EUR/USD has posted modest gains on Wednesday, bolstered by positive PMIs out of Germany, France and the Eurozone. The pair is above the 1.32 level in the European session. After a light load on Tuesday, the markets will be busy plowing through a large number of releases out of the Eurozone and the US on Wednesday. Today’s major event is US New Home Sales. Speculation about QE tapering in September is increasing after a new survey shows more confidence among economists that the Fed will take action.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

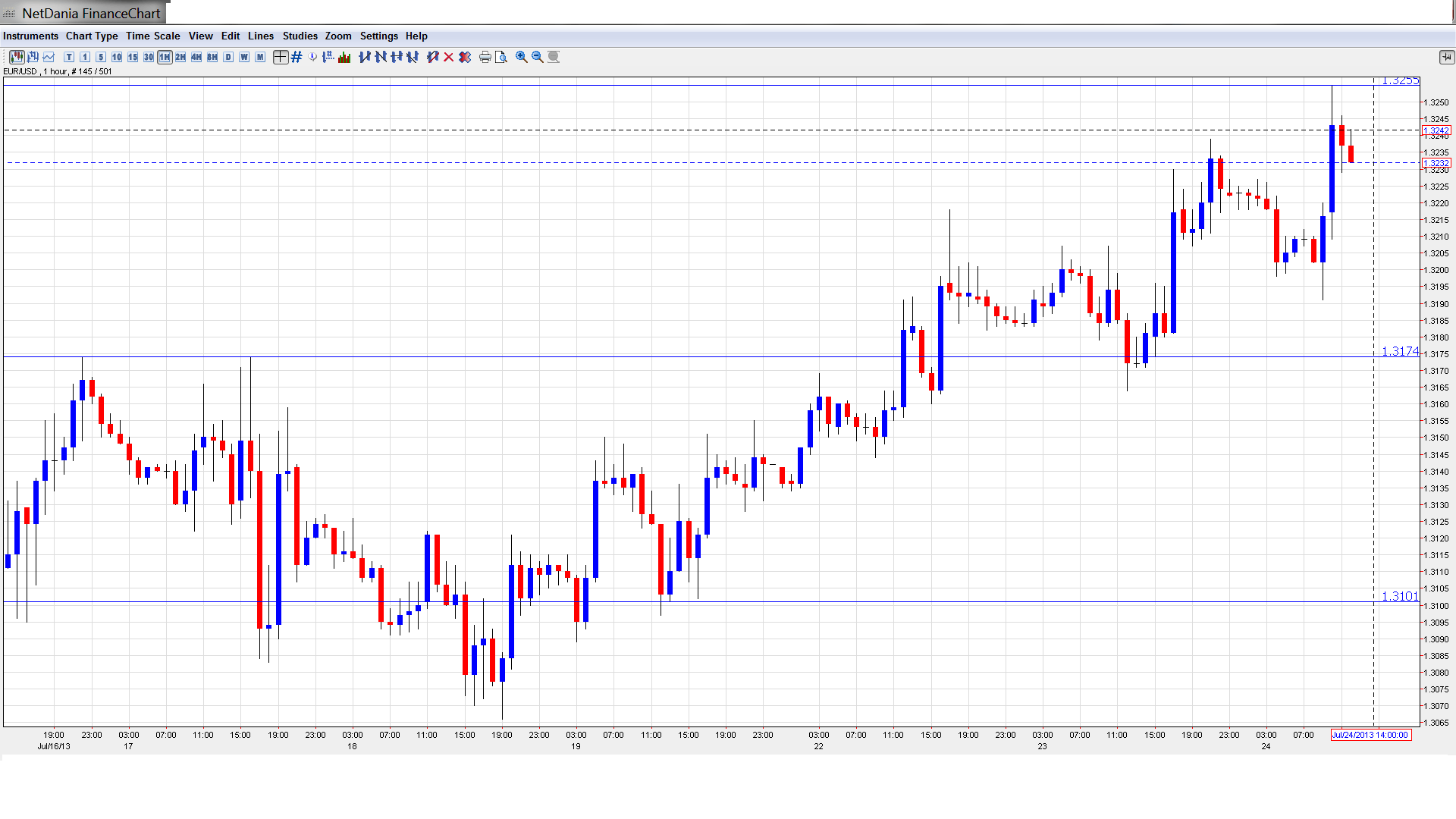

EUR/USD Technical

- Asian session: Euro/dollar edged lower, dipping below the 1.32 line late in the session. The pair has bounced back in the European session, crossing back into 1.32 territory.

