EUR/USD has reversed directions in Thursday trading, posting modest gains. The pair is trading in the low-1.36 range in the European session. In economic news, Eurozone CPI posted a gain of 0.8%, matching the estimate. Core CPI gained 0.7%, missing its estimate. In the US, it’s a busy day with three key events – Core CPI, Unemployment Claims and the Philly Fed Manufacturing Index. As well, Fed chair Bernard Bernanke will deliver a speech in Washington.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

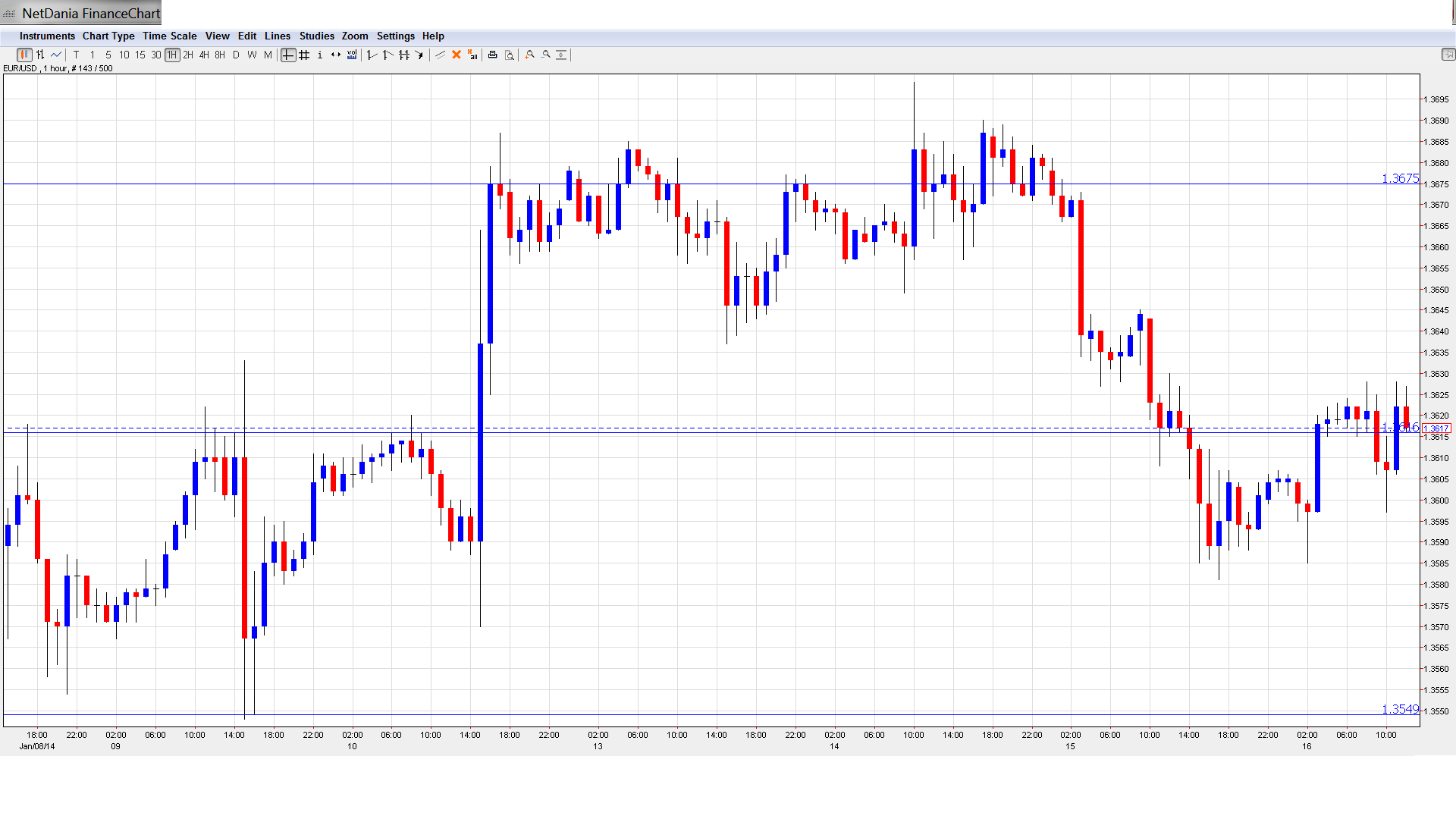

EUR/USD Technical

- EUR/USD traded slightly above the 1.36 line for most of the Asian session, consolidating at 1.3608. The pair has edged higher early in the European session.

