- The USD/JPY extended its gains, riding higher on US yields.

- The beginning of the new month features the all-important Fed decision and Non-Farm Payrolls.

- The pair is risking entering into overbought territory after the rally.

Almost all about the yields

The last full week of April was dominated by rising US bond yields. The benchmark 10-year Treasury note topped the 3% level for the first time since 2011, and this made the US Dollar attractive across the board. Bond yields of other maturities also reached multi-year highs in the secondary market as well as in the primary one, with bond auctions resulting in unfavorable conditions for the Treasury.

The rise in yields is fueled by a growing sense that the Fed is eager to raise rates at a quick pace, following upbeat data and bullish comments from Fed officials. Also, the tax cuts and fiscal spending spree also have an impact. The government has extended funding needs.

The US GDP report came out at 2.3% annualized, slightly above 2.0% expected. However, the upbeat headline Durable Goods Orders on Thursday had already lifted real expectations. The reaction was relatively limited.

The Bank of Japan left the interest rate unchanged at -0.10% and maintained its bond-buying guidelines. They did, however, abandon the timeframe of Fiscal Year 2019 as the target for reaching the 2% inflation target. Governor Haruhiko Kuroda was busy explaining the change, but markets did not react.

Korea Summit: South Korea’s President Moon Jae-in met North Korean leader Kim Jong-un in a first meeting of this kind in 11 years. The leaders announced that denuclearization of the peninsula is a common goal. The progress towards peace in the Korean Peninsula is due to be followed by a meeting between Kim and US President Trump. The improved mood diminishes demand for the safe-have Japanse Yen.

Japanese PM Shinzo Abe remains embattled by a series of scandals that hurt his popularity. Rumors of a potential resignation and a snap election have circulated but have been denied.

US events: Fed decision and a data-packed buildup to the NFP

The week begins with the Fed’s favorite inflation figure: the Core PCE Price Index for March. The CPI report for March showed a jump in core inflation from 1.8% YoY to 2.1% YoY. The Core PCE will likely advance as well, rising from 1.6% seen in February. However, it is unlikely to hit the Fed’s target of 2%. The publication also includes Personal Spending and Personal Income which are both expected to rise by 0.4% MoM. The Chicago Purchasing Managers’ Index and Pending Home Sales conclude an unusually busy Monday.

Tuesday features the ISM Manufacturing PMI, the first hint towards the Non-Farm Payrolls report on Friday. A slight drop from the highs of 59.3 points is on the cards.

Another hint towards the official NFP comes on Wednesday from the ADP Non-Farm Payrolls. The private sector report is expected to show a more moderate rise in April after a whopping gain of 241,000 in March. However, markets’ attention will be on a more significant event later in the day: the Fed decision.

The Federal Reserve convenes on Wednesday for a meeting that does not consist of new forecasts nor a press conference. Fed Chair Jerome Powell and his colleagues are not expected to raise interest points at this juncture. However, they may cement a rate hike in June, which is priced in by markets. Comments about rising inflation and the recent GDP report will be eyed. .Recent commentary has been upbeat, and the tone is likely to remain positive, conveying a confident message toward the June hike.

A significant bulk of data awaits traders on Thursday: the politically-sensitive Trade Balance report will likely show a vast trade deficit. Unit Labor Costs serves as another indicator of wage inflation Factory Orders are expected to show an ongoing expansion. The most critical data point is the ISM Non-Manufacturing PMI for April. The services sector, the largest in the US, is projected to continue enjoying robust growth with a similar figure to the 58.8 points seen in March.

And the best is kept for last. The Non-Farm Payrolls report for April is expected to show a gain of 198,000 jobs, a bounce back to the average after a disappointing rise of only 103,000 positions in March. The focus remains on wages. Month over month, an increase of 0.2% is expected to follow last month’s 0.3% gain. Yet year over year, markets are bracing for stability with a repeat of the 2.7% level. Any move toward 3% wage growth may send the US Dollar higher while a slip back to the previous stubborn average of 2.5% may weigh on the greenback.

All in all, this is a very eventful week.

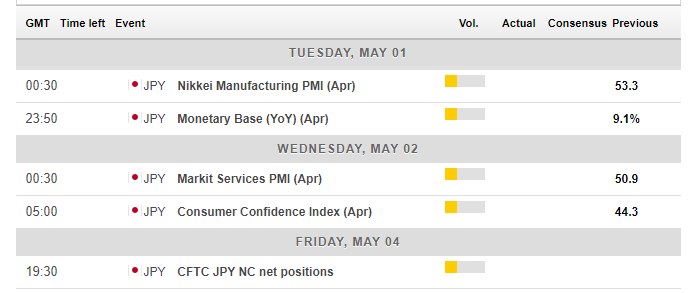

Here are the top US events as they appear on the forex calendar:

Japan: Politics, not economics

The economic calendar is light in Japan. The changes in the Monetary Base may be of interest after the BOJ decision but is unlikely to be a significant market mover. However, politics, internal and external, will likely play a role in the Yen’s movements.

The embattled Abe will continue facing pressures from his own party as approval ratings remain low. So far, no other nominee as emerged and the opposition is not a formidable force. Abe enacted massive fiscal stimulus and promoted even more massive monetary stimulus that weakened the Yen. More signs of an early departure may push the Yen higher.

The fallout from the Korean Summit will continue reverberating in the markets. Optimism about the North Korea’s abandoning of the nuclear arms may weigh on the Yen. This may wait for the Trump-Kim Summit which will take place in late May or early June.

Here are the events lined up in Japan:

USD/JPY Technical Analysis: Did it go too far?

The fast move to the upside enjoys strong Momentum, but the RSI is already around 70, indicating overbought conditions. This may point to a pullback.

Looking up, ¥109.80 was a stubborn high in early February and late January. Above the round number, the significant 200-day Simple Moving Average meets the price at ¥110.30. Even higher, the mid-January high of ¥111.50 looms above.

Looking down, the round number of ¥109.00 should provide some support. Lower, ¥108.30 served as support early in the year. It is followed by the double-top of ¥107.90, last visited in early April is the next line of support.

-636604318377952754.png)

What’s next for USD/JPY?

The US Dollar has all the right reasons to rise, but it may have gone too far, too fast. The one-sided rally may stall before the pair resumes its gains. Extraordinary US data will be needed to see a similar rally this week.

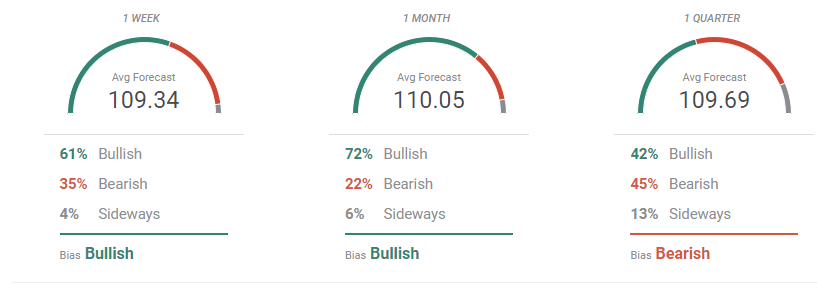

The FXStreet FX Poll shows a bullish tendency in the near and medium terms. The views for the medium term are in line with the ones expressed here, but in the near term, there is a split.

More: Trading forex in Europe? This is what the new ESMA regulations mean for you.