The US dollar started 2017 with a bang, but that faded away quite quickly. What kind of rally is good for the dollar? Here is the view from Morgan Stanley:

Here is their view, courtesy of eFXnews:

The USD advance witnessed early last year was EM focused and in this sense, it was a ‘bad’ rally. When the USD rallies against EM,global economic costs tend to be high, as opposed to a ‘good’ rally where the USD rallies against low-yielding currencies such as the EUR and JPY.

The BIS has shown that EM currency weakness that pushes local funding costs higher by reducing EM access to international funding pools creates growth-reducing second-round effects. Seeing the USD higher against low-yielding currencies is supportive of global growth. This applies especially in the current situation, with low-yielding sovereign curves still tradingnear levels which we classify as leaving yield curves in ‘exhausted’ positions. EUR and JPY weakness is beneficial as it allows the ECB and BoJ to push local real yield levels down to desired levels. In this respect, low-yielding currency weakness against a rising USD is what we would call ‘good USD strength’.

Recent USD strength has been ‘good USD strength’. China’s currency is in a more difficult position. As low-yielding currencies fall, the RMB’s TWI trades higher unless China allows USDCNY to break higher. A higher RMB-TWI provides an unwanted decline in China’s relative competitive position, but a higher USDCNY may make it more difficult to keep capital outflows at bay.Failing to contain capital outflows may push RMB funding costs higher. China is clearly impacted by the USD rallying against low-yielding currencies,hence USD investors need to keep China’s currency moves in focus.

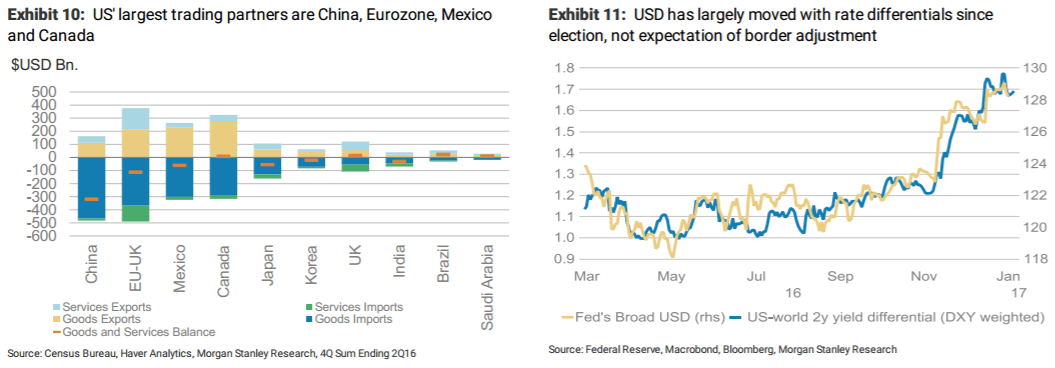

Border adjustment supportive of USD. Another USD bullish factor over the coming weeks and months will be the threat of protectionist measures by the new administration. As we wrote before the holidays the House Republicans have proposed converting the corporate income tax into a destination-based cash flow taxation system that would ‘border adjust’ by not taxing revenues from exports and disallowing dedication for the cost of imports. This would essentially have the same impact as an export subsidy and import tariff in equal size (20% based on the new corporate tax rate being proposed). USD would have to rise 25% on a trade weighted basis in order to offset the impact of these provisions on USD exporters and importers (which is what proponents of the plan argue will happen). We are more skeptical but still think this will be a big deal for USD; we believe a 10-15% rise in USD on the back of the policy is reasonable…

For lots more FX trades from major banks, sign up to eFXplus

By signing up to eFXplus via the link above, you are directly supporting Forex Crunch.

Even though we have our doubts that the policy will be ultimately implemented, we think the market is too complacent around the issue (and broader protectionist measures). House Republicans and the Trump administration have stayed with the plan despite large political pushback and it seems to be a policy which can fulfill Trump’s plans to boost US manufacturing that the Republicans can more readily support (as opposed to tariffs). Despite this, USD has barely moved since the markethas become more aware of the provision and much of USD previous gains were consistent with widening interest rate differentials. Therefore, we think the market is pricing a very low probability this plan is passed. As the market increases the probability of this occurring, USD should rall

At the very least, as this policy is debated over coming weeks, in our view this will be a lingering factor which reduces market appetite to be short USD.

For lots more FX trades from major banks, sign up to eFXplus

By signing up to eFXplus via the link above, you are directly supporting Forex Crunch.