AUD/USD continued to lose ground last week, posting modest losses. The pair closed at 0.8919. This week is very busy with 16 releases. Here is an outlook on the major market-movers and an updated technical analysis for AUD/USD.

US releases continue to disappoint, as GDP missed the estimate and Unemployment Claims were higher than expected. In Australia, Private Capital Expenditure dropped sharply in January.

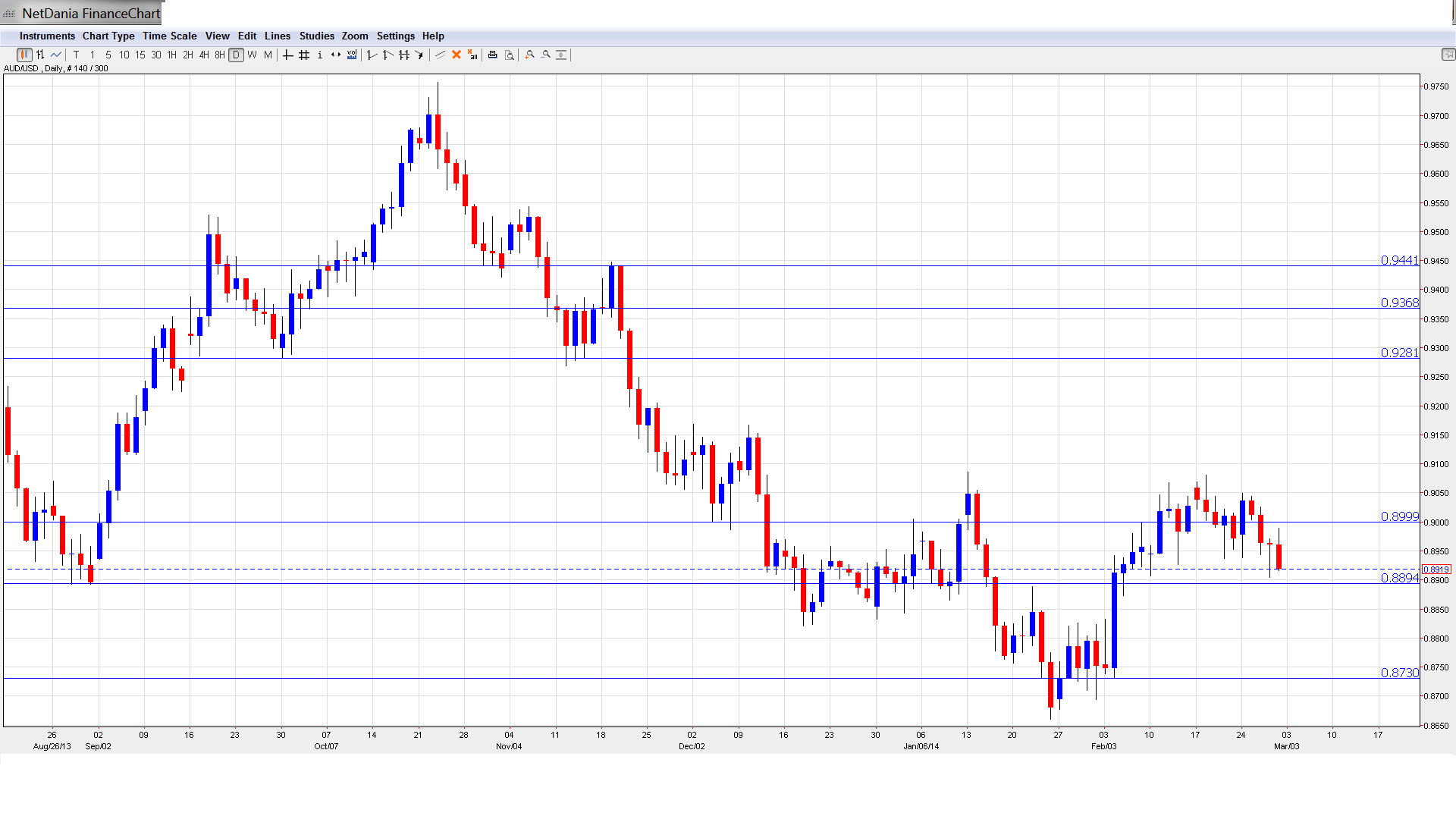

[do action=”autoupdate” tag=”AUDUSDUpdate”/]AUD/USD graph with support and resistance lines on it. Click to enlarge:

- AIG Manufacturing Index: Sunday, 22:30. The index has posted three straight readings under the 50-point level, indicating contraction in the manufacturing sector. The markets are not expecting much change in the upcoming release.

- Chinese Final Manufacturing PMI: Monday, 1:45. The Australian dollar is sensitive to key Chinese data, as the Asian giant is Australia’s largest trading partner. The index slipped below the 50-point line in January, pointing to contraction for the first time since August. Another drop is expected in the February release, with the estimate standing at 48.5 points.

