- DXY adds to Friday’s gains above the 92.00 level.

- US 10-year yields trade on the defensive below 1.70%.

- Powell, Fedspeak, housing data next in the US docket.

The greenback, when tracked by the US Dollar Index (DXY), starts the week on a positive footing and looks to extend the recovery further north of the 92.00 level.

US Dollar Index focused on yields, data, Powell

The index advances for the third consecutive session and looks to leave behind the 92.00 barrier on a sustainable basis and therefore targets the YTD highs in the 92.50 region in the near-term.

The buying interest in the dollar remains anything but abated for yet another session, always on the back of the firm performance of US yields, while the recent announcement by the Fed on the supplementary leverage ratio (SLR) has also collaborated with the upside.

In the broader scenario, the US continues to outperform its G10 peers when comes to the vaccine rollout (mainly vs. Europe) and the prospects of economic recovery in the post-pandemic era, all exacerbating the resilience around the buck.

Later in the US calendar, the Chicago Fed National Activity Index is due seconded by Existing Home Sales, all for the month of February.

In addition, Chairman Powell will speak on “How Can Central Banks Innovate in the Digital Age” seconded by the speech by FOMC’s R.Quarles, while FOMC’s M.Bowman will speak on “The Economic Outlook and Prospects for Small Business”.

What to look for around USD

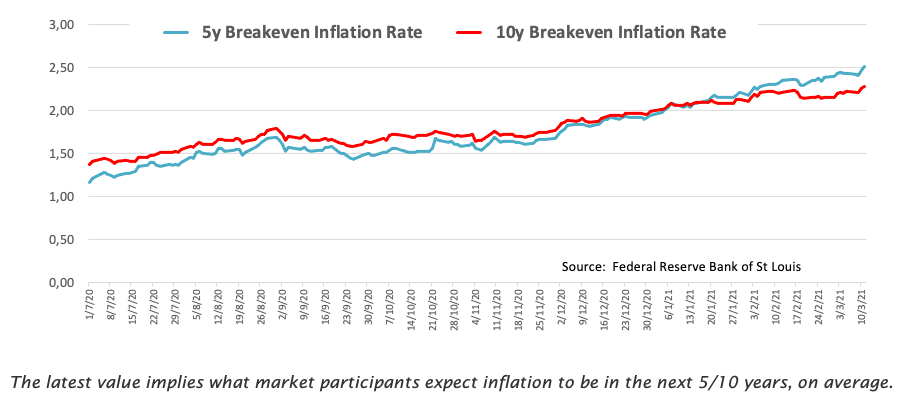

The greenback manages well to keep business in the upper end of the recent trading range and eyes a potential visit to the yearly highs around 92.50 in the not-so-distant future. The recently approved fiscal stimulus package adds to the ongoing outperformance of the US economy narrative as well as the investors’ perception of higher inflation in the next months, all morphing into extra oxygen for the buck. However, the mega-accommodative stance from the Fed (until “substantial further progress” in inflation and employment is made) and hopes of a strong global economic recovery remain an omnipresent source of support for the risk complex and are seeing limiting the dollar’s upside for the time being.

Key events in the US this week: Chairman Powell testimonies before the House of Representatives and the Senate on Tuesday and Wednesday, respectively – Flash Markit’s PMIs, Durable Goods Orders (Wednesday) – Final Q4 GDP, Initial Claims (Thursday) – February’s PCE, Personal Income/Spending, final U-Mich Index (Friday).

Eminent issues on the back boiler: US-China trade conflict under the Biden’s administration. Tapering speculation vs. economic recovery. US real interest rates vs. Europe. Could US fiscal stimulus lead to overheating? Future of the Republican party post-Trump acquittal.

US Dollar Index relevant levels

At the moment, the index is gaining 0.10% at 92.01 and a breakout of 92.50 (2021 high Mar.9) would expose 92.65 (200-day SMA) and finally 94.30 (monthly high Nov.4). On the other hand, the next support is located at 91.30 (weekly low Mar.18) seconded by 91.05 (high Feb.17) and then 90.90 (50-day SMA).