A slow start to the week seems long behind us, as the euro continues to rally against the dollar. EUR/USD is trading in the high-1.29 range in Thursday’s European session. Will we see a move towards the 1.30 barrier? In economic news, Eurozone Retail PMI looked sharp, hitting an eight-month high. The markets are awaiting the Italian 10-year bond auction. We could see some action from the pair as the US releases three key events later today – Preliminary GDP, Unemployment Claims and Pending Home Sales.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

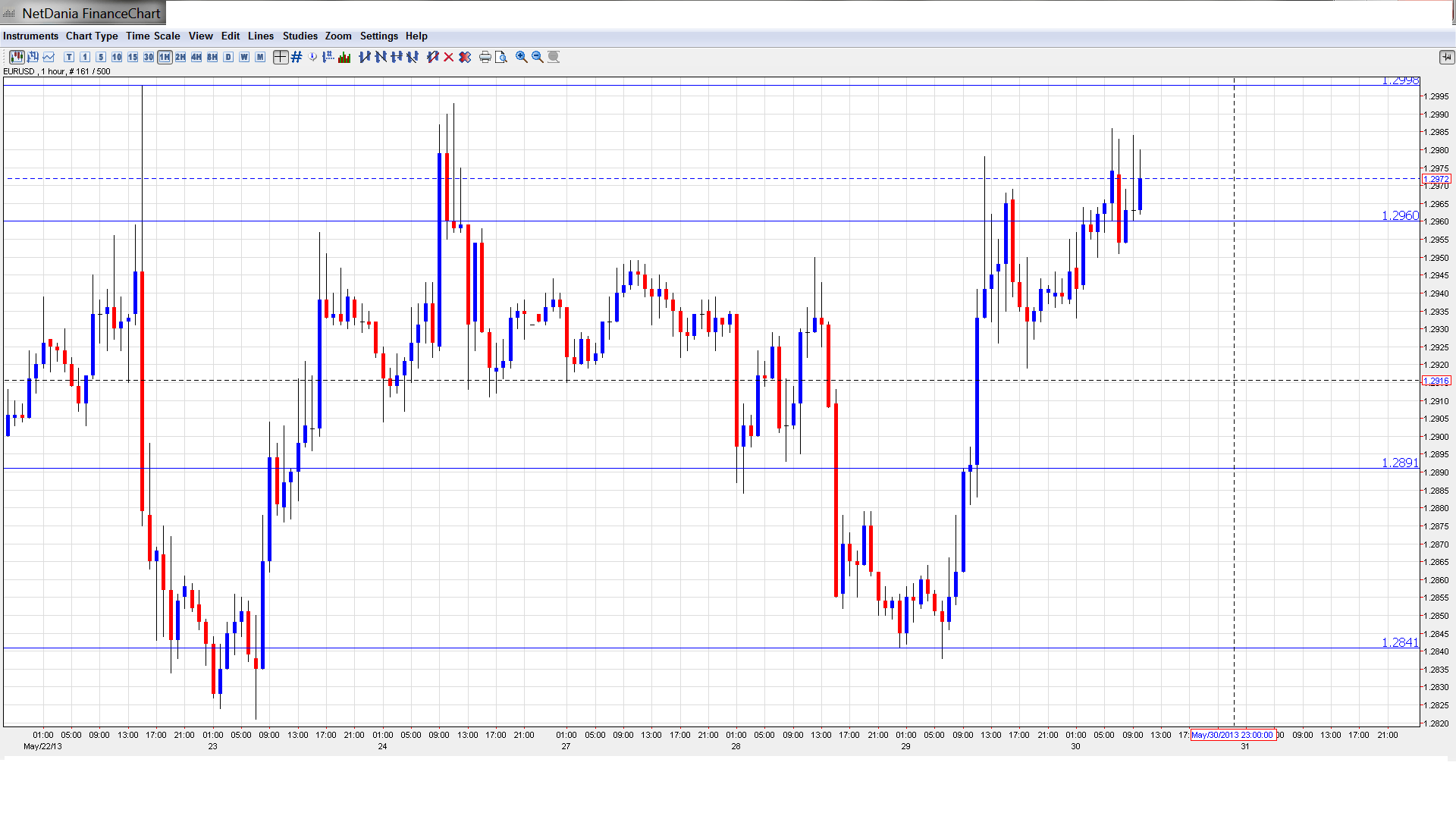

EUR/USD Technical

- Asian session: Euro/dollar showed some upward momentum, touching a high of 1.2986 and consolidating at 1.2969. In the European session, the pair is unchanged.

Current range: 1.2960 – 1.3000.

Further levels in both directions:

- Below: 1.2960, 1.2890, 1.2840, 1.2800, 1.2750, 1.27, 1.2624 and 1.2587.

- Above: 1.30, 1.3050, 1.31, 1.3160 and 1.32, 1.3255, and 1.3290.

- On the upside, 1.30 is providing weak resistance. 1.3050 is next.

- 1.2960 is the next support level. There is stronger support at 1.2890.

Euro continues to climb towards 1.30 – click on the graph to enlarge.

EUR/USD Fundamentals

- 8:10 Eurozone Retail PMI. Actual 46.8 points.

- Tentative: Italian 10-year Bond Auction.

- 12:30 US Preliminary GDP. Exp. 2.5%.

- 12:30 US Unemployment Claims. Exp. 342K.

- 12:30 US Preliminary GDP Price Index. Exp. 1.2%.

- 14:00 US Pending Home Sales. Exp. 1.3%.

- 14:30 US Natural Gas Storage. Exp. 85B.

- 15:00 US Crude Oil Inventories. Exp. -0.8M.

For more events and lines, see the Euro to dollar forecast

EUR/USD Sentiment

- More of a Mix from Germany: On Tuesday, the markets were greeted with dismal German employment numbers. Unemployment Change shot up to 21 thousand, blowing past the estimate of 4 thousand. This was the highest reading since June 2008. There was better news on the inflation front, as Preliminary CPI rebounded nicely and posted a 0.4% gain, surpassing the forecast of 0.2%. Where is the German economy headed? The Eurozone will find it more than difficult to get back on track if Europe’s locomotive is not steaming in the right direction. So traders should keep a close eye on Germany, the Eurozone’s largest economy.

