EUR/USD had a bad week, even temporarily sliding below 1.25. Are we set for a bounce from the double bottom or is the third time a charm? The ECB decision is the clear highlight of a very busy week to open the penultimate month of the year. Here is an outlook on the highlights of this week and an updated technical analysis for EUR/USD.

Inflation in the euro-zone remains low, with CPI at 0.4% and Core CPI at 0.7%. Disappointing German inflation created worries for even lower numbers. The zone’s locomotive also printed another falling business confidence number, but at least the number of unemployed is falling. The much anticipated stress tests didn’t break any scary news and were well received by markets, even though they didn’t take a deflation scenario into account. In the US, the Fed finally ended QE and even sounded upbeat on the labor market. In addition, GDP beat expectations, even though doubts were cast about its quality. While not all US data shine, the overall picture is positive. Does all this imply another leg lower for the pair or is everything already baked into the current price? Let’s start:

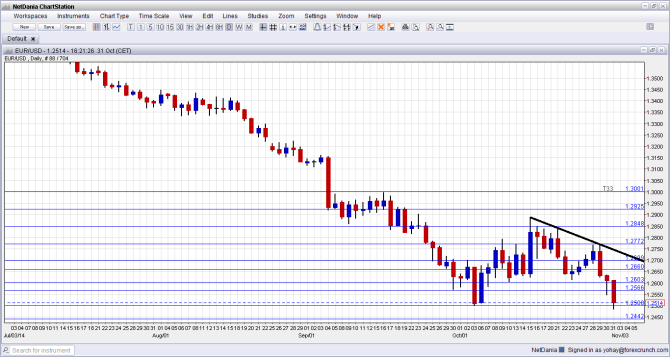

[do action=”autoupdate” tag=”EURUSDUpdate”/]EUR/USD daily graph with support and resistance lines on it. Click to enlarge:

- Manufacturing PMI: Monday, 8:15 for Spain, 8:45 for Italy and 9:00 sees final manufacturing PMI for the euro-zone. According to Markit, the manufacturing sector is somewhat growing, with a score of 52.6 in September. A minor slide to 52.4 is expected. Italy’s manufacturing sector is closer to stall speed (50 points). Also here, a dip from 50.7 to 50.6 is expected. For the whole euro-zone, the preliminary read of 50.7 is expected to be confirmed with these numbers and updates from France and Germany.

- Spanish Unemployment Change: Tuesday, 8:00. Spain has seen a remarkable drop in its high unemployment rate, but the improvement in jobless claims seemed to have slowed down. After a rise of 19.7K in September, a bigger rise of 23.4K is expected in the zone’s fourth largest economy.

- EU Economic Forecasts: Tuesday, 10:00. These medium term forecasts for the next two years are made using a detailed assessment and released only 3 times per year. While forecasts get it wrong quite often, they reflect current expectations. When Germany lowered forecasts, it had a dampening impact on the euro.

- PPI: Tuesday, 10:00. The Producer Price Index dropped by 0.1% in August and no change is expected in September. This is another inflation number feeding into the ECB meeting and it fell in recent months more often than not.

- Services PMI: Wednesday: 8:15 for Spain, 8:45 for Italy and 9:00 sees final services PMI for the euro-zone. The services sector is doing better than the manufacturing one, but not in all countries. While Spain is expected to see the purchasing managers’ indicator advance from 55.8 to 56.2 points in October, Italy’s is expected to remain in contraction zone, rising from 48.8 to 49.6 points. For the whole euro-zone, a confirmation of the initial read of 52.4 points is predicted.

- Retail Sales: Wednesday, 10:00. Germany’s retail sales badly disappointed with a fall of 3.2%. This is expected to send the whole euro-zone to a dive of 0.6% in September after a surprising rise of 1.2% in August.

- German Factory Orders: Thursday, 7:00. On the same day the ECB releases its decision, we will get to know if the huge plunge of 5.7% in Germany’s orders in August was indeed a one-off due to seasonal changes, or something worse. A rise of 2.2% is expected.

- Retail PMI: Thursday, 9:10. This purchasing managers’ indicator is showing outright contraction for three months, ending at 44.8 points last time. Another underwhelming number is expected now.

