- DXY gains further traction and surpasses 93.00 on Tuesday.

- Higher US yields underpins the rally in the greenback.

- US housing data, Consumer Confidence, Fedspeak next on tap.

The greenback pushes higher and lifts the US Dollar Index (DXY) to new yearly tops in the area above 93.00 the figure.

US Dollar Index looks to data, yields

The upside momentum surrounding the index remains well and sound and now trades in levels last seen back in early November 2020 beyond the 93.00 hurdle.

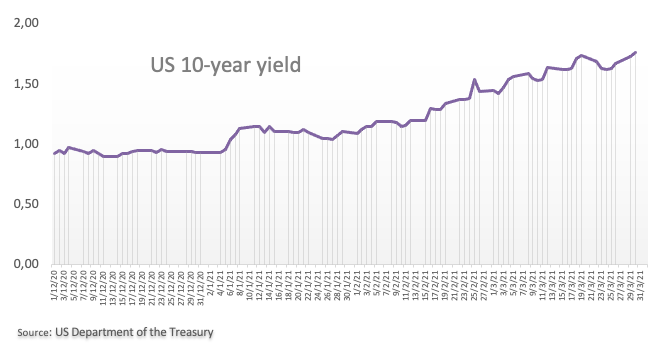

The rally remains well supported by rising yields in the US bond markets. Indeed, yields of the key 10-year note advance to fresh highs above 1.75%, area last visited in January 2020.

Biden’s plan to boost the infrastructure adds to the recently passed $1.9 trillion fiscal stimulus bill, all morphing into further speculations of higher inflation in the coming months. This, plus the US economy outperformance (vs. its overseas peers) narrative bolster further the current constructive stance in the buck.

Later in the US data space, FHFA’s House Price Index is due along with the S&P/Case-Shiller Index and the Conference Board’s Consumer Confidence gauge for the month of March.

In addition, FOMC’s R.Quarles (permanent voter, centrist), Atlanta Fed R.Bostic (voter, centrist) and Mew York Fed J.Williams (permanent voter, centrist) are all due to speak throughout the session.

What to look for around USD

The upside momentum in the dollar looks well and sound and the index already trade above 93.00 yardstick, or new YTD tops. Supporting this idea, the recent breakout of the 200-day SMA seems to bolster the now constructive view on the buck, at least in the near-term. In addition, the recently approved fiscal stimulus package adds to the ongoing outperformance of the US economy narrative as well as the investors’ perception of higher inflation in the next months, all morphing into extra oxygen for the buck. However, the mega-accommodative stance from the Fed (until “substantial further progress” in inflation and employment is made) and hopes of a strong global economic recovery (now postponed to later in the year) remain a source of support for the risk complex and carry the potential to curtail the upside momentum in the dollar in the longer run.

Key events in the US this week: CB’s Consumer Confidence (Tuesday) – ADP Report, President Biden’s speech (Wednesday) – Initial Claims, ISM Manufacturing (Thursday) – Nonfarm Payrolls (Friday).

Eminent issues on the back boiler: Biden’s infrastructure bill worth around $3 trillion. US-China trade conflict under the Biden’s administration. Tapering speculation vs. economic recovery. US real interest rates vs. Europe. Could US fiscal stimulus lead to overheating? Future of the Republican party post-Trump acquittal.

US Dollar Index relevant levels

At the moment, the index is gaining 0.10% at 93.04 and a breakout of 93.07 (2021 high Mar.30) would expose 94.00 (round level) and finally 94.30 (monthly high Nov.4). On the downside, the next support lines up at 92.52 (200-day SMA) followed by 91.30 (weekly low Mar.18) and then 91.16 (50-day SMA).