EUR/USD maintained its range as we entered the last month of the year. The ECB meeting is left, right and center this week, but certainly not the only event, in a week that starts with the fallout from the Italian referendum. Here is an outlook for the highlights of this week and an updated technical analysis for EUR/USD.

Euro-zone inflation remained mediocre, not helping the euro. Worries about the Italian referendum also weighed. In the US, GDP came out at an upbeat 3.2% according to the revised data. Also, consumer confidence beat expectations. The NFP was mixed: job gains were OK but wages disappointed. However, the dollar seemed to consolidate its gains seen in November.

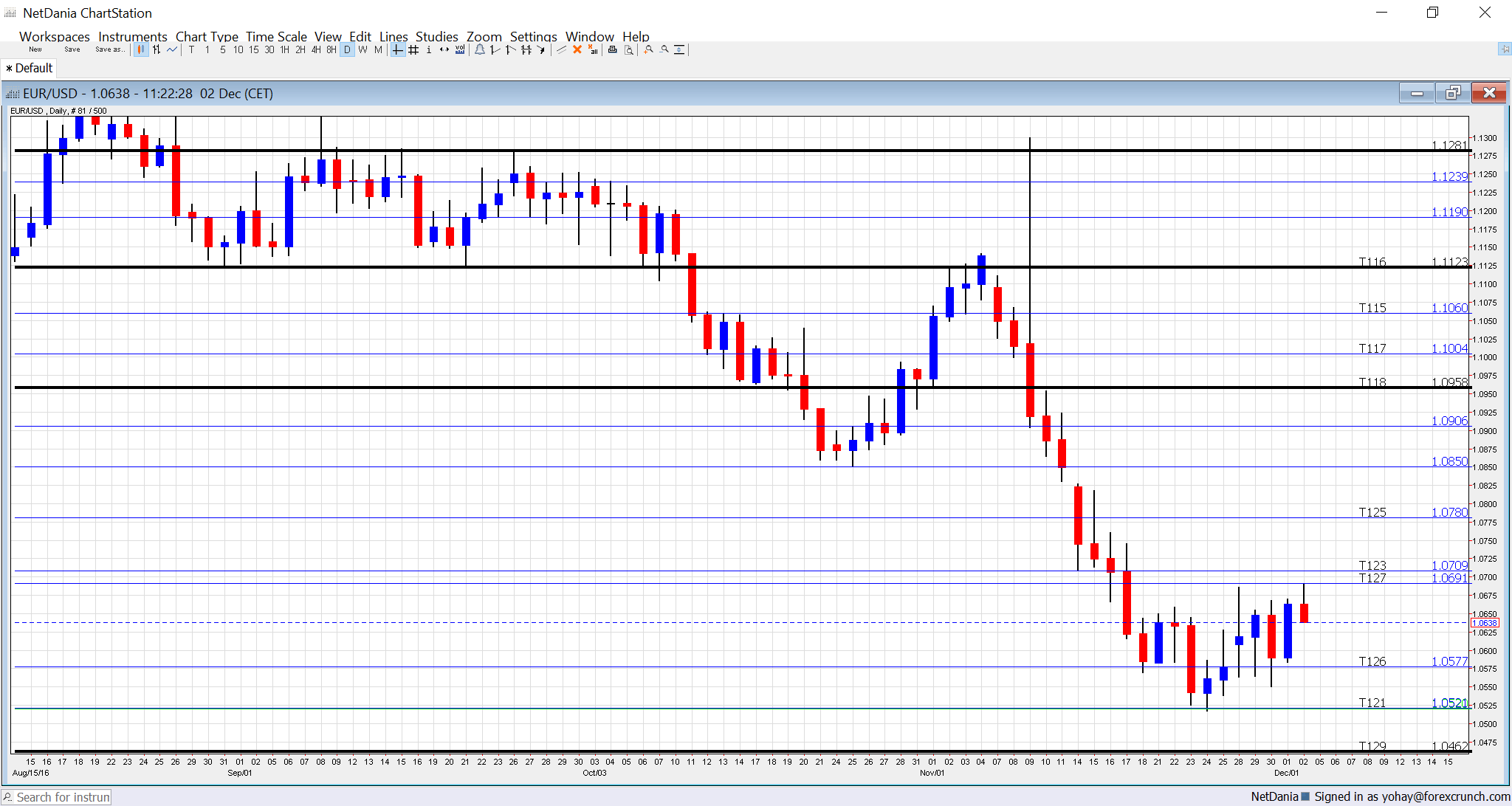

[do action=”autoupdate” tag=”EURUSDUpdate”/]EUR/USD daily graph with support and resistance lines on it. Click to enlarge:

- Italian Referendum: Sunday. Italians go to the polls to decide on far-reaching changes to the political system, moves that, if approved, are supposed to make the third-largest economy of the euro-zone more governable. Prime Minister Matteo Renzi has made the vote also critical for his personal future, raising the stakes for the euro-zone and Italian banks. Polls show a lead for the NO camp in the #Renzirendum, with some saying that such an outcome could be the “third fall” after Brexit and Trump. However, this hype may be exaggerated: Italy is used to function with a rapid change of governments. A NO vote would be negative for the euro, but it is probably priced in, while a YES vote would be a big surprise and could result in a leap when markets open on Sunday.