- US releases on a roll: The markets are used to ups and downs in US numbers, and we continue to see alternating weeks in economic data. This past week was mostly positive, with better than expected new home sales, a record low in continuing claims and a nice rise in durable goods orders on Friday. There was more good news on Tuesday, as CB Consumer Confidence shot up to its highest level since June 2009. As well, the S&P/CS Composite-20 HPI posted a sharp gain, indicating more activity in the US housing market. Will the upward trend continue? We’ll get a better idea of the extent of the US recovery, with three key releases later on Thursday.

- Taper speculation boosts US dollar: Although the Fed hasn’t made any changes to the current round of QE, Fed policymakers, including Fed Chair Bernanke, continue to hint that QE could be scaled back in the next few months. The currency markets have reacted sharply to talk about terminating QE, and much of the volatility we are seeing from EUR/USD can be attributed to market uncertainty about what action the Fed will take. Talk of an end to QE has helped the dollar, and we can expect the currency markets to continue to be very sensitive to further talk of tapering QE.

- Negative Interest Rates for ECB? Recent comments from the ECB about negative interest rates have affected the euro, and ECB Mario Draghi and other policymakers have expressed openness to the idea. Earlier in the week, ECB Executive Board member Joerg Asmussen said that the ECB will continue its expansive monetary policy in order to boost the Eurozone economy, but urged caution on the question of whether to continue reducing rates. Asmussen said that the ECB can’t simply fix uncompetitive economies with monetary policy, such as the adopting negative interest rates. The ECB’s deposit rate currently stands at zero, and if the ECB decides to go lower, it would be the first central bank to introduce negative interest rates.