminary Business Estimate: Wednesday, 9:30. This indicator is also released on a quarterly basis. The Q3 reading showed a respectable gain of 1.4%, but this fell well short of the estimate of 2.3%. The markets are expecting a strong improvement in Q4, with an estimate of 2.6%.

- GfK Consumer Confidence: Friday, 00:05. Despite the improving UK economy, Consumer Confidence continues to lag, and posted a disappointing reading of -7 points. The markets are expecting another weak reading, with the estimate standing at -6 points.

- BOE Governor Mark Carney Speaks: Friday, 15:30. Carney will speak at a financial symposium in Frankfurt. Remarks which are more hawkish than expected are bullish for the pound.

* All times are GMT

GBP/USD Technical Analysis

GBP/USD opened the week at 1.6763. The pair quickly hit a high of 1.6823, but it was all downhill after that. GBP/USD dropped all the way to 1.6611, closing the week at 1.6615.

Live chart of GBP/USD:

[do action=”tradingviews” pair=”GBPUSD” interval=”60″/]

Technical lines from top to bottom

We begin with resistance at 1.7383. This line marked the start of a rally by the pound back in April 2006, which climbed as high as the 2.11 level.

1.7180 served as a key support line in early 2006. The line has served in a resistance role since October 2008.

1.6990 is next. This line has been protecting the key 1.70 level and has held firm since October 2008.

1.6705 has switched back a resistance role. It is not a strong line and could face pressure if the pound pushes upwards.

The round number of 1.6600 is providing weak support as the pound dropped sharply last week.

1.6475 remains a strong support line. 1.6343 is the next support level.

1.6247 was a key resistance line in October and November 2012.

1.6125 is the final support line for now. This line has held steady since late November.

I am neutral on GBP/USD.

The pound hit some turbulence last week but still remains at high levels. Inflation is within the BOE’s 2.0% target, and there is increasing speculation that the Bank may have to consider a rate hike in the near future. Over in the US, recent releases have missed expectations, but market sentiment remains upbeat and QE tapering is expected to continue, which would be a vote of confidence from the Federal Reserve.

Further reading:

- For a broad view of all the week’s major events worldwide, read the USD outlook.

- For EUR/USD, check out the Euro to Dollar forecast.

- For the Japanese yen, read the USD/JPY forecast.

- For the Australian dollar (Aussie), check out the AUD to USD forecast.

- For USD/CAD (loonie), check out the Canadian dollar forecast.