The talk about ECB tapering supported the common currency, but not for long. Here are two additional reasons why this could be just temporary:

Here is their view, courtesy of eFXnews:

ECB: ‘Too Early’ To Discuss Tapering – Danske

According to ECB officials the ECB is set to gradually wind down bond purchases once the QE programme ends.. The ECB officials said an informal consensus has built among policymakers that QE will be tapered once the programme ends. The tapering may be in steps of EUR10bn per month, which would be similar to the Fed’s tapering. An extension of the QE purchases beyond the current end date of March 2017 by EUR80bn per month was not excluded according to the sources.

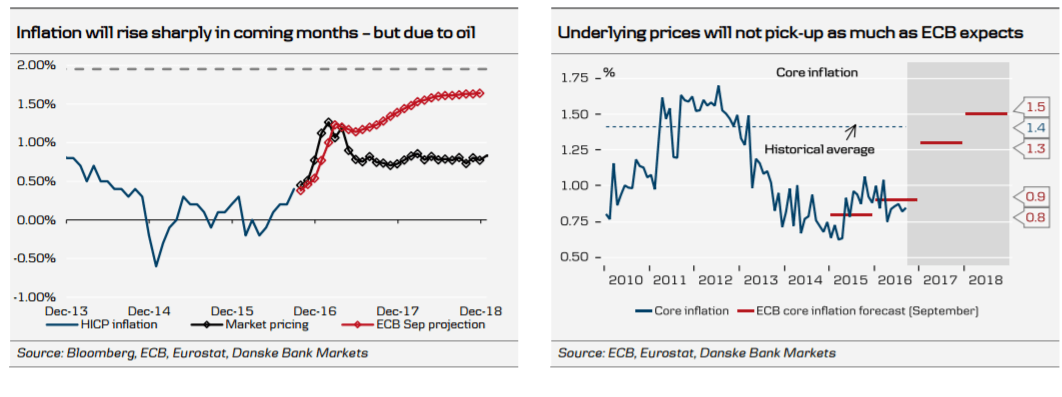

In our view, it is too early to discuss tapering and we expect the ECB to announce an extension of the QE purchases by six months at the meeting in December. Nevertheless, rising inflation could ignite speculation on whether ECB could do ‘less rather than more’. Continuing the QE programme is needed, in our view, although inflation is set to rise sharply in coming months.

The ECB expects inflation at 1.2% in Q1 17 but 0.7pp of the expected pick-up is driven by the oil price according to the ECB. The rise will thus not imply that the ECB has seen a ‘sustained adjustment in the path of inflation’ and hence end the QE programme. Instead, the ECB is likely to remain focused on low core inflation, which will not rise towards its historical average as the ECB expects next year.

For lots more FX trades from major banks, sign up to eFXplus

By signing up to eFXplus via the link above, you are directly supporting Forex Crunch.

ECB: ‘Reducing QE Is Not Tapering’ – Barclays

ECB’s macroeconomic outlook is optimistic in our view: The ECB forecasts euro area growth of 1.6% over 2017-18 and inflation to average 1.6% in 2018. In December 2016, the ECB could release updated forecasts for 2017-19, including average 2019 inflation at 1.8%. We find these forecasts somewhat optimistic (more on this below). We also believe these forecasts are likely to factor in considerable monetary policy accommodation, including QE monthly purchases through 2018. In other words, the inflation dynamics are not yet self-sustaining without additional QE.

If the ECB’s macro scenario is correct, we would expect a time extension of QE with a reduction in the pace of monthly purchases: We expect the ECB in December to announce changes to the technical parameters and an extension of QE beyond March 2017, although we see a good chance that the new, reduced pace of monthly purchases is not announced until March 2017. We believe that in 2017, the ECB will choose to purchase less than EUR80bn per month, but it will need to manage communication carefully to explain that reducing the amount of monthly purchases while maintaining it for an undefined but long period is not tapering. Firmer QE forward guidance could help to address market perceptions of tapering.

How much will the ECB buy? To achieve the ECB’s baseline forecast of 2018 average growth and inflation both at 1.6%, our model-based simulation (using a BVAR framework) suggests that monthly purchases would need to average c. EUR45bn per month until end-2018. Importantly, and consistent with these estimates, the ECB could start with average monthly purchases of EUR70-60bn in 2017 and reduce purchases gradually towards c.EUR20bn per month. As a reference, our estimate for net EGBs issuance per month is c.EUR17bn in 2018. Meanwhile, the Eurosystem already signalled that it will re-invest principal of maturing bonds at least until 2020.

We expect QE technical parameters to be relaxed before year-end: To complete its EUR80bn of monthly purchases until March 2017, the ECB would need to relax some of its self-imposed QE constraints no later than December. Specifically, we think (from more to less likely): 1) the removal of the yield floor is very likely; 2) the issue share limit is likely to be relaxed for non-CAC bonds; 3) the issue and issuer share limit could be relaxed for AAA-rated countries; 4) purchases of bonds beyond a 30y duration is unlikely; and 5) the capital key is unlikely to be removed, even if it would allow temporary deviations from the rule.

What if growth and inflation worsen? Under our base-case forecast for GDP growth of 1.0% in 2017 and downside inflation risk, we think the ECB should keep EUR80bn asset purchases for another six months before possibly reducing purchases later in 2017. Instead, if growth and inflation expectations were to fall sharply, we think scaling up QE would not be enough (even if it would be a likely first step). In our view, the ECB could need to become more “inventive” and extend credit and quantitative easing to other asset classes, possibly including bank loans. More importantly, in such a scenario, fiscal policy would be required to work together with monetary policy. Elevated political risks and lack of euro area policy coordination are likely to remain a serious handicap to pro-growth non-monetary policies, in our view.

For lots more FX trades from major banks, sign up to eFXplus

By signing up to eFXplus via the link above, you are directly supporting Forex Crunch.