Current range: 1.3615 to 1.3675.

Further levels in both directions:

- Below: 1.3615, 1.3550, 1.3450, 1.34, 1.3320, 1.3240 and 1.3175.

- Above: 1.3675, 1.3710, 1.3800, 1.3832, 1.3940 and 1.4036.

- On the downside, 1.3615 is under strong pressure. 1.3550 follows.

- 1.3675 is the first line of resistance. 1.3710 is next.

EUR/USD Fundamentals

- 7:00 German Final CPI. Exp. 0.4%. Actual 0.4%.

- 9:00 ECB Monthly Bulletin.

- 9:00 Italian Trade Balance. Exp. 3.88B. Actual 3.09B.

- 10:00 Eurozone CPI. Exp. 0.8%. Actual 0.8%.

- 10:00 Eurozone Core CPI. Exp. 0.9%. Actual 0.7%.

- 10:00 German Buba President Weidmann Speaks.

- 13:30 US Core CPI. Exp. 0.1%.

- 13:30 US CPI. Exp. 0.3%.

- 13:30 US Unemployment Claims. Exp. 327K.

- 13:30 US Treasury Secretary Jack Lew Speaks.

- 14:00 US TIC Long-Term Purchases. Exp. 42.3B.

- 15:00 US Philly Fed Manufacturing Index. Exp. 8.8 points. See how to trade this event with EUR/USD.

- 15:00 NAHB Housing Market Index. Exp. 58 points.

- 15:30 US Natural Gas Storage. Exp. -296B.

- 16:10 US Fed Chair Bernard Bernanke Speaks.

*All times are GMT

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- US PPI bounces higher: Low inflation levels in the US remain a concern, as this is an indication of an underperforming economy. On Tuesday, the Producer Price Index posted a gain of 0.4%, reversing directions after three consecutive declines. On Wednesday, Chicago Fed President Charles Evans said that the low rate of U.S. inflation is “both puzzling and worrisome,” and enough reason to maintain low interest rates, even if the employment picture continues to brighten. We’ll get another look at inflation indicators on Thursday, as the US releases Core CPI and CPI.

- US retail numbers in all directions: US retail sales numbers painted a mixed picture on Tuesday. Retail Sales dropped sharply to 0.2%, down from 0.7% in November. However, this figure matched the forecast. Core Retail Sales took the opposite route, jumping to 0.7%, compared to 0.4% the month before. This easily beat the estimate of 0.4%. Retail sales are an important gauge of consumer spending, and these numbers will have to improve if the recovery is to pick up speed.

- Taper likely to continue despite weak NFP: Last week’s dismal Non-Farm Payrolls report may create some concern in the markets, but is unlikely to change the Federal Reserve’s path of tapering QE, which it started just this month. In December, outgoing Fed chair Bernard Bernanke strong hinted that the Fed planned to wind up QE by the end of 2014, reducing the asset-purchase program by increments of $10 billion at each meeting. The Fed next meets for a policy meeting on January 28, and the question is will the Fed reduce QE by another $10 billion, down to $65 billion each month. Most analysts feel that one bad employment report will not affect the taper schedule and we will see another reduction in QE at the next meeting.

- Steady course for ECB: The first ECB rate announcement of 2014 was a non-event, as the central bank held the benchmark rate at a record low of 0.25% last week. Mario Draghi’s press conference did not make waves and move the currency markets, as has often been the case in the past. Draghi said that monetary policy will remain accommodative for as long as is needed to help the Eurozone economy recover, and that interest rates will likely remain at present or lower levels for the foreseeable future. If growth and inflation indicators continue to look weak, the ECB may have to take action at its next meeting in February.