- Eurogroup meetings: Monday, with the wider Ecofin on Tuesday. Finance ministers of the 19-country euro area convene to discuss various matters: the implications of the Italian referendum will be high on the agenda and so will the ongoing Greek saga as well as the upcoming Brexit negotiations and the woes of banks. An optimistic view on the various issues could help the euro while a “euro-fudge” could weigh on it.

- Services PMIs: Monday: 8:15 for Spain, 8:45 for Italy, final French figure at 8:50, final German number at 8:55 and the final read for November for the whole euro-zone at 9:00. According to Markit, Spain had a score of 54.6 points in October, reflecting OK growth. 50 points is the threshold that separates expansion and contraction. A score of 55.1 points is on the cards now. Italy had a score of 51 points, closer to no-growth and 51.4 is predicted now. According to the initial release for France, the country had 52.6 points. Germany had a score of 55, expressing better growth. The whole euro-zone had 54.1 points. The latter three figures will likely be confirmed.

- Sentix Investor Confidence: Monday, 9:30. In November, this survey of around 2800 analysts and investors surprised with an upbeat level of 13.1 points, extending the advance seen in previous months, to 14.7 points.

- Retail sales: Monday, 10:00. German retail sales beat with a rise of 2.4% in October, raising expectations for the all-European release. Back in September, the euro-zone saw a drop of 0.2%. A bounce is on the cards now: +0.9%.

- German Factory Orders: Tuesday, 7:00. This volatile indicator dropped by 0.6% last month. Despite the bouncy nature, the release does have an impact. A rise of 0.6% is projected.

- Retail PMI: Tuesday, 9:10. Markit’s measure for the retail sector stood at 48.6 points back in October. No significant change is expected now.

- GDP: Tuesday, 10:00. This is a revision of GDP growth in Q3 2016. The previous release showed 0.3%, in line with expectations and not showing any acceleration in growth. This will probably be confirmed now.

- German Industrial Production: Wednesday, 7:00. German industrial output dropped by no less than 1.8% in September, disappointing many. A bounce is projected now: +0.9%.

- French Trade Balance: Thursday, 6:30. Contrary to Germany, France has a chronic trade deficit. This widened to 4.8 billion in September but now, a narrower deficit of 4.2 billion is on the cards.

- ECB decision: Thursday: decision at 12:45 and the press conference is at 13:30. The European Central Bank is not expected to change its monetary policy, leaving the main lending rate at 0%, the deposit rate at -0.40% and the QE program at 80 billion euros per month. However, we will get updated forecasts from the staff and more importantly, markets expect announcements regarding the next steps in the QE program. The bond-buying scheme is scheduled to end in March 2017. In the previous two rate decisions, ECB President Mario Draghi told us that either extending it or tapering it down were not discussed. However, now is probably the time to spread the news. There are good reasons to expect an extension of the program in the current conditions. Inflation in the euro-zone remains low, despite rising oil prices. The ECB is only very slowly getting closer to its 2% target, with inflation currently at 0.6%. Also, problems in banks also imply further assistance. Another reason comes from the other direction: in the past, there were worries about the ECB finding enough bonds to buy. It has a self-imposed limit of buying bonds yielding higher than -0.40%. However, with the recent bond sell-off, yields are now higher, making it easier for the ECB to find bonds to buy. An extension of 6 months would not be a surprise and would follow the previous 6-month extension from September 2016 to March 2017. An extension of one year would already be very bearish for EUR/USD. On the other end, a reduction in the pace of bond buys from March to 70 or 60 billion, would boost the euro.

- German Trade Balance: Wednesday, 7:00. Germany enjoys a wide surplus in its trade balance, reaching 21.3 billion euros back in September. The numbers for October are forecast to be similar. A narrower surplus of 20.8 billion is forecast.

- French Industrial Production: Friday, Also the second largest economy in the euro-zone saw a drop in its output, a fall of 1.1% in September. A recovery is on the cards: +0.6%.

* All times are GMT

EUR/USD Technical Analysis

Euro/dollar traded in clear ranges mentioned last week. It failed to stage an outright recovery but also refrained from the lows.

Technical lines from top to bottom:

1.10 is a round number and significant resistance. 1.0960, which supported the pair in early 2016 worked as resistance in October. 1.0850, which worked as support during the same month, serves as support.

The post-Draghi low 1.0780 replaces 1.08 as support. 1.0710 is the next support line on the chart after temporarily capping the pair in April 2015.

1.0690 is the post-Trump high. 1.0570 is the bottom of the range seen afterwards.

Further below, the 2016 low of 1.0520 and the 2015 low of 1.0460 provide further support – it is the last line in the sand.

I remain bearish on EUR/USD

In the current environment, the ECB is likely to continue QE, keeping the pressure on the euro and emphasizing the monetary policy divergence with the FED.

Our latest podcast is titled From the Crude Cut to Draghi’s Drag

Follow us on Sticher or iTunes

Safe trading!