EUR/USD is under pressure in Thursday trading, as the pair trades in the low-1.30 range. The pair lost more ground on Wednesday, after ECB President Mario Draghi said that the central bank’s monetary policy will remain loose. In the US, Final GDP was a disappointment, falling well below the estimate. Looking at Thursday’s releases, German Unemployment Change posted a sharp drop. Italian 10-year bonds continue to rise, and posted an average yield of 4.55% in the Thursday auction. In the US, there are two major releases – Unemployment Claims and Pending Home Sales.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

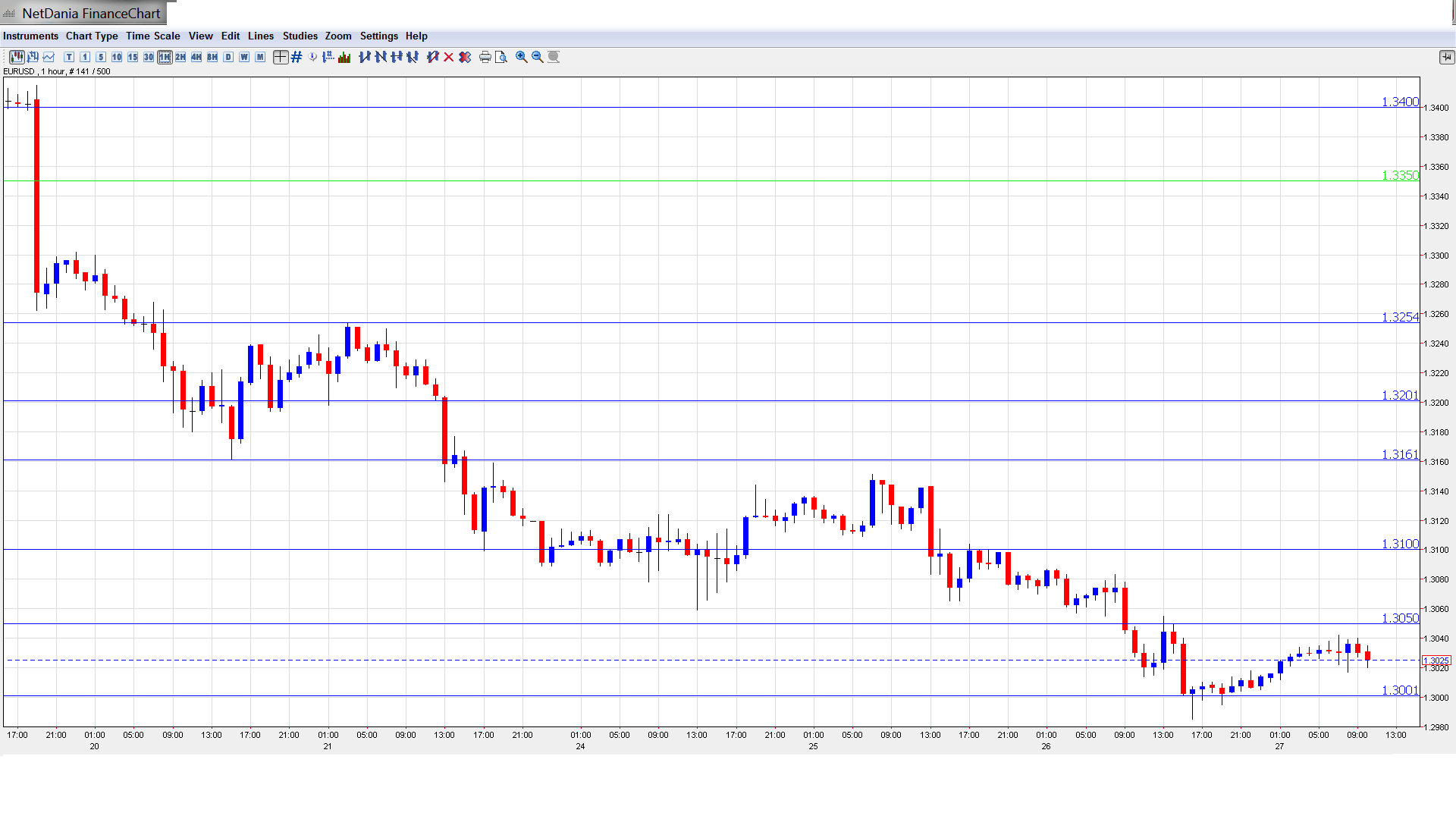

EUR/USD Technical

- Asian session: Euro/dollar was steady, touching a low of 1.3017 and consolidating around 1.3030. The pair is unchanged in the European session.

Current range: 1.3000 – 1.3050.

Further levels in both directions:

- Below: 1.30, 1.2940, 1.2890, 1.2840, 1.28, 1.2750 and 1.27.

