EUR/USD has edged higher in Tuesday trading, as the euro trades close to the 1.37 line in the European session. In economic news, French and German inflation data was weak, but within market expectations. Eurozone Industrial Production will be released later in the day. Over in the US, Tuesday’s key events include Core Retail Sales and Retail Sales.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

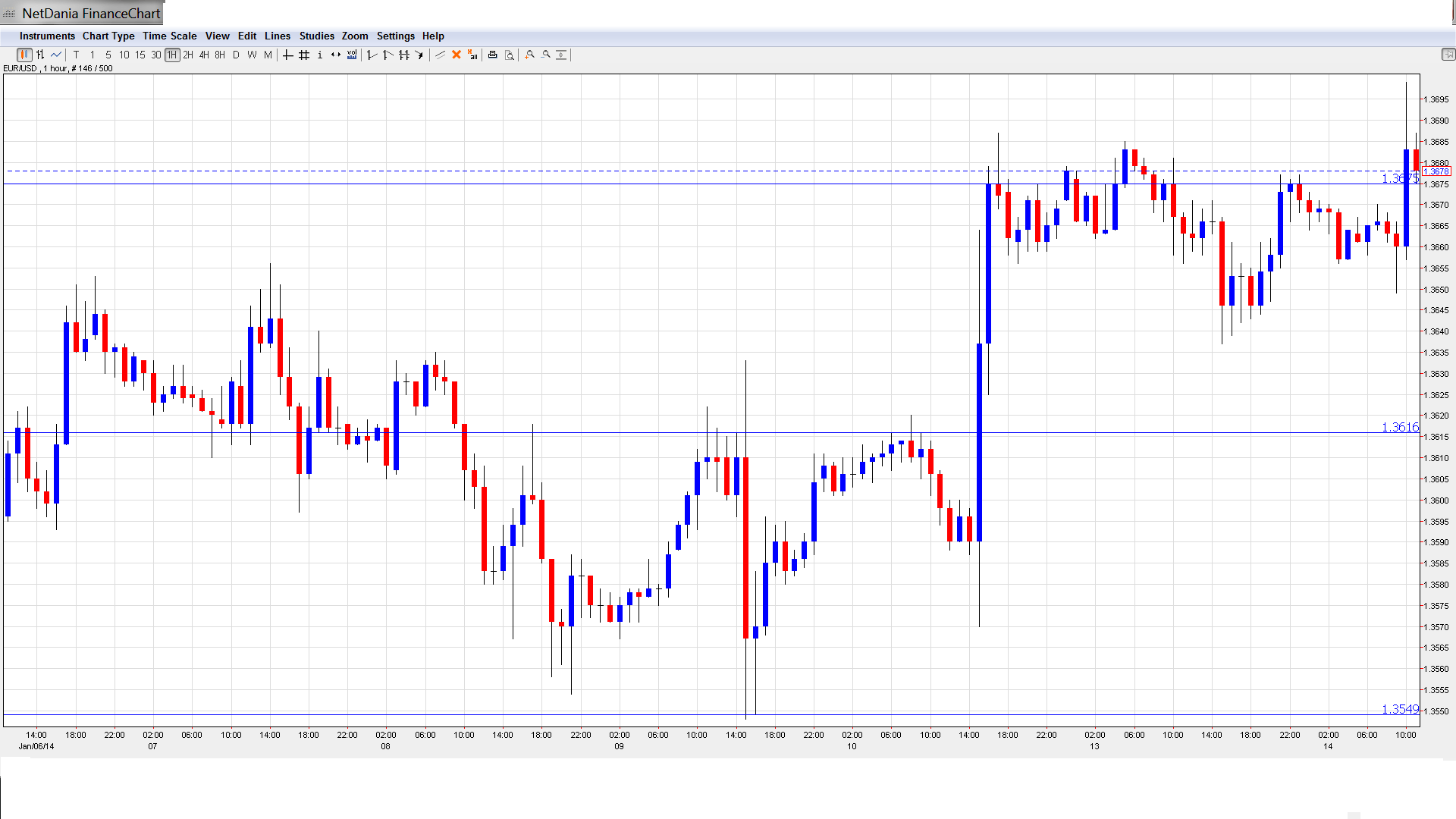

EUR/USD Technical

- EUR/USD was steady in the Asian session, consolidating at 1.3660. The pair has edged higher early in the European session.

Current range: 1.3615 to 1.3675.

Further levels in both directions:

- Below: 1.3615, 1.3550, 1.3450, 1.34, 1.3320, 1.3240 and 1.3175.

- Above: 1.3675, 1.3710, 1.3800, 1.3832, 1.3940 and 1.4036.

- On the upside, 1.3675 is under strong pressure. 1.3710 follows.

- 1.3615 is providing support. 1.3550 is next.

EUR/USD Fundamentals

- 7:00 German WPI. Exp. 0.4%. Actual 0.4%.

- 7:00 French WPI. Exp. 0.4%. Actual 0.3%.

- 10:00 Eurozone Industrial Production. Exp. 1.6%.

- 12:30 US NFIB Small Business Index. Exp. 93.2 points.

- 13:30 US Core Retail Sales. Exp. 0.4%.

- 13:30 US Retail Sales. Exp. 0.2%.

- 13:30 US Import Prices. Exp. 0.3%.

- 15:00 US Business Inventories. Exp. 0.4%.

- 17:45 US FOMC Member Charles Plosser Speaks.

- 18:20 US FOMC Member Richard Fisher Speaks.

*All times are GMT

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Non-Farm Payrolls take a hit: US employment data had a promising start in 2014, but Friday’s Non-Farm Payrolls was a disaster, posting its lowest gain since May 2012. The key employment indicator dropped to just 74 thousand, down from 203 thousand a month earlier. This was nowhere near the estimate of 196 thousand. Although the unemployment rate dropped to 6.7%, this was due to a drop in the participation rate. The participation rate dropped to 62.8%, its lowest since 1978. This figure points to a worrying trend of a jobless US recovery.

- Taper likely to continue despite weak NFP: Last week’s dismal Non-Farm Payrolls report may create some concern in the markets, but is unlikely to change the Federal Reserve’s path of tapering QE, which it started just this month. In December, outgoing Fed chair Bernard Bernanke strong hinted that the Fed planned to wind up QE by the end of 2014, reducing the asset-purchase program by increments of $10 billion at each meeting. The Fed next meets for a policy meeting on January 28, and the question is will the Fed reduce QE by another $10 billion, down to $65 billion each month. Most analysts feel that one bad employment report will not affect the taper schedule and we will see another reduction in QE at the next meeting.

- ECB holds course: The first ECB rate announcement of 2014 was a non-event, as the central bank held the benchmark rate at a record low of 0.25% last week. Mario Draghi’s press conference did not make waves and move the currency markets, as has often been the case in the past. Draghi said that monetary policy will remain accommodative for as long as is needed to help the Eurozone economy recover, and that interest rates will likely remain at present or lower levels for the foreseeable future. If growth and inflation indicators continue to look weak, the ECB may have to take action at its next meeting in February.

- Light at end of Portuguese bailout tunnel: Portugal is scheduled to end its bailout program in May, which saw the country receive a rescue package from the EU and the IMF which amounted to EUR 78 billion. Portuguese Treasury Minister Castelo Branco is hopeful that the country will be able to sell bonds through auctions before May. Until now, Portugal has been relying on banks to sell bonds. The end of the bailout should allow Portugal full access to debt markets. Ireland, which exited a bailout program in December, became the first Eurozone member to do so since the debt crisis which rocked the bloc in 2009.