- Eurogroup and ECOFIN Meetings: .Thursday for euro-zone members and Friday for all 28 EU member states. The tension between France and Germany is growing around fiscal policy as well as monetary policy. France wants Germany to spend more, while Germany wants France to balance its budgets. In addition, the next moves around Greece are unclear and the demand that Britain pay back money to the EU is also a hot topic. Statements coming out of these meetings often stir markets.

- ECB rate decision: Thursday, decision at 12:45, press conference from 13:30. No changes are expected in rates, as the ECB stated they have “reached their lower bound”. The main lending rate stands at +0.05% and the deposit rate at -0.20%. The big question is: how far is the ECB willing to go in order to expand its balance sheet? ABS is probably not enough. Buying corporate bonds has been floated, and outright QE, buying sovereign bonds is a delicate issue for German policymakers. While Japan added QE, this may not be enough to counter the end of the same program in the US. Will Draghi drop a hint of a wider, faster expansion of the balance sheet? If so, it could significantly hurt the euro, but he is more likely to refrain for this for now, given his known discord with Bundesbank president Jens Weidmann.

- German Industrial Production: Friday, 7:00. Similar to factory orders, Germany’s output bad disappointed with a fall of 4% in August. And also here, a rebound of 2.1% is expected, but nothing is guaranteed.

- German Trade Balance: Friday, 7:00. Germany’s huge trade surplus is keeping the euro big. After printing 17.5 billion euros in August, a higher level of 18.3 billion is expected for September.

- French Industrial Production: Friday, 7:45. French industrial output is more stable, but not necessarily better. It remained flat in August and is expected to slide for September.

- French Trade Balance: Friday, 7:45. Contrary to Germany, the other core country has a deficit, reaching 5.8 billion last month. A slide to 5.2 billion is expected.

* All times are GMT

EUR/USD Technical Analysis

Euro/dollar began the week with a climb to 1.2775, but after a second attempt to break higher, the pair fell sharply, losing the 1.2660 line (mentioned last week). It then continued lower, eventually reaching a new low of 1.2586 but eventually closed at 1.2523, above the all important round number of 1.25.

Live chart of EUR/USD: [do action=”tradingviews” pair=”EURUSD” interval=”60″/]

Technical lines from top to bottom:

1.33 was a swing low earlier in the year and works as distant resistance at the moment. 1.31 worked in both direction for quite some time.

1.3050 serves as a minor line before the key line: 1.30, which is more than a round number. The pair bounced off this line before making the big fall.

Below 1.30, we find 1.2960 which capped the pair’s recovery attempts after it fell to lower ground. The 1.2920 level was the initial low and should be watched as well.

1.2850 worked as support in September and later capped the pair.1.2775 proved to be a stubborn top in October 2014 and is the important resistance line to the upside.

1.27 is a round number and also worked as resistance to a recovery attempt. This is followed by 1.2660 – which marks the beginning of long term uptrend support.

Below, 1.2570 is the initial low seen in October and now a line of resistance. The next line is critical: of 1.25, which is USD/EUR at 0.80. The pair flirted with this line and even dipped below it in October. This is key support.

Even lower, 1.2445 was a swing high in August 2012 and it is followed by 1.2385, which was stubborn resistance around the same time.

1.2250 served as support several times in that summer, and 1.2170 was the “shoulder” in the inverse H&S pattern around the same time. The last line is the 2012 low of 1.2040.

Downtrend resistance

As the thick black line shows, the pair is trading under downtrend resistance since mid October. This line should be watched in recovery attempts.

Here is closer look at recent movements via the hourly chart:

I remain bearish EUR/USD

The euro-zone is on the verge of recession, suffering from very low inflation and with a central bank that is looking for ways to expand its balance sheet. In the US, balance sheet expansion has ended, the economy advances nicely and the next move is a rate hike. Is all this already priced in after a fall of over 10% from May? Probably not. Despite a lower value of the euro in recent months, inflation hasn’t picked up. The euro area needs an even weaker euro, and the central bank can engineer it lower.

In our latest podcast, we review November’s big event and run down the recent ones:

Subscribe to our podcast on iTunes.

Further reading:

- For a broad view of all the week’s major events worldwide, read the USD outlook.

- For the Japanese yen, read the USD/JPY forecast.

- For GBP/USD (cable), look into the British Pound forecast.

- For the Australian dollar (Aussie), check out the AUD to USD forecast.

- USD/CAD (loonie), check out the Canadian dollar forecast

- For the kiwi, see the NZDUSD forecast.