EUR/USD continues to move higher, as the pair trades in the high-1.32 range on Tuesday. Later today, a German court will rule on the legality of OMT, the ECB’s bond-buying rescue program. It’s another quiet day in economic news, with no other releases from the Eurozone. In the US, there are just two minor releases on the schedule – the NFIB Small Business Index and Wholesale Inventories.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

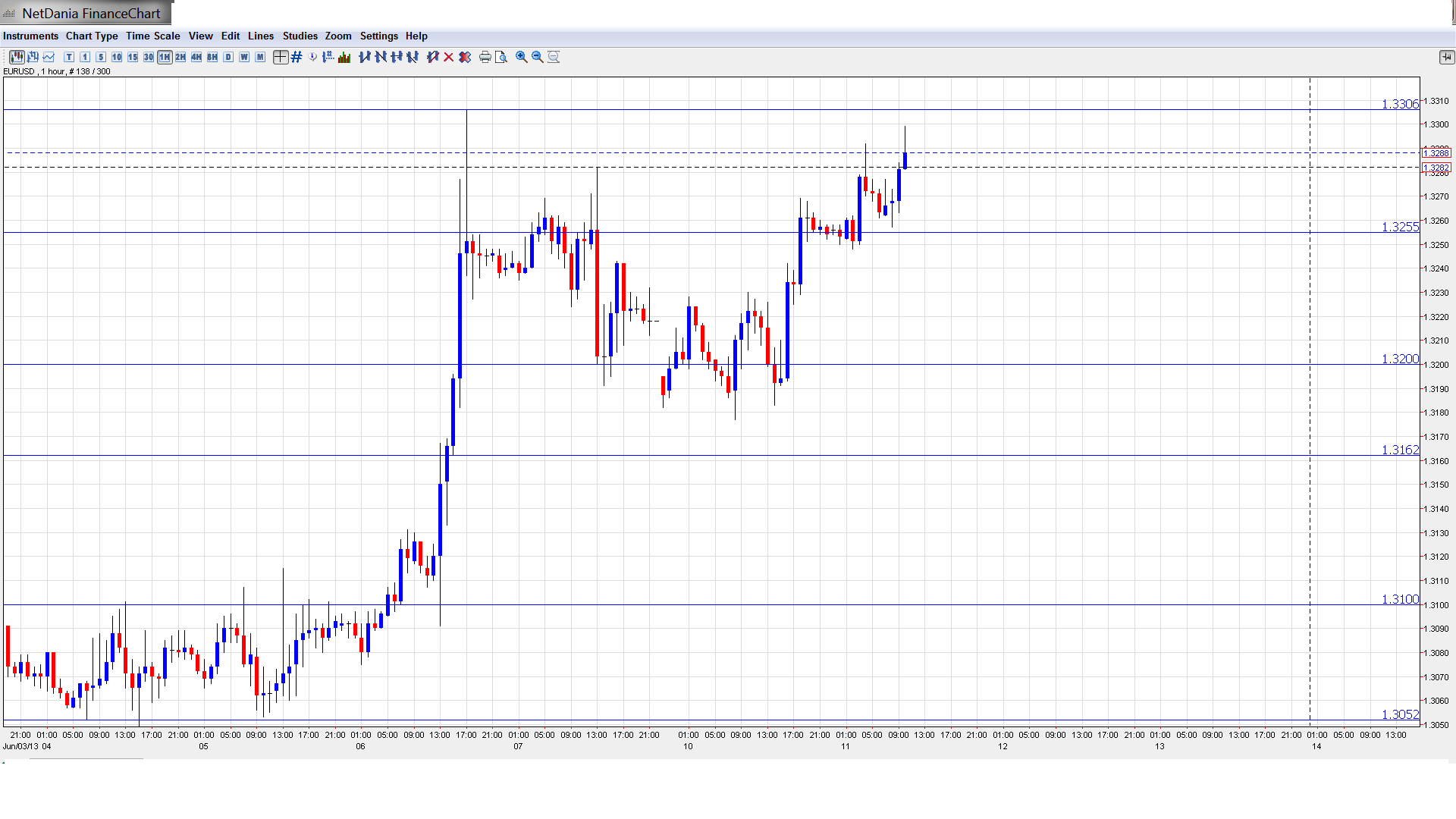

EUR/USD Technical

Asian session: Euro/dollar edged higher, touching a high of 1.3292. The pair consolidated at 1.3267. The pair is unchanged in the European session.

Current range: 1.3255 – 1.3306.

