Idea of the Day

Markets have reacted to the deal reached over the weekend designed to curtail Iran’s nuclear ambitions. This had been a source of tension for many years and has impacted safe haven assets and oil on an on-going basis. Although there are several hurdles still to climb, including a sceptical US Congress, the deal has already seen an initial impact in markets. In FX, the yen has further weakened, underlining the reduced safe haven appeal of the Japanese currency, with gold weaker also. Oil prices have also moved lower in response, on the prospect of the lifting of sanctions.

At present, the cap on limited oil sales to select countries remains in place, so on face value the move looks a little knee-jerk. Nevertheless, if sustained it would put further downward pressure on inflation, with low energy prices already responsible for a proportion of the lower inflation rates being seen in both then US and Europe. So while welcomed politically, it could be another headache for central bankers in Europe, pushing inflation lower and pressuring more policy measures from the ECB.

Data/Event Risks

USD: Just pending home sales data in the US today, which are seen recovering 1% from the 5.6% fall seen in September, but data generally not a big deal for the dollar.

Latest FX News

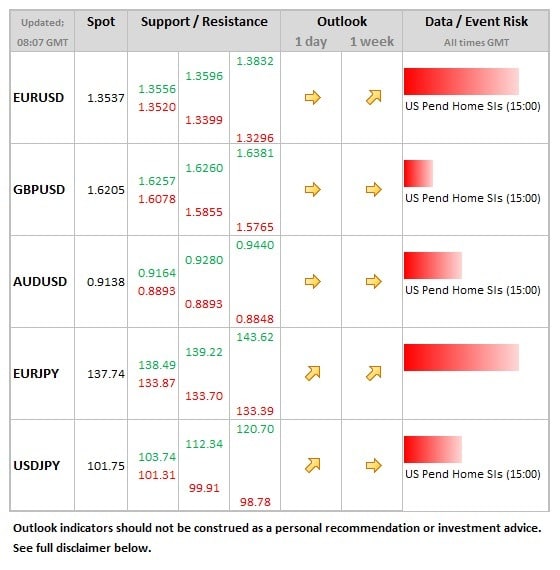

AUD: The Aussie finished what was its fifth week of losses against the US dollar on Friday. Last week it was helped by further comments from the RBA suggesting it was over-valued and subtle comments regarding intervention from Governor Stevens.

EUR: The euro was once again showing some resilience in the latter half of last week. Not all currencies can fall, so that was left to the Aussie and yen. The euro regained the losses seen after Wednesday’s story on the potential for a deposit rate cut, which were undermined by subsequent comments from ECB officials. Last week’s high of 1.3579 will be the initial upside focus for this week.

JPY: Key moves on the yen at the end of last week, breaking out to see USDJPY at a 4 ½ month high, with EURJPY at 4 year highs. It was not necessarily the case that there was a strong fundamental push for this, but there are a couple of themes bubbling beneath the surface. Firstly, a perception that the BoJ’s 2% inflation target is looking ever more distant. Secondly, upcoming changes to Nippon savings account and the possibility that this will push more Japanese savings overseas, something which has still remained largely illusive overall.

Further reading: