EUR/USD continues to trade at high levels on Thursday, as the pair is trading in the mid-1.37 range. In economic news, it’s a busy day. Eurozone Industrial Production was a major disappointment, with a sharp decline of 1.1%. Later on, ECB President Mario Draghi will speak about ECB policy at the European Parliament in Strasbourg. The US has three key events later in the day – Core Retail Sales, Retail Sales and the Unemployment Claims. So we could have an eventful day, and traders should be prepared for some volatility from EUR/USD.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

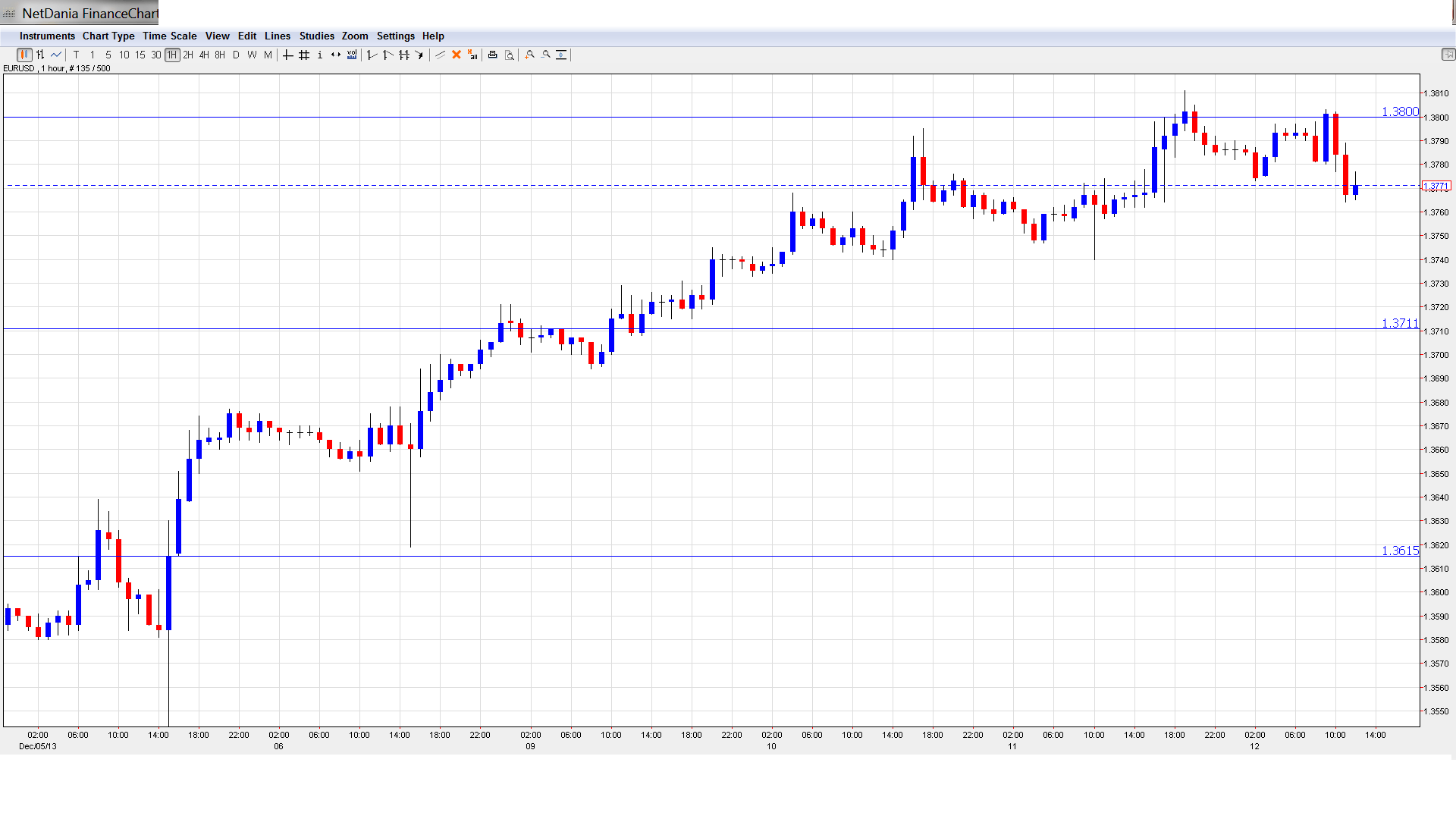

EUR/USD Technical

- EUR/USD moved higher late in the Asian session, pushing across the 1.38 line and consolidating at 1.3801. The pair has lost ground in the European session.

