The Canadian dollar seems to be on a roll but perhaps it’s a bit off. Here is the view from Nomura:

Here is their view, courtesy of eFXnews:

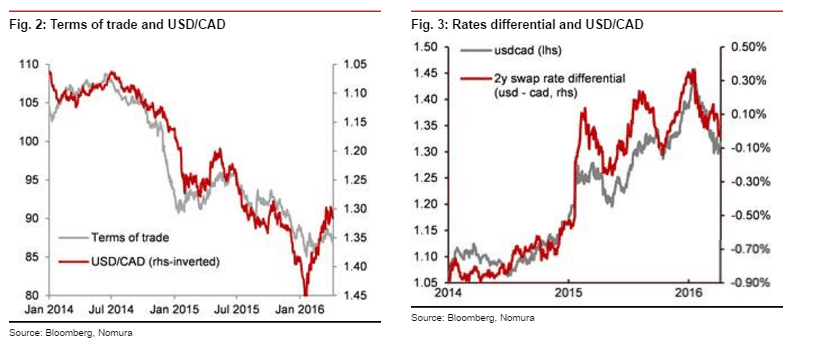

Since reaching a low of about $26 in mid-February, oil prices (WTI) have rebounded sharply to more than $41 by the second half of March. This was the result of a reduction in short positions in oil and of expectations of an accord between oil producers to freeze output. However, oil prices have declined in recent weeks, as it has become clear that a production freeze would only happen if Iran were to participate. Nevertheless, it remains clear that USD/CAD is likely too low considering the terms of trade.

We believe that an agreement on oil production is unlikely and that will prove negative for oil prices in the short term, pushing oil prices below $35. Nevertheless, we continue to expect oil prices to recover gradually in the second half of the year and hover around $45 over the period, possibly reaching $50, lending some support to CAD in H2. But it is very likely that oil prices will remain volatile and subject to positioning over the coming months.

The recent economic data in Canada have been relatively supportive. The manufacturing sector is showing a rebound in activity, led by the motor vehicle sectors, and this has translated into an improvement in non-energy exports, supported by the weaker CAD, as shown in the latest monthly GDP. It remains to be seen how much momentum there is, especially given the recent weakness in the trade data, but it reduces the need for further monetary policy easing, especially given the stimulus coming from the fiscal side.

While we believe that the stimulus from fiscal policy is likely to be smaller than the government estimates, we believe that it will be enough to keep the Bank of Canada on hold at 0.5% for the rest of the year. If we are correct, this means that the rates differential is likely to be mostly driven by US rates rather than by Canadian rates. With the Fed still expected to hike twice this year, this should provide support for USD/CAD.

With the sharp increase in commodity prices in recent weeks and the change in the rates differential since our last update, we estimate that fair value for USD/CAD has declined to 1.38. This suggests that USD/CAD could be currently undervalued by slightly more than 5%.

With this in mind, we believe that USD/CAD should move higher in Q2 and Q3, reaching 1.38, as the currency is expected to converge gradually to its fair value, oil prices are unlikely to pick up in the short term and higher rates in the US should support USD. Going into the second half of the year, we expect oil prices to recover somewhat which should push USD/CAD slightly lower.

*Nomura’s forecasts last updated on eFXplus on 4/6.

For lots more FX trades from major banks, sign up to eFXplus

By signing up to eFXplus via the link above, you are directly supporting Forex Crunch.