- DXY leaves behind Wednesday’s drop and regains the 93.30 area.

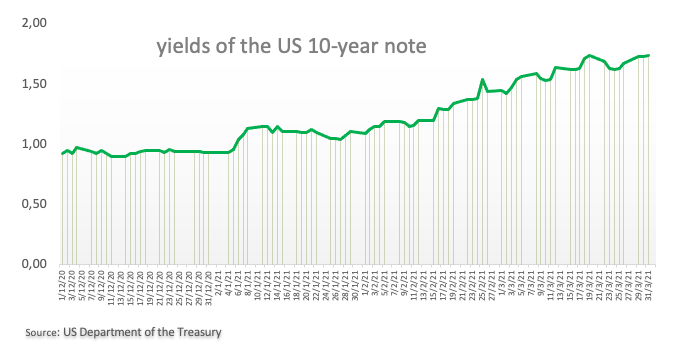

- US yields recede a tad but remain above 1.70%.

- Weekly Claims, ISM Manufacturing, final PMIs next on tap.

The greenback, when measured by US Dollar Index (DXY), reclaims the upper hand and advances to the 93.30 region ahead of the opening bell in the Old Continent on Maundy Thursday.

US Dollar Index focused on data

The index returns to the positive territory following Wednesday’s inconclusive price action, always above the key 93.00 barrier.

Month/quarter-end flows, steady US yields and a supportive tone in the risk universe put the index under some downside pressure soon after hitting new 2021 highs around 93.40 on Wednesday.

In the meantime, the index remains well supported by firm hopes of a strong US economic recovery vs. its G10 peers helped by a solid pace of the vaccination campaign and amidst rising fiscal stimulus and yields trading in multi-month highs.

Later in the US data space, the focus of attention is expected to gyrate around the ISM Manufacturing for the month of March, the final Manufacturing PMI for the same period and usual weekly Claims. In addition, Philly Fed P.Harker (2023 voter, hawkish) is due to speak.

What to look for around USD

The upside momentum in the dollar looks well and sound for the time being. Supporting this idea, the recent breakout of the 200-day SMA seems to bolster the now constructive view on the buck, at least in the near-term. In addition, the recently approved fiscal stimulus package adds to the ongoing outperformance of the US economy narrative as well as the investors’ perception of higher inflation in the next months, all morphing into extra oxygen for the buck. However, the mega-accommodative stance from the Fed (until “substantial further progress” in inflation and employment is made) and hopes of a strong global economic recovery (now postponed to later in the year) remain a source of support for the risk complex and carry the potential to curtail the upside momentum in the dollar in the longer run.

Key events in the US this week: Initial Claims, ISM Manufacturing (Thursday) – Nonfarm Payrolls (Friday).

Eminent issues on the back boiler: Biden’s new stimulus bill worth around $3 trillion. US-China trade conflict under the Biden’s administration. Tapering speculation vs. economic recovery. US real interest rates vs. Europe. Could US fiscal stimulus lead to overheating? Future of the Republican party post-Trump acquittal.

US Dollar Index relevant levels

At the moment, the index is up 0.10% at 93.32 and a break above 93.43 (2021 high Mar.31) would expose 94.00 (round level) and finally 94.30 (monthly high Nov.4). On the flip side, the next support emerges at 92.48 (200-day SMA) followed by 91.30 (weekly low Mar.18) and then 91.29 (50-day SMA).