- Current range: 1.3710 to 1.3800.

Further levels in both directions:

- Below: 1.3710, 1.3675, 1.3615, 1.3525, 1.3440, 1.34, 1.3320, 1.3240, 1.3175 and 1.31.

- Above: 1.3800, 1.3870, 1.3940 and 1.4036.

- 1.3710 continues to provide support. 1.3675 is next.

- On the upside, 1.3800 is under strong pressure. 1.3870 follows.

EUR/USD Fundamentals

- 7:45 French CPI. Exp. 0.1%, Actual 0.0%.

- 8:00 ECB President Mario Draghi Speaks.

- 9:00 ECB Monthly Bulletin.

- 10:00 Eurozone Industrial Production. Exp. 0.4%. Actual -1.2%.

- 13:30 US Core Retail Sales. Exp. 0.2%.

- 13:30 US Retail Sales. Exp. 0.6%.

- 13:30 US Unemployment Claims. Exp. 321K.

- 13:30 US Import Prices. Exp. -0.7%.

- 15:00 US Business Inventories. Exp. 0.4%.

- 15:30 US Natural Gas Storage. Exp. -85B.

- 18:01 US 30-year Bond Auction.

*All times are GMT

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Eurozone Industrial Production slides: Eurozone manufacturing data continues to look weak, as Eurozone Industrial Production declined 1.1% in November, its weakest showing in three months. The markets had expected a gain of 0.4%. Earlier in the week, German and French Industrial Production posted declines and were well short of their estimates. These indicators underscore weak economic activity which is hobbling the Eurozone. However, the euro has managed to shrug off weak Eurozone data, and has gained closed to 200 points since the start of December.

- European finance minister discuss banking union: EU finance ministers met in Brussels on Tuesday and high on the agenda was a proposal for a European banking union. The aim is to relieve debt-ridden countries from the burden of rescuing failing banks in their countries. Instead, the banks would tap a Eurozone rescue fund, the Single Resolution Mechanism. However, no agreement has been reached on the SRM, and the finance ministers are likely to meet again next week to try and hammer out details of a banking union. ECB head Mario Draghi is a firm supporter of a banking union and has urged national governments to move forward with the plan.

- German data disappoints: The week started off on a sour note, as German releases fell below market expectations on Monday. Germany’s trade surplus shrank to 16.8 billion euros, down from 18.8 billion in October. Industrial Production declined by 1.2%, the third decline in the past four readings. The estimate stood at 0.8%. German CPI gained 0.2%, which matched the estimate. Although just a modest gain, this was the best figure we’ve seen in the past four months. If German numbers don’t improve, we’re unlikely to see much growth out of the struggling Eurozone economy.

- Will Fed taper in December? Last week’s employment numbers were super, as Unemployment Claims, Non-Farm Payrolls and the Unemployment Rate all impressed. There was more good news this week, as US Job Openings hit its highest level in over five years. The Fed has said that a stronger employment picture is a prerequisite to tapering, and last week’s numbers certainly increase the possibility of the Fed taking action at its December policy meeting. Other factors also favor a December taper. Currently, the Fed is purchasing $85 billion in assets every month, and a Fed taper will likely boost the US dollar against the major currencies.

- Negotiators reach budget agreement: With memories of the October government shutdown still fresh on Capitol Hill, Congressional negotiators have reached a budget deal which Congress will have to pass. The agreement will remove the risk of a government shutdown and reduce the deficit by a modest $23 billion. Democrats and Republicans both had criticism of the proposal, but there is general agreement in Washington that the compromise reached is a positive step which removes some of the economic uncertainty we’ve seen in recent months. Congress must approve a budget, or the US could face another government shutdown in mid-January.