The end of August approaches and as many traders take their vacations, central bankers including Fed Chair Janet Yellen, gather in Jackson Hole, Wyoming. Will she hint about a move in September? How will the dollar react? Here are opinions from 3 banks:

Here is their view, courtesy of eFXnews:

Jackson Hole: Don’t Expect Guidance On Timing Of Next Fed Hike – BofA Merrill

The focus will be on the future

On August 25-27, many chief economists and policymakers will be gathering in a serene mountainside resort in Jackson Hole, Wyoming, for the annual economic symposium. The topic is “Designing Resilient Monetary Policy Frameworks for the Future“, which will likely include lessons learned from the crisis and expectations for the future conduct of monetary policy. Although market participants will be on the lookout for clues about the timing of the next hike from the Fed, we think they will be difficult to find.

The latest star at the Fed

Fed Chair Yellen is scheduled to talk on Friday, the 26th (the timing of her speech has not yet been released). She is likely to spend time discussing the latest star at the Fed – R*, which is the equilibrium Fed funds rate. The short-term R*, which represents the equilibrium rate impacted by current headwinds, is believed to be about 0% in real terms. With the real Fed Funds rate running below, Yellen will likely argue that policy is still accommodative. We expect Yellen to reiterate the desire to keep policy simulative, given a “risk-management“ approach. There is asymmetry to a policy when so close to the zero bound – hiking too quickly could derail the economy, but going slowly will only mean a risk of having to play catch up. In this context, Yellen might argue that conditions are increasingly being met to normalize rates further before the end of the year, consistent with the latest communication from the FOMC. However, we do not expect guidance on the exact timing of the next hike.

The new regime

The more in-depth conversation is likely to be over how policymakers should calibrate policy going forward, assuming that R* is permanently lower and central bank balance sheets are permanently larger. This goes back to the topic of the conference – designing resilient frameworks. We think this will include debates about financial stability concerns, global central bank policy coordination, benefits/costs of negative rates and the effectiveness of forward guidance. We also suspect that there will be a conversation about inflation targeting, perhaps echoing some of the comments made by San Fran Fed Williams in his recent paper, where he made a case for considering price level targeting or nominal GDP targeting (NGDP) to allow an overshoot of inflation.

A shallow path

The acceptance of an R* that is permanently depressed and an emphasis on prudent risk management makes a case for policymakers to tread carefully toward the exit. In other words, central bankers should want to prolong this business cycle, with hopes that R* can head higher. From the Fed‘s perspective, this will involve balancing near-term data, which call for hikes (sub-5% unemployment rate), with longer-term concerns, which require patience. The result is a very shallow Fed hiking cycle. We think this will be a theme of the Jackson Hole Conference, which means we should not expect much insight into the timing of the next Fed rate hike.

Jackson Hole: How Will The USD React To Fed’s Yellen Speech? – Barclays

Market attention will be squarely focused on US Fed Chair Yellen’s speech at the Federal Reserve Bank of Kansas City’s annual Economic Policy Symposium in Jackson Hole. We believe she may use the opportunity to signal the FOMC’s growing confidence in the outlook for activity and inflation, given the rebound in labor markets since June and the solid rise in household spending in Q2. Although some FOMC members have lingering concerns about inflation, we expect Yellen to deliver a stronger signal about the likelihood of near-term rate hike and retain our view that the next increase will occur in September.

Given the low market expectations for a September or December Fed rate hike, a repricing at the front end of the rates curve in the event of a hawkish signal should drive a near-term rebound in the USD, accompanying a bear flattening of the yield curve.

However, the reaction in the USD over the medium term might be complicated by the Fed’s seemingly increased comfort with a modest overshoot of the dual mandate. Recent communications by current and former Fed officials suggest that the FOMC is coming around to the point of view that potential growth has fallen, the Phillips curve is flat, and the neutral rate of interest fell to very low levels. If the Fed wants to test whether monetary policy can bolster rates of productivity growth, it could let the domestic economy ‘run hot’ as it evaluates whether productivity is rebounding. If so, incoming data on inflation could become incrementally more important for understanding the Fed’s reaction function. Our rates strategy team thinks that a shift in the response function is likely to allay market concerns of lower-for-longer inflation and lead to a pickup in term premia, driving a steepening of the US yield curve.

