Recent figures in the US haven’t been too bad. Is the greenback making a big comeback? The team at Credit Agricole examines:

Here is their view, courtesy of eFXnews:

The USD-decoupling trade is staging a return on the back of improving US data, the abatement of global risk aversion and the growing resilience of the US domestic demand-driven recovery to persistent global headwinds and future Fed rate hikes.

The USD should regain more ground because better US data and easing global financial conditions should help the Fed keep its constructive economic outlook, and signal further gradual tightening.

USD should do well against EUR and JPY as flows related to the policy divergence trade continue with Eurozone and Japanese excess savings heading to the US, and EUR-funding replacing pricey USD-funding.

…We have argued in the past that our bullish case for USD is partly based on the expectations that FX flows triggered by the persistent policy divergence between the Fed and other major central banks, like the BoJ and ECB, should continue to support the USD against EUR and JPY. We further argued that these flows will likely continue even if policy divergence does not intensify from here but so long as the Fed remains on course to hike gradually, and the ECB and the BoJ maintain their highly accommodative stance:

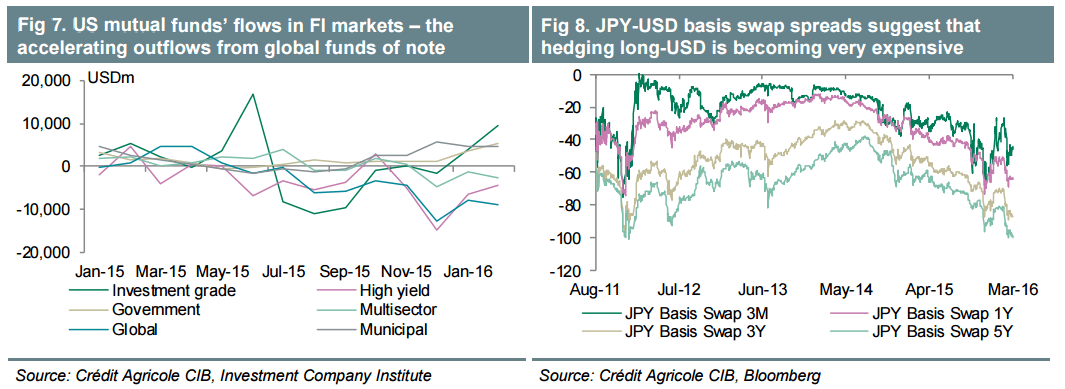

1. Investor outflows from the FI markets of Europe and Japan, where negative bond yields make EGBs and JGBs less attractive compared to USTs. As shown in Figure 7, the US mutual funds flow data has been pointing at persistent outflows from global portfolios in recent months. The outflow could intensify as further easing by the ECB and the BoJ drives yields deeper below zero, and bull flattens domestic bond curves.

2. We also expect that policy easing by the BoJ should continue to drive excess savings out of Japan. This is consistent with the latest flow data from the Japanese MoF, which suggested that domestic investors continued to buy assets abroad despite the recent bout of risk aversion. As we argued recently data seems to suggest that that Japanese investors are exploiting the latest JPY-appreciation to expand their holdings of foreign assets and even grow their FX exposure. With the outflow of excess savings out of Japan expected to continue, we further note that a growing portion of that flow could remain unhedged given the growing costs associated with long-USD exposure. Indeed, as shown in Figure 8, the USD-JPY basis swap spread has turned significantly negative in recent months. A growing share of unhedged outflows from Japan and into the US should keep USD/JPY on an uptrend from here.

3. Last but not least, we expect foreign demand for EUR-funding to continue as international borrowers exploit the more attractive funding conditions in Eurozone FI markets at present. In that, they will continue to swap expensive USD-debt for cheaper EUR-debt, selling EUR/USD in the process. This flow could remain the main channel for recycling the Eurozone’s sizeable excess savings in the coming quarters and keep downside pressure on the currency pair. Importantly, given that it is foreign borrowers who issue EURdenominated debt, and subsequently sell the proceeds to buy USD and repay USD-denominated debt, this flow need not go into reverse during bouts of risk aversion as in the case of other EUR-funded carry trades. Because of that the correlation between EUR and risk aversion should remain much weaker than in the case of JPY.

For lots more FX trades from major banks, sign up to eFXplus

By signing up to eFXplus via the link above, you are directly supporting Forex Crunch.