- MI Inflation Gauge: Monday, 23:30. This indicator helps analysts track consumer inflation on a monthly basis, as CPI is only released each quarter. The January release dropped to just 0.1%, down from 0.7% a month earlier.

- HIA New Home Sales: Monday, Tentative. This event tends to fluctuate sharply. The indicator posted a decline of 0.4% last month, after a superb gain of 7.5% in December. The markets are hoping for a turnaround in the February release.

- ANZ Job Advertisements: Monday, 00:30. This employment indicator continues to look weak, having posted four consecutive declines. Will the indicator bounce back with a gain in February?

- Company Operating Profits: Monday, 00:30. This indicator tends to fluctuate, resulting in some estimates that are off the mark. The previous release posted an excellent gain of 3.9%, well above the estimate of 1.1%. The forecast for the February release stands at 2.3%.

- Commodity Prices: Monday, 5:30. Commodity Prices have been posting sharper declines, which does not bode well for the country’s key export sector. The January reading came in at -9.9%, and another decline is expected in the upcoming release.

- Building Approvals: Tuesday, 00:30. This key event has not impressed of late, with three declines in the past four releases. The markets are expecting a modest gain in the upcoming release, with an estimate of 0.7%.

- Current Account: Tuesday, 00:30. Current Account is directly linked to currency demand, as foreigners require Australian dollars to purchase domestic goods and services. The indicator is released every quarter, magnifying the impact of each release. In Q3, the deficit rose to -$12.7 billion, well above the estimate of -$11.1 billion. The markets are expecting an improvement in Q4, with an estimate of -$10.1 billion.

- Cash Rate: Tuesday 3:30. Although the RBA has surprised the markets with rate cuts more than once, it is very likely that the rates will remain at 2.50%, where they have been pegged since August. The RBA will announce the rate in a rate statement.

- AIG Services Index: Tuesday, 22:30. The index continues to post readings under the 50-point level, pointing to contraction in the services industry. The January reading came in at 49.3, its best showing in two years.

- GDP: Wednesday, 00:30. GDP, one of the most important economic indicators, is released on a quarterly basis. The indicator has been very steady, posting three straight gains of 0.6%. The estimate for Q4 stands at 0.7%.

- Retail Sales: Thursday, 00:30. Retail Sales is the primary gauge of consumer spending, a key component of economic growth. The indicator posted a gain of 0.5% in January, matching the forecast. No change is expected in the upcoming release.

- Trade Balance: Thursday, 00:30. Trade Balance shook off a string of deficits, posting a surplus of +$0.47 billion last month, well above the estimate of $0.27 billion. The markets are expecting another gain in February, with an estimated surplus of $0.11 billion.

- RBA Governor Glenn Stevens Speaks: Thursday, 22:30. Stevens will address a House of Representatives Economic Committee in Sydney. Remarks which are more hawkish than expected is bullish for the Canadian dollar.

- Chinese Trade Balance: Saturday, Tentative. The indicator looked strong in January, improving to $31.9 billion, well above the estimate of $24.2 billion. However, the markets are expecting a much weaker gain in February, with a forecast of $13.2 billion. If the indicator fails to meet expectations, we could see the Aussie lose ground.

*All times are GMT.

AUD/USD Technical Analysis

AUD/USD started the week at 0.8977 and quickly touched a high of 0.9049. The pair then reversed directions, dropping to a low of 0.8904, as support at 0.8893 (discussed last week) remained intact. The pair closed the week at 0.8919.

Technical lines from top to bottom:

We start with resistance at 0.9442. This marked the high point of the pair in November, which saw the Aussie go on a sharp slide and drop below the 0.89 line. This is followed by resistance at 0.9368, which was an important line in mid-November.

Next, there is resistance at 0.9283. This line saw a lot of action in the months of June and July, alternating between resistance and support roles. It has provided steady resistance since November.

0.9180 follows. It is followed by the round number of 0.9000, which was breached again this week as the Aussie briefly pushed higher. This key line has switched back to a resistance role to start the week.

0.8893 is the first support line. It held firm last week as the Aussie dropped close to the 0.89 line.

0.8728 marks the low point of an Aussie rally which began in early February and pushed above the 0.90 level.

This is followed by 0.8578, which has remained intact since July 2010.

The final support level for now is 0.8432, which played a key support role in late 2009.

I am bearish on AUD/USD.

The Aussie is having trouble cracking the 0.90 level, and with the Australian economy not churning out impressive numbers, there is room for the currency to lose ground. The US is also having its problems, but market sentiment remains positive and QE tapering is expected to continue later in March, which would be a vote of confidence from the Federal Reserve.

- For a broad view of all the week’s major events worldwide, read the USD outlook.

- For EUR/USD, check out the Euro to Dollar forecast.

- For the Japanese yen, read the USD/JPY forecast.

- For GBP/USD (cable), look into the British Pound forecast.

- For the Australian dollar (Aussie), check out the AUD to USD forecast.

- USD/CAD (loonie), check out the Canadian dollar.