Idea of the Day

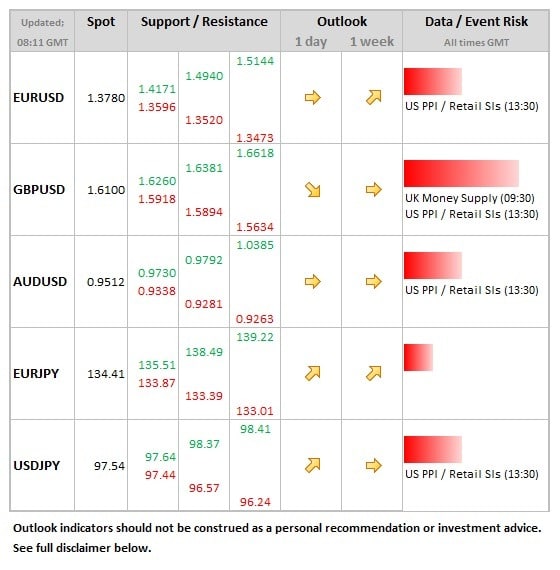

The euro was the strongest performer last week on the majors, pushing to a high of 1.3832 before pulling back into the weekend. Trends are what FX markets thrive on, but there’s an underlying reluctance to this rally, certainly evident in the wider market. Investors are fearful that there will be comments from officials and the next ECB meeting (next week) will increase this nervousness. But there are structural forces that are keeping the euro under-pinned. The fact that it is the second most liquid currency after the dollar, together with a sense that more flows back into the single currency could be seen as banks bolster their balance sheets ahead of the next round of stress tests. The dollar allowing, this suggest that the rally could have further to run.

Data/Event Risks

USD: PPI and retail sales data today, but impact of data on the dollar is receding as tapering expectations have been pushed well into next year. PPI is seen rising 0.2% MoM, with retail sales expected to be flat on the same measure.

Latest FX News

AUD: The wind has been taken out of the sales of the Aussie overnight by comments from RBA Governor Stevens, who stated that “at some point in the future the Australian dollar will be material lower than it is today”. The 0.9724 level, which is the mid-point of the year’s range to date, is likely to prove a tough barrier going forward after these comments.

GBP: As with the Aussie there was a sense that the currency is not keen to push new highs vs. the dollar. The recent run of data surprises and developments on interest rate differentials continue to suggest that sterling may struggle for now.

EUR: The euro has continued to defy expectations and push higher, making another year high last week. The 1.40 area, not seen since November 2011 is not that far away, but there remains an underlying reluctance on the part of the wider market to go with the flow towards this level.

Further reading:

EURUSD: Corrective Pause Within Uptrend Is Pointing Towards 1.3860/1.3900