One of the questions troubling EUR/USD traders is: does the price already reflect the anticipated ECB and Fed moves in December?

The team at Morgan Stanley weighs in:

Here is their view, courtesy of eFXnews:

While Morgan Stanley sees EUR/USD remaining under pressure and forecasts a move to parity next year, MS thinks that the risks of a pause in the near-term have increased.

“Expectations for ECBs easing in December are high, suggesting delivery risks. But we see any EURUSD recovery in the near-term as providing renewed selling opportunities although the anticipated move lower next year is likely to be at a slower pace than seen this year. EURUSD declined 25% from the mid-2014 high to the March low of this year. Downside progress since then has been altogether slower, even with the heightened expectation of greater policy divergence between the ECB and Fed.

While the USD uptrend has remained steady, we suggest that the EUR side of the equation has been far more erratic. Indeed, EUR on a trade weighted basis rebounded 10% April through August. While some EUR “catching-up” on the downside has been seen over the past couple of months as focus on potential further ECB action has intensified, the EUR still remains some way from its March/April trough in tradeweighted terms,” MS argues.

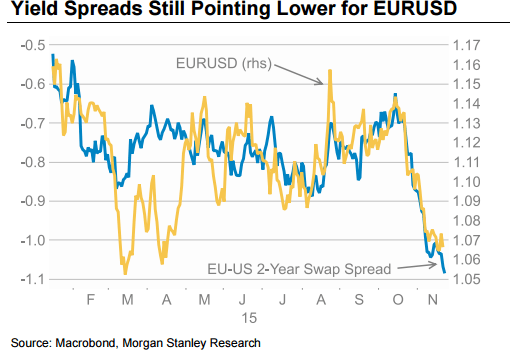

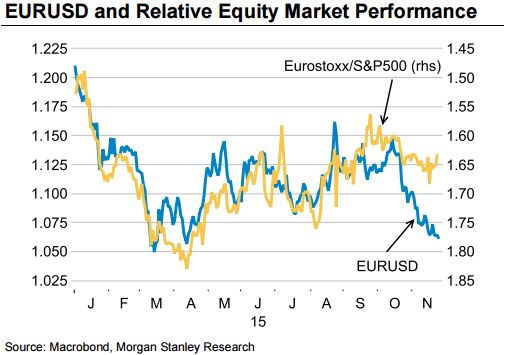

“We continue to see EURUSD remaining under pressure, but downside potential is likely to be driven move by the USD side of the equation, we believe. The overall pace of EUR decline compared to many market metrics has been lagging in our view. Even during periods where 2-yield differentials have been pointing sharply lower and equity markets have been stable, providing ideal conditions for a lower EURUSD, we would suggest the downtrend has become more reluctant than these indicators would have implied. EUR bearish positioning has been building, but is not extreme, suggesting further downside potential.

Hence, MS thinks that other factors are likely constraining EUR downside.

“Indeed, the incentive for additional EUR positioning may be lacking currently. The prospect of further easing is fully priced into interest rate markets, we believe. While Draghi’s highlighting of the potential for further ECB easing has had a significant “announcement effect” on the EUR, triggering the recent decline, to maintain or extend downward momentum the ECB would have to produce a further negative surprise. This was previously achieved by the ECB “over-delivering” on easing measures. While market expectations for easing measures were met and even exceeded earlier in the year, it may be more difficult for the ECB to repeat the market impact this time,” MS clarifies.

“For the EUR to move lower there will have to be an incentive to use the EUR as a funding currency. Certainly a further cut in the deposit rate as anticipated would help to fuel renewed enthusiasm for investors to fund in EUR. However, this requires a risk positive environment to be maintained globally. Increased global asset market volatility, potentially developing via the anticipated Fed hiking in December, could produce a more challenging investment environment, discouraging the use of the EUR for funding purposes,” MS argues.

“However, hedging activity is still likely to be an important source of EUR weakness. If further ECB easing and positive European growth surprises result in EMU asset market outperformance, then currency hedging of European assets by foreign investors could still exert downward pressure on the EUR. Hence, while we see the EURUSD decline continuing, it may not be as rapid as suggested by the Europe-US policy divergence and the EU-US yield spread. Indeed, a more cautious global risk picture could moderate the EUR decline,” MS adds.

MS runs a limit order to sell EUR/USD at 1.0880 with a stop at 1.0990, and a target at 1.0400.

For lots more FX trades from major banks, sign up to eFXplus

By signing up to eFXplus via the link above, you are directly supporting Forex Crunch.