EUR/USD is steady in Wednesday trading, as the pair continues to trade in the mid-1.36 range in the European session. In economic news, German releases continue to shine, as German Consumer Climate climbed for the third straight month. However, Eurozone M3 Money Supply slipped badly in December. Over in the US, all eyes will be on the Federal Reserve policy meeting, with expectations that the Fed will go ahead with another QE taper.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

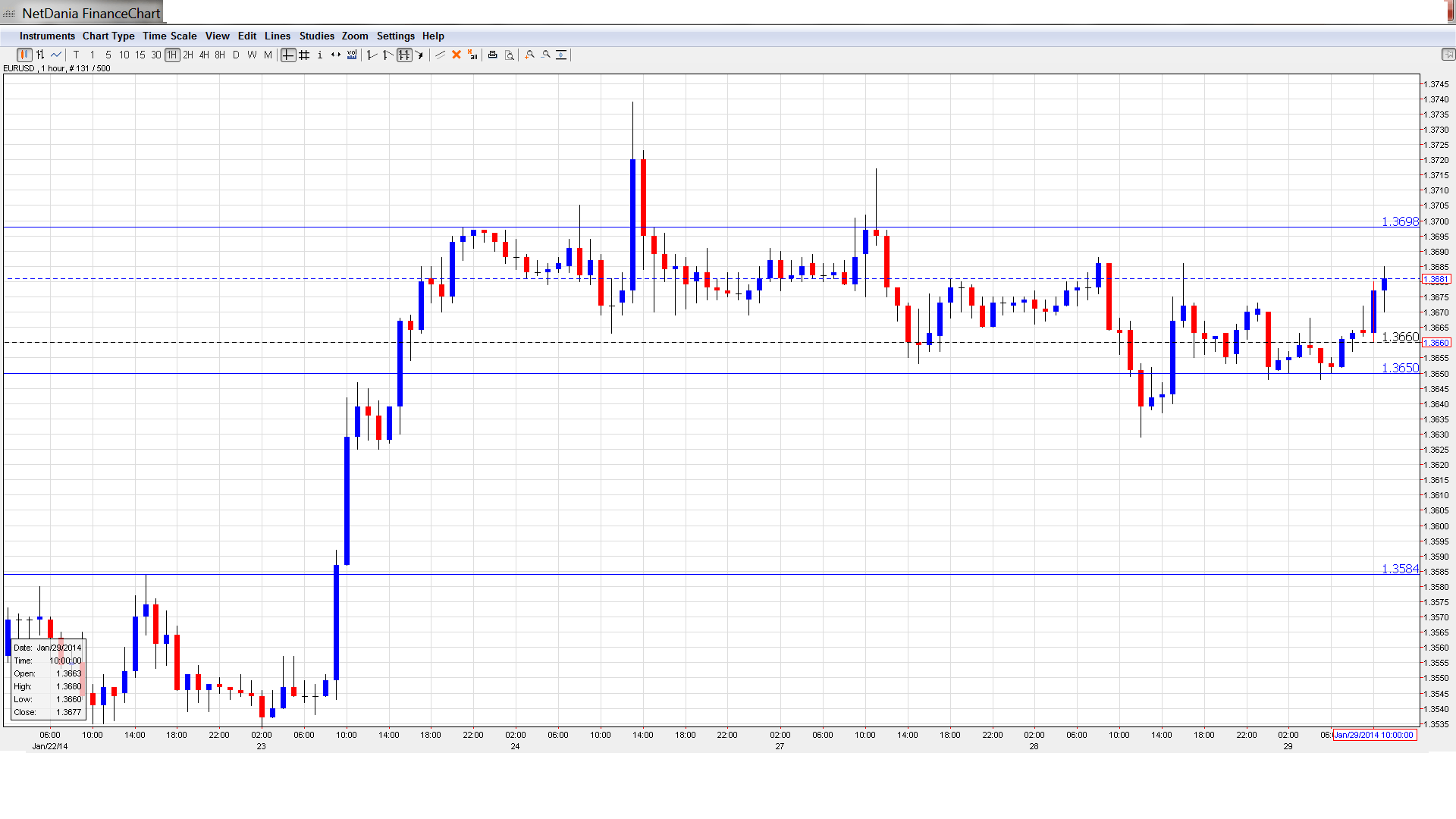

EUR/USD Technical

- EUR/USD was steady for most of the Asian session, staying close to the 1.3660 line. The pair has edged higher early in the European session.

Current range: 1.3650 to 1.37.

Further levels in both directions:

- Below: 1.3650, 1.3580, 1.3515, 1.3450, 1.34, 1.3320, 1.3240, 1.3175 and 1.31.

- Above: 1.37, 1.3800, 1.3832 and 1.3940.

- 1.3650 has reverted to a support level. 1.3580 is stronger.

- 1.3700 is weak resistance. 1.3800 follows.

EUR/USD Fundamentals

- 2:00 US President Barak Obama Delivers State of the Union Address.

- 7:00 GfK German Consumer Climate. exp. 7.8, actual 8.2 points.

- 9:00 Eurozone M3 Money Supply. exp. 1.7%, actual 1.0%.

- 9:00 Eurozone Private Loans. exp. -2.3%, actual -2.3%.

- Tentative – German 10-year Bond Auction.

- 15:30 US Crude Oil Inventories. Exp. 2.2M.

- 19:00 US FOMC Statement.

- 19:00 US Federal Funds Rate. Exp. <0.25%.

*All times are GMT

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Will Fed pull the taper trigger? The markets are waiting for the Federal Reserve’s policy meeting on Wednesday, with most analysts predicting that the Fed will go ahead and reduce QE for a second straight month. Such a move would be an important vote of confidence in the US economy, and could give a boost to the US dollar against its major rivals. This policy meeting will be chairman Bernard Bernanke’s last hurrah, as Janet Yellen takes over the reins of the Fed on February 1.

- German Consumer Climate Improves: The German locomotive is chugging along, much to the delight of the markets. Gfk German Consumer Climate rose for the third straight month, climbing to 8.2 points in December, up from 7.6 a month earlier. The strong reading beat the estimate of 7.8 points. This release comes on the heels of German Ifo Business Climate, which topped the 110 level. The readings show that German businesses and consumers are optimistic about the economy as we begin 2014. Germany is the Eurozone’s largest economy, and the region will need Germany to lead the way to an economic recovery.

- US Housing Numbers Slide: The US housing sector is showing some weakness. New Home Sales dropped sharply in December to 414 thousand, down from 464 thousand a month earlier. This was nowhere near the estimate of 457 thousand. This follows a disappointing Existing Home Sales release last week. The key indicator dropped to 4.87 million, down from 4.90 million a month earlier and shy of the estimate of the 4.94 million. This was the indicator’s fourth straight drop. The markets will be hoping for better news from Pending Home Sales on Thursday. A third straight housing reading below the estimate could weigh on the dollar.

- IMF warns about deflation in Eurozone: Eurozone inflation indicators continue to point to weak inflation, and the situation as deteriorated to such an extent that the IMF has voiced its concern about the danger of deflation in Europe. This was seen in a report published by the organization as well as in a speech by IMF Managing Director Christine Lagarde in Davos. While the ECB seems concerned with low inflation and not outright deflation, any further deterioration could push the ECB to set a negative deposit rate as soon as March 2014. This is a primary source of euro vulnerability.