EUR/USD has edged lower, dropping below the 1.36 line in Wednesday trading. In economic news, Eurozone Retail Sales jumped 1.5%, reversing directions after two consecutive declines. The Eurozone Unemployment Rate remained steady at 12.1%. German Factory Orders posted a sharp gain, while German Trade Balance improved, but fell short of the estimate. In the US, today’s highlight is the ADP Non-Farm Employment Change. The markets are expecting a lower reading for December. As well, the Federal Reserve will release the minutes of its most recent policy meeting.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

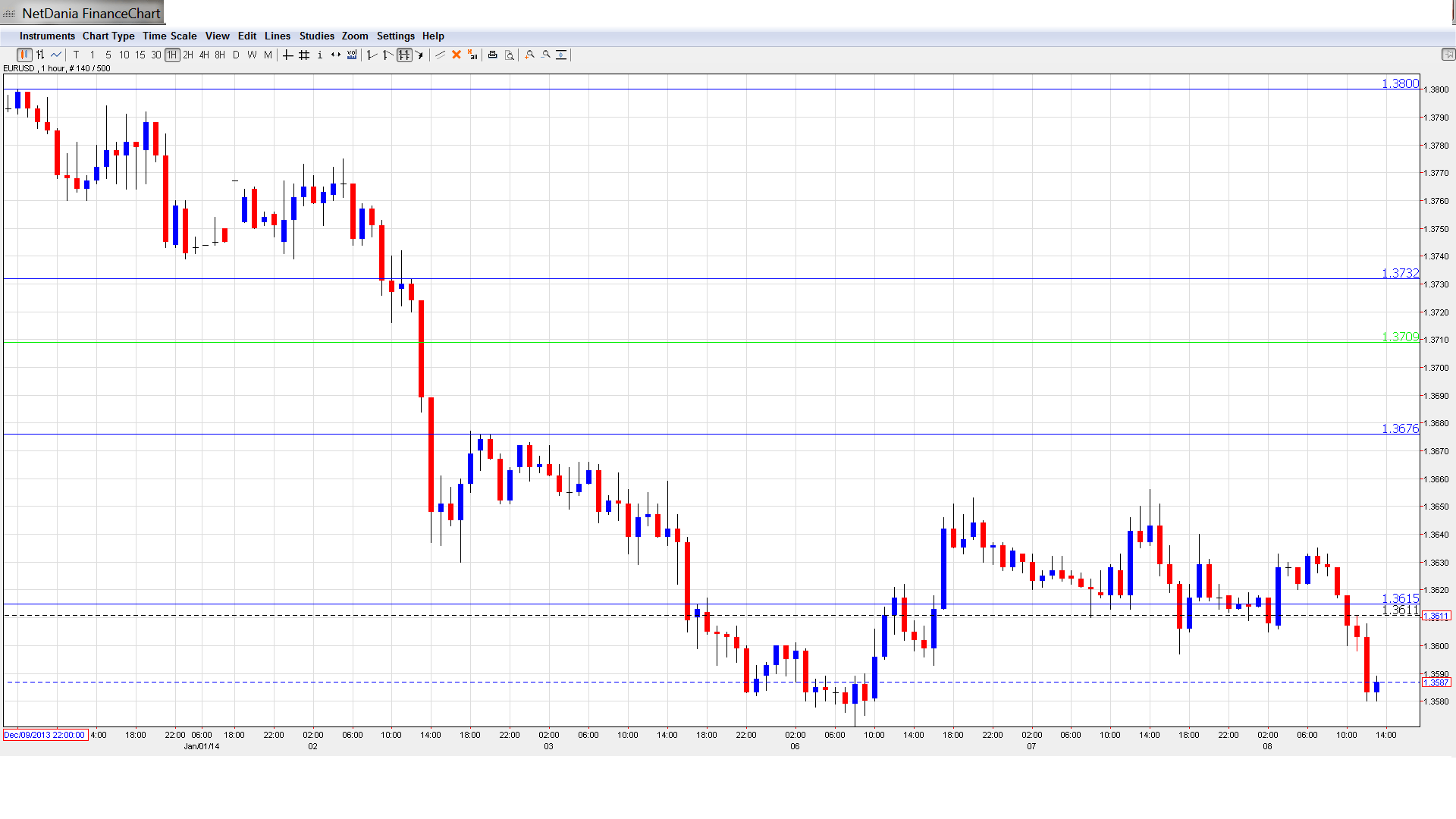

EUR/USD Technical

- EUR/USD edged higher in the Asian session, touching a high of 1.3635 before consolidating at 1.3618. The pair has dropped below the 1.36 line in the European session.

