EUR/USD has edged higher on Tuesday, as the pair trades in the mid-1.36 level in the European session. There are no Eurozone releases today, but there are two major releases out of the US. Incoming Federal Reserve Chair Janet Yellen will testify about the Fed’s Semiannual Monetary Policy Report before the House Financial Services Committee. As well, JOLTS Job Openings will be released later in the day.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

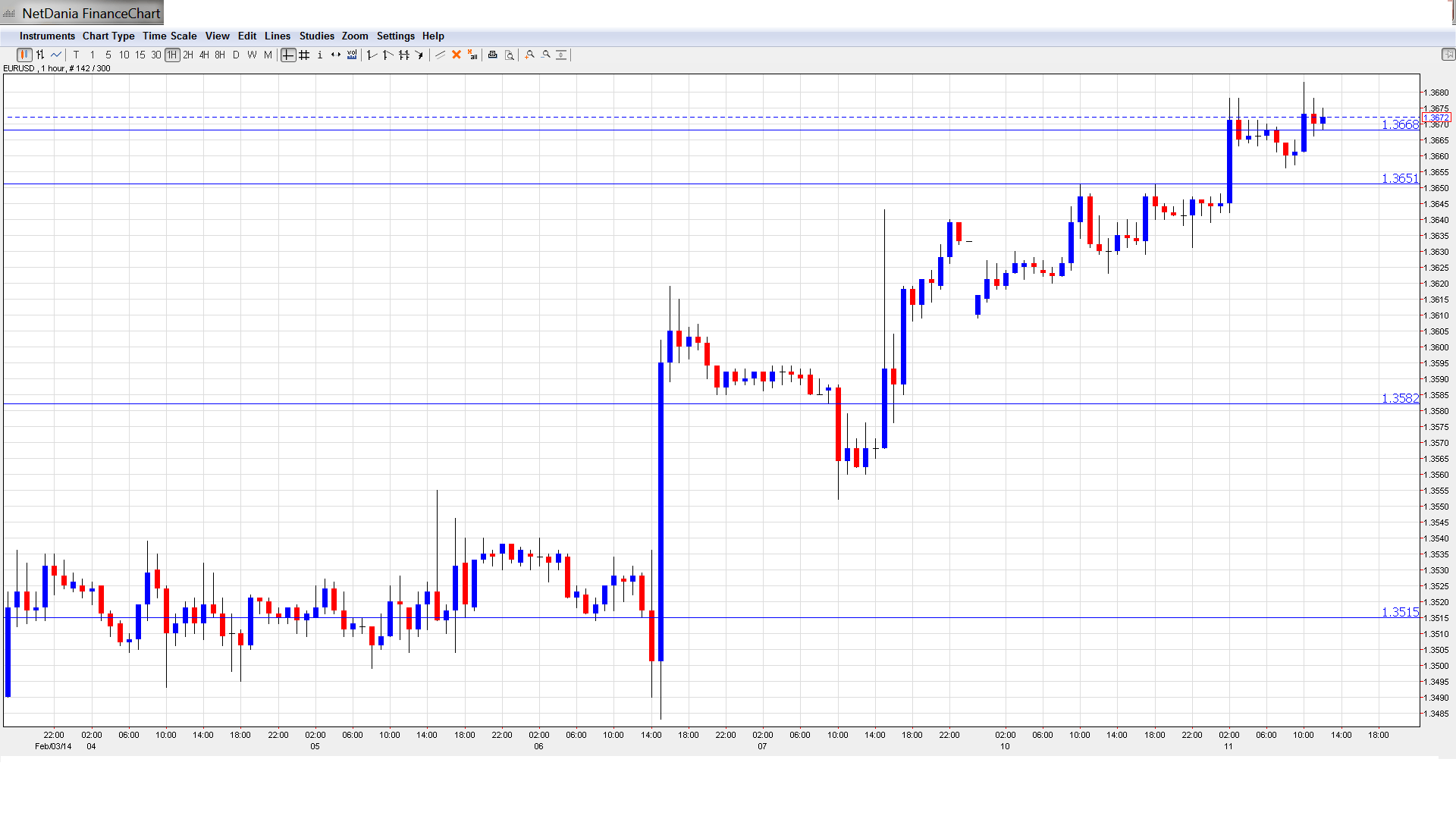

EUR/USD Technical

- EUR/USD was stable in the Asian session and closed at 1.3673. The pair is unchanged in the European session.

Current range: 1.3650 to 1.3700

Further levels in both directions:

- Below: 1.3650, 1.3580, 1.3515, 1.3450, 1.34, 1.3320, 1.3295, 1.3175, 1.31 and 1.3050.

- Above: 1.37, 1.38, 13915 and 1.40.

- 1.3650 is providing weak support. 1.3580 is next.

- 1.3700 is the first resistance line. 1.38 is stronger.

EUR/USD Fundamentals

- 12:30 US NFIB Small Business Index. Exp. 93.6 points.

- 14:00 US FOMC Member Charles Plosser Speaks.

- 15:00 US Fed Chair Janet Yellen testifies before the House Financial Services Committee.

- 15:00 US JOLTS JOB Openings. Exp. 4.04M.

- 15:00 US Wholesale Inventories. Exp. 0.5%.

*All times are GMT

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Yellen Testifies Before Congress: Incoming Federal Reserve Chair Janet Yellen took over the reins of the Fed last week, and heads to Congress on Monday to present her first semi-annual testimony in front of the House Financial Services Committee. She is expected to reiterate the Fed’s plan to continue its taper of QE and wind up the stimulus program by the end of the year, despite recent weakness in the economy and some worrying NFP numbers. Traders should be prepared for some fluctuation from EUR/USD as a result of Yellen’s remarks.

- Eurozone Manufacturing Data Disappoints: Eurozone Industrial Production looked weak in January. The French release posted a decline of 0.3%, shy of the estimate of -0.1%. This was the third decline in four readings, pointing to weak activity in the French manufacturing sector. Italian Industrial Production headed south after three straight gains, with a decline of 0.9%. The markets had expected a reading of 0.0%. We’ll need to see stronger economic data if the Eurozone economy is to improve.

- Euro rallies after Draghi comments: Last week, the ECB left interest rates unchanged at 0.25%. This was certainly expected, but the upbeat message was certainly not, and the euro rallied. Not only did Draghi deny deflation, but he also found a reason for every malaise: low headline inflation is due to energy prices, low core inflation is due to the program countries (Greece, Portugal, etc.), and even the squeeze in money supply, M3, is a result of the upcoming stress tests. Draghi expects the latter to improve shortly. However, he also said that more data is awaited in early March. The high exchange rate could result in even lower inflation and a move in March cannot be ruled out.

- Taper moves on track: The taper train has left the station, as the Fed has implemented two cuts of $10 billion to the QE scheme, reducing QE to $65 billion each month. Only really bad figures can stop the Fed from continuing to reduce QE. The Fed took its time with making the decision, and it will be hard to stop it now, even if emerging markets crumble again. Another reason for pushing on with the move is that the Fed is more hawkish now.

More: Analysis: ECB expects the situation to sort itself out, but things could still worsen