EUR/USD continues to have a fairly quiet week, with the pair trading in the high-1.33 range in European trading on Wednesday. In economic news, the US finally broke out with some strong releases as consumer climate and manufacturing releases looked very sharp. On Wednesday, German Consumer Climate disappointed as it fell short of the estimate. On a brighter note, Eurozone M3 Money Supply surpassed the forecast. The market-mover of the day is US Pending Home Sales.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

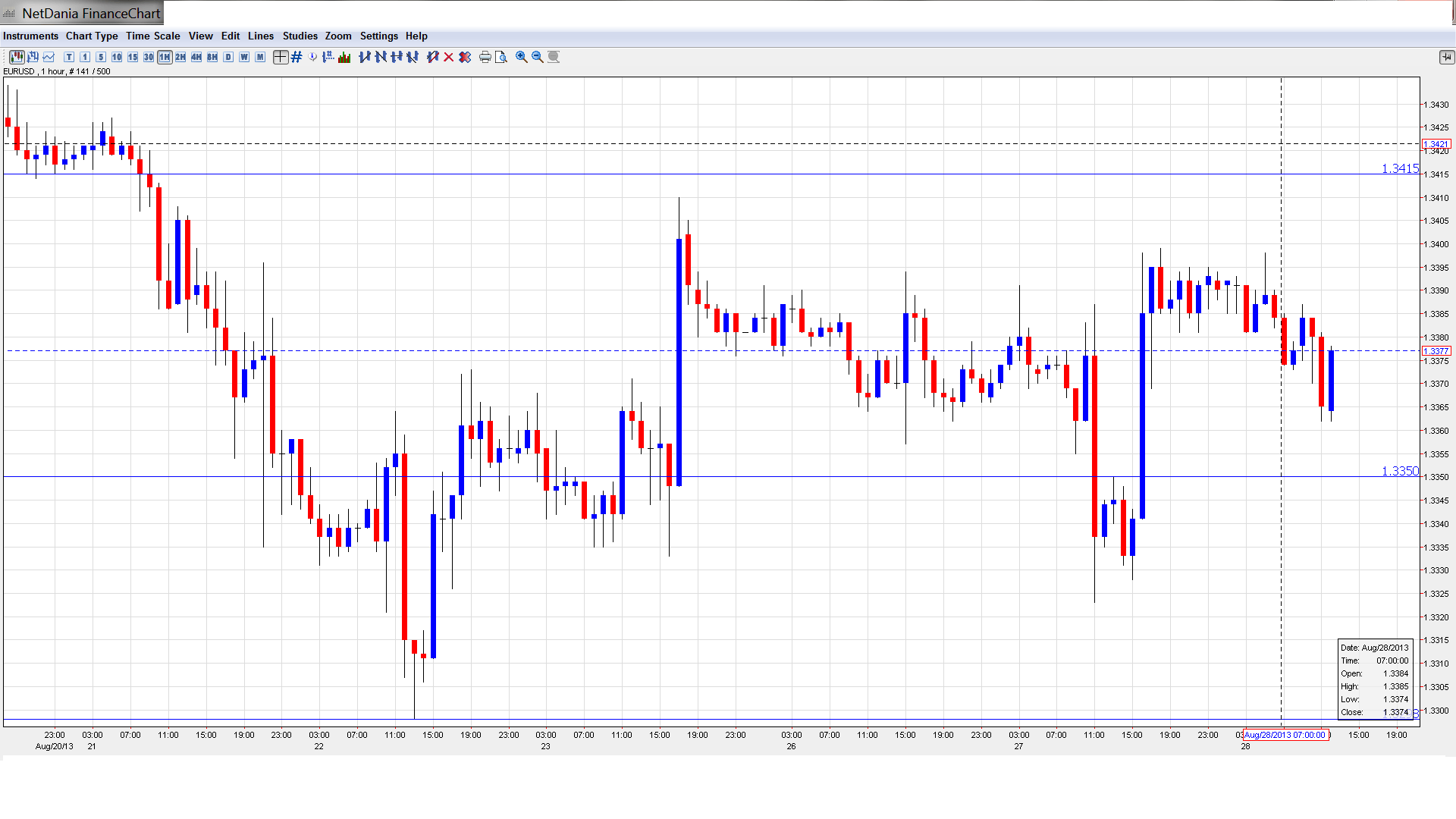

EUR/USD Technical

- In the Asian session, EUR/USD was steady, touching a high of 1.3398 before consolidating at 1.3377. The pair is unchanged in the European session.

