The global gloom has hit the dollar but had a different effect on bonds. This could be telling a bigger story for the greenback.

The team at Bank of America Merrill Lynch explains:

Here is their view, courtesy of eFXnews:

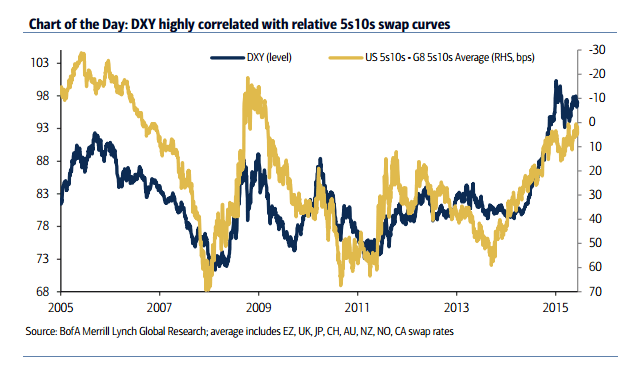

“Policy divergence has been and remains a key theme supporting our bullish USD stance. The transmission of this theme has manifested itself in rate differentials broadly moving in the USD’s favor. However, less followed has been the high correlation between the shape of US curves both on their own and relative to other G10 curves in driving the USD.

In fact, the flattening of the US 5s10s Treasury curve that began around the time the Fed officially announced tapering in December 2013 preceded the start of the broader DXY rally by about six months (Chart 1) suggesting it led the USD rally. More recently, the dollar and 5s10s curves began moving in a more synchronized manner, perhaps reflecting increased perceptions that USD strength would weigh on inflation, implying financial conditions were unlikely to tighten through both the exchange rate and interest rates.

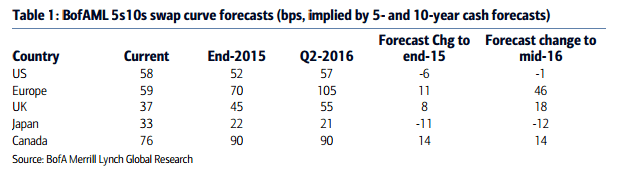

Our Rates team recently shifted to a longer-term (2-3 year horizon) steepening bias, raising the question of whether this will end USD strength? Not in the near term, in our view, for the following reasons:

1- The steepening curve our Rates team sees is expected to proceed over the next two to three years.

2- -5s10s swaps curves (implied by our global rates forecasts) are all expected to steepen through year-end and to the middle of next year with the exception of Japan and the US (Table 1). This means that on a relative basis, US curves will remain flat, providing support for the USD.”

Ian Gordon, Adarsh Sinha, Yang Chen, and David Woo – BofA Merrill Lynch

For lots more FX trades from major banks, sign up to eFXplus

By signing up to eFXplus via the link above, you are directly supporting Forex Crunch.