EUR/USD has looked listless all week and we’re seeing more of the same on Wednesday, as the pair continues to trade in the mid-1.37 range. German Consumer Confidence continues to rise and hit its highest level in seven years. In the US, today’s highlight is New Home Sales. The markets are braced for a weaker reading than last month.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

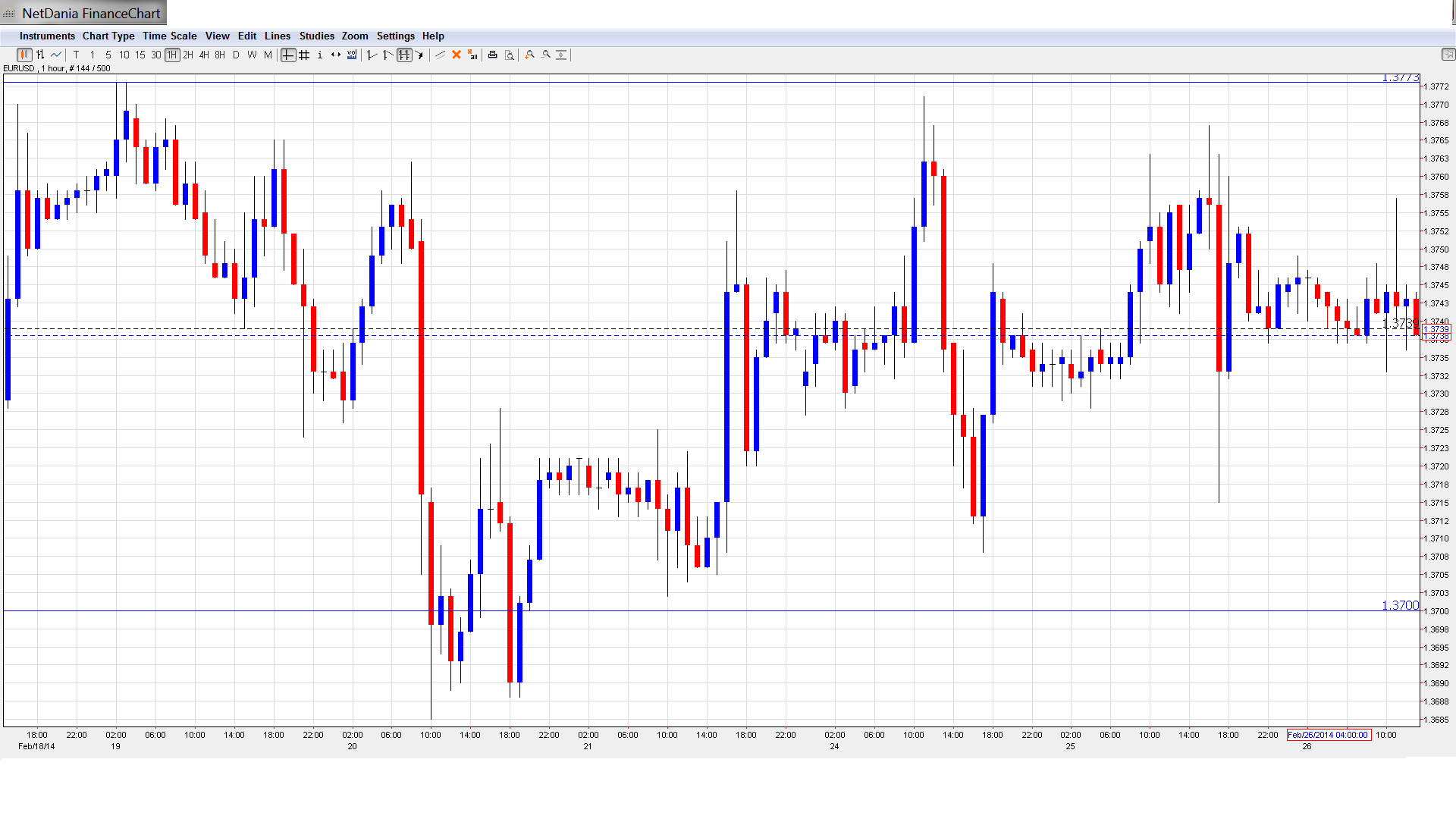

EUR/USD Technical

- EUR/USD has not shown much movement in the Asian or European sessions, as the pair continues to trade close to the 1.3740 line.

Current range: 1.37 to 1.3773. Further levels in both directions:

- Below: 1.37, 1.3650, 1.3580, 1.3515, 1.3450 and 1.34

- Above: 1.3773, 1.38, 1.3830, 1.3895, 13915 and 1.40.

- 1.3773 is a weak resistance line. 1.38 is next.

- 1.37 continues to provide support. This is followed by 1.3650.

EUR/USD Fundamentals

- 7:00 GfK German Consumer Climate. Exp. 8.3, actual 8.5 points.

- Tentative – German 30-year Bond Auction.

- 15:00 US New Home Sales. Exp. 406K.

- 15:30 Crude Oil Inventories. Exp. 1.1M.

*All times are GMT

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Thumbs-up from German consumers: German GfK Consumer Confidence continues to rise, as the key indicator moved upwards for the fourth straight month. The indicator hit 8.5 points, its highest level since January 2007. The markets had expected another strong showing, with an estimate of 8.3 points. The excellent reading comes on the heels of German Ifo Business Climate, which also posted a multi-year high. A strong German CPI release on Thursday could push up the euro.

- ECB hints at negative rates: ECB Governing Council member Ignazio Visco said that a negative deposit rate is on the agenda in the upcoming March meeting (currently the rate is at 0%). While the ECB may not take action, this comment certainly weighed on the euro. It joins similar sentiments out of the ECB and some complaints about the euro’s strength from the head of the Eurogroup. The key to the ECB decision is the flash CPI figure for February, which will be released on Friday.

- Markets watching developments in the Ukraine: The Ukrainian president was practically overthrown and is fleeing an arrest warrant. He may be in Russia. With the Winter Olympic Games now over in Sochi, Russian president Putin may get involved in his neighbor’s affairs. Political, military and economic turmoil (such as a default of the Ukraine on its debt) may trigger a contagion effect.

- US housing data raises concerns: Recent US numbers have not impressed, and the weak numbers are being felt in the housing sector. Building Permits slid to a five-month low in January, dropping to 0.94 million. The estimate stood at 0.98 million. Existing Home Sales looked awful, dropping to 4.62 million in January, compared to 4.87 million a month earlier. This was well short of the estimate of 4.73 million, and the lowest reading from the key indicator since July 2012. Is the housing sector experiencing a downturn? The markets will be hoping for better news from New Home Sales later on Wednesday.

- Federal Reserve may adjust forward guidance: Last week’s Federal Reserve minutes indicated that interest rates are unlikely to rise, even if unemployment drops to 6.5%. Previously, the Fed had said it would consider raising rates at the 6.5% threshold, but with unemployment falling faster than expected, Fed policymakers agreed that it would “soon be appropriate” to revise the Fed’s forward guidance regarding interest rate levels. The minutes also indicated that the Fed will likely continue trimming QE, barring any downturns in the economy.

More: Video: Game changing EUR event, USD/JPY before the burst and more