Current range: 1.3350 to 1.3415.

Further levels in both directions:

- Below: 1.3350, 1.33, 1.3240, 1.3175, 1.31, 1.3050, 1.30 and 1.2940.

- Above: 1.3415, 1.3450, 1.3520, 1.3590 and 1.37.

- 1.3350 is providing weak support. 1.3300 is next.

- 1.3415 is the next resistance line. 1.3450 is stronger.

EUR/USD Fundamentals

- 6:00 GfK German Consumer Climate. Exp. 7.1, actual 6.9 points.

- 6:00 German Import Prices. Exp. 0.3%, actual 0.3%.

- 8:00 Eurozone M3 Money Supply. Exp. 2.0%. Actual 2.2%.

- 8:00 Italian Retail Sales. Exp. 0.1%, actual -0.2%.

- 6:00 Eurozone Private Loans. Exp. -1.5%, actual -1.9%.

- 14:00 US Pending Home Sales. Exp. 0.2%. See

how to trade this event with USD/JPY - 14:30 US Crude Oil Inventories. Exp. 0.5M.

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- US rebounds with strong numbers: After a string of disappointing key releases, US data looked sharp on Tuesday. CB Consumer Confidence rose to 81.5 points in August, its highest level since January 2008. The estimate stood at 79.6. After some weak manufacturing data earlier in the week, Richmond Manufacturing Index sparkled, soaring from -1 to +14 points. This crushed the estimate of -7 points and was the indicator’s best showing since April 2012. If US data continues to look good, we could see the dollar post gains against the euro, which failed to take advantage of the recent weak numbers out of the US.

- Mixed data out of Germany: German Ifo Business Climate started the week on a positive note, posting its fourth consecutive gain and climbing to its highest level in over a year. However, GfK German Consumer Climate could not keep up, as it dropped slightly from 7.0 to 6.9 points, missing the estimate of 7.1 points. Last month’s reading of 7.0 was a multi-year high, so the slight drop is unlikely to be of great concern to the markets. German consumers continue to spend, but are worried about inflation. National elections are just a few weeks away, and the economy promises to be the central issue of the campaign as Chancellor Angela Merkel seeks a third straight term in office.

- Fed split over QE tapering timing: The Federal Reserve has kept mum about when it might taper QE, but the recent Jackson Hole summit provided a glimpse of the divisions in the Fed as to when it might act. Fed chair Bernard Bernanke was a no-show at the summit, giving other policymakers an opportunity to express their views on QE. Dennis Lockhart, head of the Atlanta Fed, said that tapering could start in September, but only if US data justified such a move. There was a more hawkish statement from James Bullard, head of the St. Louis Fed. Bullard said that there was no need for the Fed to rush into QE tapering. The uncertainty over QE tapering has buoyed the US dollar, raised the yields on US treasury bonds and led nervous investors to pull billions of dollars out of emerging markets. With September just around the corner, we could see strong volatility in the markets as speculation over QE heats up.

- Dollar shrugs off weak releases: The US has posted some weak key releases, but the dollar remains firm against the euro and other major currencies. On Friday, US New Home Sales dropped sharply. The indicator had beaten the estimate for four consecutive releases, but that impressive streak came to a crashing end on Friday, as the indicator slid to its lowest level since January. Core Durable Goods Orders was released on Monday, and the key manufacturing index posted a decline of -0.6%. Despite these weak numbers, the dollar was not hurt, as the markets seem more focused on QE than on US economic data.

- Greece wants more aid but no strings attached: Greece has already received two bailouts from the troika, amounting to some 240 billion euros. Despite this massive infusion of funds, the country’s economy is still in difficult straits, and there is talk of a third bailout. On Sunday, Greek finance minister Yannis Stournaras said that Greece was looking for another 10 billion euros in aid, but would not adopt any austerity measures in return. Germany is unlikely be in a giving mood, with just weeks to go before national elections in Germany. Another rescue package for Greece could damage Chancellor Angela Merkel’s credibility, as she recently said she didn’t see a need for more aid to Greece.