Current range: 1.3175 to 1.3255.

Further levels in both directions:

- Below: 1.3175, 1.31, 1.3050, 1.30, 1.2940, 1.2890 and 1.2840.

- Above: 1.3255, 1.3350 and 1.34.

- On the downside, 1.31 is providing significant support.

- The pair has pushed past 1.32 and faces resistance at 1.3255.

EUR/USD Fundamentals

- 7:00 French Flash Manufacturing PMI, exp. 48.9, actual 49.8 points.

- 7:00 French Flash Services PMI, exp. 47.7, actual 48.3 points.

- 7:30 German Flash Manufacturing PMI, exp. 49.3, actual 50.3 points.

- 7:30 German Flash Services PMI, exp. 50.9, actual 52.5 points.

- 8:00 Eurozone Flash Manufacturing PMI, exp. 49.1, actual 50.1 points.

- 8:00 Eurozone Flash Services PMI, exp. 48.9, actual 49.6 points.

- 8:00 Italian Retail Sales, exp. 0.4%, actual 0.1%.

- 13:00 US Flash Manufacturing PMI, exp. 52.5 points.

- 14:00 US New Home Sales, exp. 482K.

- 14:30 US Crude Oil Inventories, exp. -2.5M.

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Strong Euro PMIs bolster euro: There was good news out of the Eurozone early on Tuesday, as European PMIs looked strong. Eurozone, German and French Services and Manufacturing PMIs all beat their estimates, pointing to improvement in the services and manufacturing sectors. The markets were especially pleased with the German data, as both PMIs came in above the 50 level, which is the separator between expansion and contraction. Despite showing improvement, both French PMIs still remain below 50, which has been the case throughout 2013. Eurozone PMIs were a mix, with the Manufacturing PMI climbing to 50.1 points, while Services PMI moves closer to expansion, rising to 49.6 points. If additional services and manufacturing indicators out of the Eurozone follow pace and point upwards, the euro could continue to post gains against the dollar.

- Will Fed press tapering trigger in September?: QE tapering remains a hot topic, and it is looking increasingly likely that the Fed will take some action before the end of the year. A new survey of economists show that half of them see tapering in September, from a scale of $85 to $65 billion. This is a rise compared to previous surveys. Is a QE downsize already priced in by the markets? There is a Fed decision at the end of July, but expectations are low that we will see any changes to QE. Fed chair Bernard Bernanke testified before Congress and did not really add anything new. Bernanke said that monetary policy would remain accommodative, and that the pace of bond buys is “not on a preset course“. This rather vague statement leaves the Fed plenty of wiggle room to scale down QE when it chooses to do so. Bernanke reiterated that any decision to taper QE would depend on economic conditions. He noted that present unemployment levels (7.6%) were “well above” normal levels, and shied away from presenting any time deadlines for scaling down QE. So the markets were left with the message that any tapering will be delayed until the recovery deepens and unemployment falls. Job figures remain left, right and center for markets.

- Concerns over US housing sector: After weak building permits and housing starts out of the US, existing home sales disappointed with a drop to 5.08 million, and this pushed the dollar lower across the board. The Fed was happy with the recovery of the housing sector, which is partially attributed to its policies. The markets will be hoping for better data out of New Home Sales later on Wednesday. Both Existing and New Home Sales are market-movers, due to the wide economic effects of building or purchasing a house.

- Spanish government tries to contain political scandal: The scandal surrounding the Spanish ruling party refuses to die. It has reached all the way to Prime Minister Mariano Rajoy, with claims that he accepted illegal payments when he was a minister in a previous government. There have been calls for Rajoy’s resignation, but analysts have noted that top level resignations by political leaders is rare in Spain. Rajoy, who has denied any wrongdoing, has a strong majority in parliament and is not expected to step down but the political crisis is still present. Spain had to tap its social security reserve fund in order to pay pensions and house prices continue falling. Nevertheless, Spain’s finance minister de Guindos declared that Spain’s economy is improving “beyond seasonal effects”.

- German optimism buoyed by strong PMI data: The German Bundesbank assessed that the euro-zone’s locomotive enjoyed strong growth in Q2, but is set to slow down in Q3. Tuesday’s PMI numbers were a breath of fresh air, as recent economic data has been mixed. Manufacturing PMI jumped from 48.7 to 50.3 points, and Services PMI kept pace, improving from 51.3 to 52.5 points. Both indexes were well above their estimates. Germany is facing elections on September 22nd, and the economy promises to be an important issue in the election campaign.

- Recent technical analysis articles: EUR/USD set to extend gains