Here are two previews towards the decision of the Bank of Canada on Wednesday. Is there room for a dovish surprise?

Here is their view, courtesy of eFXnews:

Room For A Dovish BoC Surprise Next Week; Risk-Reward Favors Short CAD – BofA Merrill

The Bank of Canada (BoC) held rates at 0.50% in January, despite expectations for an ease, preferring to see the details and impact of the coming fiscal stimulus before acting. Additionally, the sharp decline in the C$ into the meeting likely made them reticent to further exacerbate the price action with an ease.

With the budget to be released on March 22nd and Canadian data generally surprising on the upside since midJanuary, we see the BoC remaining on hold next week. With only 1bp of a cut priced in the OIS market, an on-hold, steady state outcome would likely elicit little market reaction. However, the substantial re-pricing of BoC expectations since end-January where the market is only pricing a 20% chance of a cut through September 2016 leaves asymmetric risks for the C$.

We certainly don’t expect the BoC to cut, but risks around the economy remain tilted to the downside, particularly amidst a weak global backdrop.

Indeed, despite the C$ significant depreciation, exports subtracted 0.2 pct points from Q4 GDP. The upside surprise in the print was largely driven by a collapse in imports, certainly not a positive forward-looking sign about capital investment and consumption. Additionally, the over 8% appreciation of the C$ off its mid-January lows could raise concerns about an unwanted tightening of financial conditions, particularly as the BoC has yet to see a rebalancing towards non-energy exports as it has long expected.

Therefore, risk/reward favors short CAD positions into the meeting. A dovish tone will challenge the optimistic OIS path, relative to the residual economic risks still facing an economy dealing with the oil shock.

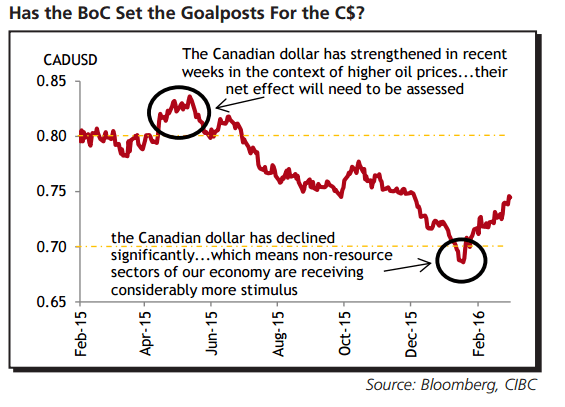

Has The BoC Set The Goalposts For The CAD? – CIBC

The Bank of Canada doesn’t target the exchange rate. But it has in the past year set down some fairly significant goalposts. At its last meeting, in January, a key reason why Governor Poloz didn’t cut was how far and fast the currency had weakened.

However, last Spring, Poloz also expressed some concern that, in rising above 80 cents, the Canadian dollar had strengthened too much. The C$ currently stands in the middle of the 70-80 goalposts.

However, if it continues to strengthen as oil prices recover Governor Poloz may feel the need to verbally push back and keep the loonie on the weak side of fair value, making sure that the encouraging signs we have seen recently from non-energy exports continue.

For lots more FX trades from major banks, sign up to eFXplus

By signing up to eFXplus via the link above, you are directly supporting Forex Crunch.