Further levels in both directions:

<img alt=”EUR USD Daily Forecast June 10th” src=”https://www.forexcrunch.com/wp-content/uploads/2013/06/EUR-USD-Daily-Forecast-June-10th-350×196.png” width=”350″ height=”196″ />

<img alt=”EUR USD Daily Forecast June 7″ src=”https://www.forexcrunch.com/wp-content/uploads/2013/06/EUR-USD-Daily-Forecast-June-7-350×196.png” width=”350″ height=”196″ /> <img alt=”EUR USD Daily Forecast June 6″ src=”https://www.forexcrunch.com/wp-content/uploads/2013/06/EUR-USD-Daily-Forecast-June-6-350×196.png” width=”350″ height=”196″ /> <img alt=”EUR USD Daily Forecast June 4″ src=”https://www.forexcrunch.com/wp-content/uploads/2013/06/EUR-USD-Daily-Forecast-June-4-350×196.png” width=”350″ height=”196″ /> <img alt=”EUR USD Daily Forecast May31″ src=”https://www.forexcrunch.com/wp-content/uploads/2013/05/EUR-USD-Daily-Forecast-May31-350×196.png” width=”350″ height=”196″ /> <img alt=”EUR USD Daily Forecast May30″ src=”https://www.forexcrunch.com/wp-content/uploads/2013/05/EUR-USD-Daily-Forecast-May30-350×196.png” width=”350″ height=”196″ /> <img alt=”EUR USD Daily Forecast May29″ src=”https://www.forexcrunch.com/wp-content/uploads/2013/05/EUR-USD-Daily-Forecast-May29-350×196.png” width=”350″ height=”196″ /> <img alt=”EUR USD Daily Forecast May28″ src=”https://www.forexcrunch.com/wp-content/uploads/2013/05/EUR-USD-Daily-Forecast-May28-350×196.png” width=”350″ height=”196″ /> <img alt=”EUR USD Daily Forecast May27″ src=”https://www.forexcrunch.com/wp-content/uploads/2013/05/EUR-USD-Daily-Forecast-May271-350×196.png” width=”350″ height=”196″ />

Below: 1.3255, 1.32, 1.3160, 1.31, 1.3050, 1.30, 1.2940, 1.2890, 1.2840, 1.28, 1.2750 and 1.27.

Above: 1.3306, 1.3350, 1.34, 1.3480, 1.3580 and 1.3710.

1.3255 is providing weak support. This is followed by the round number of 1.32. 1.3306 is the next resistance line. 1.3350 is stronger.

Euro moves close to 1.33 line – click on the graph to enlarge.

EUR/USD Fundamentals

Day 1 – German Constitutional Court Ruling .11:30 US NFIB Small Business Index. Exp. 93.4 points.

14:00 US Wholesale Inventories. Exp. 0.1%.

For more events and lines, see the Euro to dollar forecast

EUR/USD Sentiment

OMT heads to court: The Federal Constitutional Court, Germany’s highest court, will review the ECB’s OMT (Outright Monetary Transactions) program on Tuesday. OMT is a rescue program which enables the ECB to buy bonds from Eurozone members whose economies are struggling. Last week, ECB head Mario Draghi stated that OMT had helped bring stability to the global markets and was a key monetary policy measure. His upbeat view lies in sharp contrast to that of Bundesbank President Jens Weidmann, who voted against the program. In previous cases involving the legality of ECB rescue packages, the German court has given its approval, but has not hesitated to add conditions. So we can expect the court to give the nod to OMT, although there could some strings attached.S&P revises US outlook : The S&P ratings agency revised its US rating from negative to stable, which means that another downgrade in the next two years has less than a 33% chance of occuring . The agency said that a key factor in its decision was the agreement reached in Congress to avoid the fiscal cliff, which would have resulted in $600 billion in tax increases and spending cuts, and could have pushed the US economy into recession. Back in 2011, S&P cut the US credit rating from AAA to AA, and the threat of another downgrade has been hanging over the markets since then. So this development will improve market sentiment and could give a boost to the US dollar.ECB stays the course, euro jumps: The markets have become accustomed to volatility from the euro after ECB policy meetings, and last week was no exception. The euro gained about 150 points after Thursday’s policy meeting, and tested the 1.33 level before retracting. The ECB held a steady course, maintaining the benchmark rate at 0.50% and deposit rates at 0% . ECB President Mario Draghi downgraded the forecast for Eurozone growth in 2013 from 0.6% to 0.5%. However, for 2014, Draghi hiked the forecast from 1.0% to 1.1%. The markets seemed to focus on the positive aspect of Draghi’s comments, and the euro surged against the US dollar, which was broadly weaker against the major currencies .US employment numbers a mix: US Non-Farm Payrolls wrapped up the week on a positive note, as the key employment indicator rose from 165 thousand to 175 thousand. This was above the market forecast of 167 thousand. However, the Unemployment Rate rose to 7.6% from 7.5%. Earlier in the week, Unemployment Claims practically matched the estimate, but the markets responded with a lukewarm reaction. Employment numbers have added significance now that speculation has increased that the Fed could well wind up QE in the next few months, if the recovery seems to be deepening. However, the Fed has stated that it won’t act before employment numbers improve, so we can expect QE to continue if US employment numbers don’t show significant improvement.Is Germany headed up, down, or both? Almost lost in all of the excitement after the ECB policy meeting last week was a very weak German manufacturing release. German Factory Orders slumped, falling from 2.2% to -2.6%, its worst showing since November 2012. On Friday, German Trade Balance remained steady at EUR 17.7 billion, well above the estimate of EUR 16.5 billion. There was more good news as German Industrial Production rose 1.8%, blowing past the estimate of 0.0%. Germany is the locomotive of the Eurozone economy, and the country will need to post continuous solid releases if the Eurozone is to get back on track.