Current range: 1.3525 to 1.3615.

Further levels in both directions:

- Below: 1.3525, 1.3440, 1.34, 1.3320, 1.3240 and 1.3175.

- Above: 1.3615, 1.3675, 1.3710, 1.3800, 1.3832, 1.3940 and 1.4036.

- 1.3615 has reverted to a resistance role as the euro loses ground. 1.3675 is stronger.

- On the downside, there is support at 1.3525.

EUR/USD Fundamentals

- 7:00 German Trade Balance. Exp. 18.9B, actual 17.8B.

- 9:00 Italian Monthly Unemployment Rate. Exp. 12.6%, actual 12.7%.

- 10:00 Eurozone Retail Sales. Exp. 0.2%, actual 1.4%.

- 10:00 Eurozone Unemployment Rate. Exp. 12.1%, Actual 12.1%.

- 11:00 German Factory Orders. Exp. 1.2%. Actual 2.1%.

- 13:15 ADP Non-Farm Employment Rate. Exp. 199K. See

how to trade this event with USD/JPY. - 15:30 US Crude Oil Inventories. Exp. -1.6M.

- 18:01 US 10-year Bond Auction.

- 19:00 US FOMC Meeting Minutes.

- 20:00 US Consumer Credit. Exp. 14.8B.

*All times are GMT

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Euro hits early January storm: The euro has not had much to cheer about in 2014, as the common currency has lost close to two cents in the past week. Surprisingly, the currency hasn’t received a boost from recent Eurozone data, which has generally looked sharp. German and Eurozone retail sales jumped in December, and German Unemployment Change sparkled with a sharp drop. As well, recent Spanish numbers have impressed. At the same time, Italy and France are struggling, and inflation and growth in the bloc remain subdued.

- German numbers sparkle: Germany started off 2014 with sharp numbers, as Retail Sales improved by 1.5%, reversing a downtrend of two straight declines. This beat the estimate of 0.5%. Unemployment Change was very sharp, declining by 15 thousand, the first decline in five months. On Wednesday, German Factory Orders jumped 2.1%, easily beating the estimate of 1.2%. Trade surplus widened to 17.8 billion euros, but this missed the estimate of 18.9 billion. The strong numbers we have seen in January are indicative of an improving German economy, which bodes well for the Eurozone.

- Eurozone inflation remains weak: Eurozone CPI showed more of the same in December, posting a gain of 0.8%. This is well below the ECB inflation target of 2%. The central bank has responded with rate cuts which have lowered the benchmark rate to a record low of 0.25%, but inflation hasn’t risen as hoped. The ECB will meet and announce a rate decision on Thursday.

- Senate confirms Yellen: As expected, the US Senate confirmed Susan Yellen as chair of the Federal Reserve by a wide margin on Monday. Yellen becomes the first woman to head the powerful central bank. She has been a strong supporter of outgoing chair Bernard Bernanke, who lowered interest rates and implemented a QE program in order to boost a struggling US economy. The Fed has now started to trim the $85 billion QE scheme, with a $10 billion cut as of January. We could see another taper at the next Fed policy meeting in late January. Yellen takes over the helm of the Fed on February 1, and will chair her first policy meeting in March.

- Markets eye US employment releases: The markets are awaiting the ADP Non-Farm Payrolls later on Wednesday, which precedes Unemployment Claims on Thursday and the official NFP release on Friday. NFP can impact the next Fed decision, after 2013 ended with QE tapering. While it was small, the Fed did indeed change policy, and this could have a significant positive impact on the US dollar. With another taper in January a strong possibility, every employment release will be under the market microscope and could impact on the currency markets.

- Dollar outlook for 2014: Many analysts see the dollar strengthening in 2014, but the euro is certainly expected to give a fight. Here is one outlook: 2014 – Conditional Dollar Strength.