EUR/USD continues to have a slow week, as the pair trades quietly in the mid-1.35 range. In economic news, US Pending Homes Sales looked weak, posting a fifth straight decline. On Tuesday, we’ll get a look at US Building Permits data for September and October, as the former was suspended due to the government shutdown last month. Today’s other key event is CB Consumer Confidence. There are no Eurozone releases on Tuesday.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

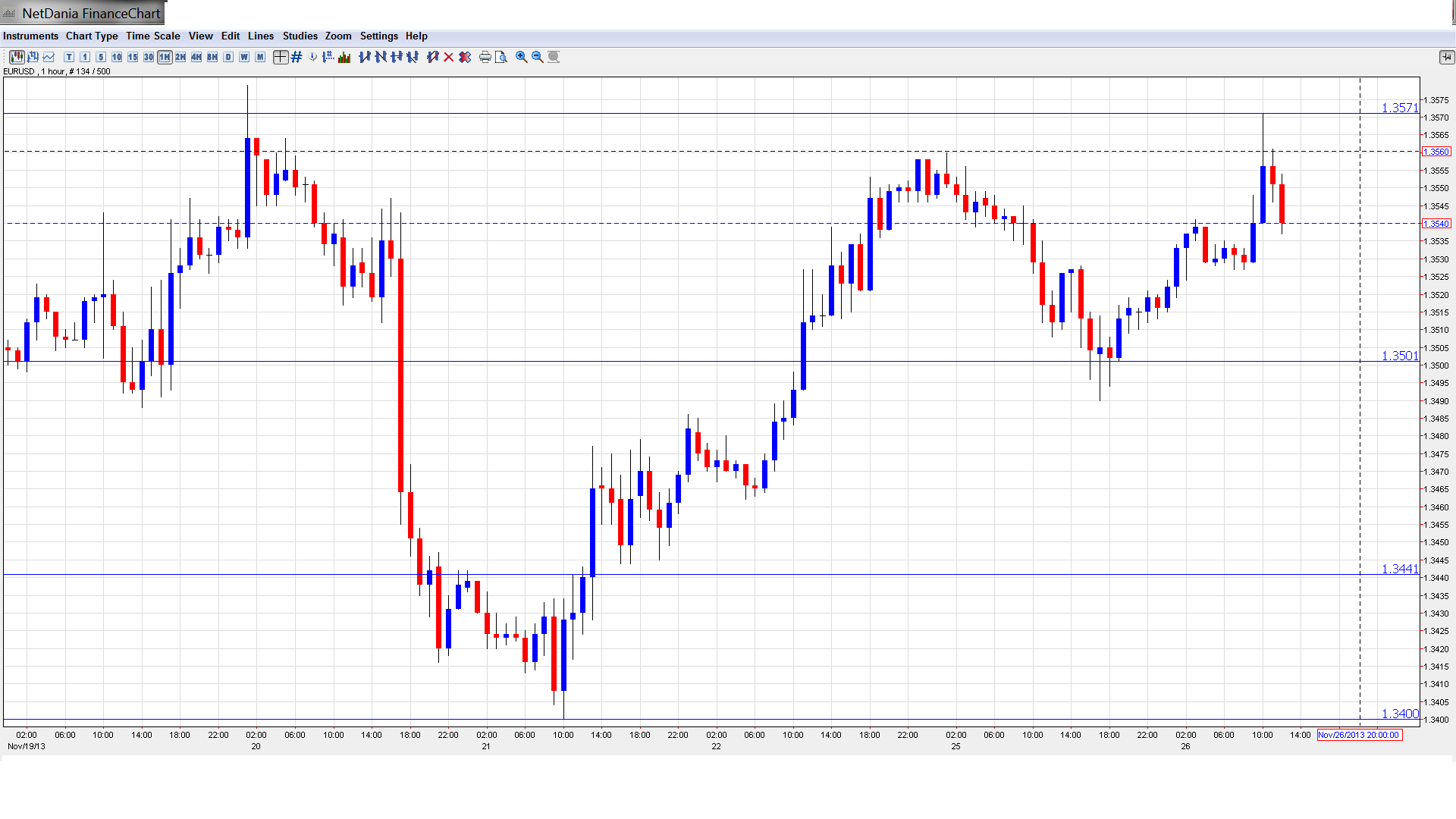

EUR/USD Technical

- EUR/USD edged higher late in the Asian session, consolidating at 1.3540. The pair is steady in the European session.

- Current range: 1.3440 to 1.3500.

Further levels in both directions:

- Below: 1.3440, 1.34, 1.3320, 1.3240, 1.3175, 1.31, 1.3050, 1.3000 and 1.2940.

- Above: 1.3500, 1.3570, 1.3650, 1.3710, 1.3800 and 1.3870.

- 1.3500 is providing weak resistance. 1.3570 follows.

- On the downside, 1.3440 is fluid. This is followed by 1.34.

EUR/USD Fundamentals

- 13:30 US Building Permits. Exp. 0.94M.

- 13:30 September Data – US Building Permits. Exp. 0.94M.

- 14:00 US S&P/CS Composite-20 HPI. Exp. 13.0%.

- 14:00 US HPI. Exp. 0.5%.

- 15:00 US CB Consumer Confidence. Exp. 72.2 points.

- 15:00 US Richmond Manufacturing Index. Exp. 3 points.

*All times are GMT

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- US Housing Numbers Falter: The week got off to a disappointing start as Pending Home Sales posted a decline of -0.6%, well off the estimate of 2.2%. The key indicator has now posted five straight declines, pointing to trouble in the housing sector. We’ll get a look at construction numbers on Tuesday, and weak releases could hurt the dollar.

- Fed minutes point to QE: Speculation that the Fed is getting ready to press the taper trigger increased following the release of the Federal Reserve minutes last week. In the minutes, policymakers said the current QE level of $85 billion monthly purchases of bonds could taper “in coming months” if the economy continued to improve. The dollar was up sharply after the minutes were released. Earlier in the week, Fed chair Bernard Bernanke said that the employment market improvement was “meaningful” and that interest rates would likely remain low even after QE ends.

- ECB mulls negative deposit rate: With inflation remaining very weak despite recent rate cuts, the ECB is considering cutting the deposit rate, which currently stands at 0.0%. However, a move into negative territory would represent unchartered territory and could have negative consequences for the economy. So if the ECB does go ahead and reduce to deposit rate, we could see a “mini cut” of less than 0.25%. The OECD is also expressing concern about the dangers of deflation in the Eurozone and is urging the ECB to consider implementing quantitative easing. ECB Governing Council member Ardo Hansson confirmed that the ECB could take further steps such as lowering the benchmark or deposit rates.

- German Business Confidence Improves: German data continues to look good, and Ifo Business Climate wrapped up the week on a high note. The indicator jumped to 109.3 points, up from 107.4 a month earlier. Earlier in the week, German PMIs pointed to continuing expansion in the services and manufacturing sectors. However, other members in the Eurozone are lagging behind Germany, and record low interest rates have not boosted inflation or economic growth in the region.