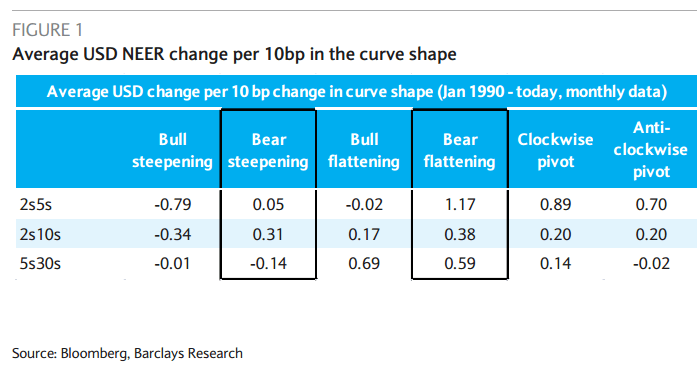

How will the USD react, given the shifting reaction of the Fed?

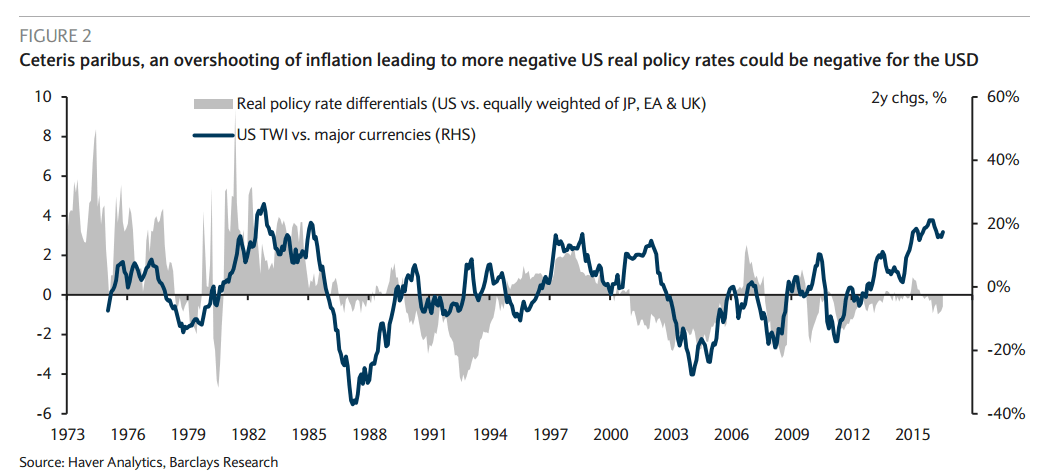

Figure 1 summarizes our findings of the dollar’s reaction to the different scenarios of the USD curve. Our results suggest that bear flattening of the yield curve is unambiguously positive for the USD, implying that a near-term USD rally is likely if Yellen indeed signals a short-term hike, as we expect. However, the durability of this bear-flattening rally in the USD is questionable, given the shifting reaction function of the Fed, in our view, unless supported by evidence of accelerating wage-price inflation accompanying a tightening of the labor market. The performance of the USD in a bear-steepening environment is however mixed historically, although a steepening of the 5s30s curve – a scenario that our rates strategy team expects to materialize – is mildly negative for the USD. But an overshoot of inflation about policy rates could lead to more negative real yields in the USD, which could lessen the relative appeal of USD assets, ceteris paribus (e.g., assuming real returns in trade partner countries stay stable).

Can The Fed Pull Off A ‘Dovish Hike’ In September? – Deutsche Bank

Has the Fed bought ‘optionality’ at the September meeting? If buying ‘optionality’ involves raising the market expectations of a rate rise to the point where the Fed can if desired raise rates without significantly surprising the market then at least based off fed fund futures, so far this has been a failure.

Can the Fed pull-off a relatively benign “dovish” rate hike in September?

Yes: i) The back-end of US yield curve will be well behaved which should be helpful for EM and equities; ii) USD/CNY and oil will create less instability; iii) the Fed can credibly tell a story of ‘hawkish in the short term, but dovish in the longer term.’

No: The market is unlikely to conclude this is a ‘two hikes and done’ rate cycle, and 2017 fed fund futures will surely sell-off significantly.

In the end, a rate hike that is so far from being priced in is bound to make some dent on risk/FX carry in the run-up to a tightening. The extent to which the market thinks that the Fed could follow with another hike in December, will have a significant impact on how FX and global asset markets absorb any September hike.

The long-term FOMC dots coming down will ameliorate some, but not all of the risk impact. Reigniting the high USD M/T view does not need anything like a normal Fed rate-hiking cycle implicit in the current Fed dots, but it does need the prospect of 1 handle on fed funds by the end of 2017.

We stand by a view that the first 5% gain in the broad USD TWI will not be too disruptive for risk in part because the full USD TWI is close to 5% off its January peak.

For lots more FX trades from major banks, sign up to eFXplus

By signing up to eFXplus via the link above, you are directly supporting Forex Crunch.