- Above: 1.3050, 1.31, 1.3160, 1.32, 1.3255, 1.3350, 1.34, 1.3434, 1.3480

- The important level of 1.30 is providing weak support. 1.2940 is stronger.

- 1.3050 is a weak resistance line. This is followed by 1.31.

Euro remains under pressure after Draghi comments – click on the graph to enlarge.

EUR/USD Fundamentals

- 6:00 German Import Prices. Exp. -0.1%. Actual -0.4%.

- 7:55 German Unemployment Change. Exp. 7K. Actual -12K. See how to trade this event with EUR/USD.

- 8:00 Eurozone M3 Money Supply. Exp. 2.9%. Actual 2.9%.

- 8:00 Eurozone Private Loans. Exp. -0.8%. Actual -1.1%.

- 8:10 Eurozone Retail PMI. Actual 49.1 points.

- 9:14 Italian 10-year Bond Auction. Actual 4.55%.

- Day 1 – EU Economic Summit.

- 12:30 US Unemployment Claims. Exp. 347K.

- 12:30 US Core PCE Price Index. Exp. 0.1%.

- 12:30 US Personal Spending. Exp. 0.3%.

- 12:30 US Personal Income. Exp. 0.2%.

- 14:00 US Pending Home Sales. Exp. 1.1%.

- 14:00 US FOMC Member William Dudley Speaks.

- 14:30 US FOMC Member Jerome Powell Speaks.

- 14:30 US Natural Gas Storage. Exp. 89B.

For more events and lines, see the Euro to dollar forecast

EUR/USD Sentiment

- ECB’s Accommodative Stance to Continue: ECB President Mario Draghi spoke on Tuesday in Paris to the French parliament. Draghi reiterated that the ECB’s monetary policy would remain accommodative for now. He said that he expects the Eurozone to recover in the second half of 2013, but that the recovery would be “gradual but fragile”. The markets have heard these comments from Draghi and other ECB policymakers before, but based on the economic data we are seeing from the Eurozone, there is skepticism if the economy in Europe will indeed improve in the near future.

- Strong US Numbers Boost Dollar: US releases impressed the markets on Tuesday, with all three key releases looking sharp. Core Durable Goods rose 0.7%, easily surpassing the estimate of 0.0%. CB Consumer Confidence shot up to a multi-year high, at 81.4 points. The estimate stood at 75.2 points. New Home Sales came in at 476 thousand, well above the estimate of 462 thousand. Manufacturing data, often a sore spot, also looked good as the Richmond Manufacturing Index jumped to 8 points. All in all, it was an excellent day for the US, and the dollar responded by posting gains against the struggling euro. The news was not as good on Wednesday, as US GDP for Q1 rose 1.8%, well short of the 2.4% estimate. However, the markets shrugged of this weak reading and the dollar remains strong against the euro.

- Fed Backtracking on QE?: After Federal Reserve Chair Bernard Bernanke said last week that the Fed was planning to scale down QE, the US dollar surged. However, global stock markets, including those in the US, fell sharply on the news, and the Fed assigned two Federal Reserve Presidents to manage damage control. Dallas’ Richard Fisher declared that “tapering” should not be confused with “tightening” and said that the Fed was not exiting from its accommodative policy action just yet. Minneapolis’ Naraya Kocherlakota reiterated that the Fed was continuing with an expansionary monetary policy event if QE was terminated, and said that the Fed had not turned more hawkish. One could be forgiven for dismissing these statements as little more than linguistic acrobatics, and it’s questionable if the markets will be reassured by these statements, which were clearly aimed at calming nervous investors.

- German data shows improvement: Germany has long been considered the locomotive of Europe, but the number one economy in the Europe has had its share of trouble, as underscored by some weak economic releases. The week did not start off well, as German Ifo Business Climate, a key indicator, came in slightly below the estimate. However, there was better news as German Consumer Climate hit a six-year high. On Thursday, German Unemployment Claims posted a sharp drop of -12 thousand, well below the estimate of 7 thousand. These solid releases will have to continue if the Eurozone is to get back on the road to recovery.

- Greek government faces crisis: Greece is once again facing political turmoil as the smallest party in the governing coalition, the Democratic Left Party, quit on Friday. The reason was the government’s decision to close the state broadcaster as part of its plan to eliminate 15,000 public sector jobs by 2014, as mandated by the bailout agreement. The loss of the Democratic Left leaves the coalition with a razor-thin majority of just three seats. The timing of this crisis is particularly bad, as Greece is due to receive another installment of bailout funds next month. The troika (European Commission, ECB and IMF) are playing down the crisis, saying that the bailout will proceed on schedule. If this proves not to be the case, we could see the euro run into some turbulence.