EUR/USD remains under pressure as we begin the new trading week. The euro lost over a cent following the surprise ECB rate cut on Thursday, and the pair is trading below the 1.34 line. On Friday, US Non-Farm Payrolls surged, further helping the dollar. However, Preliminary UoM Consumer Sentiment was a disappointment, slipping to an eight-month low. There are only two Eurozone events on Monday and US markets are closed for a holiday.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

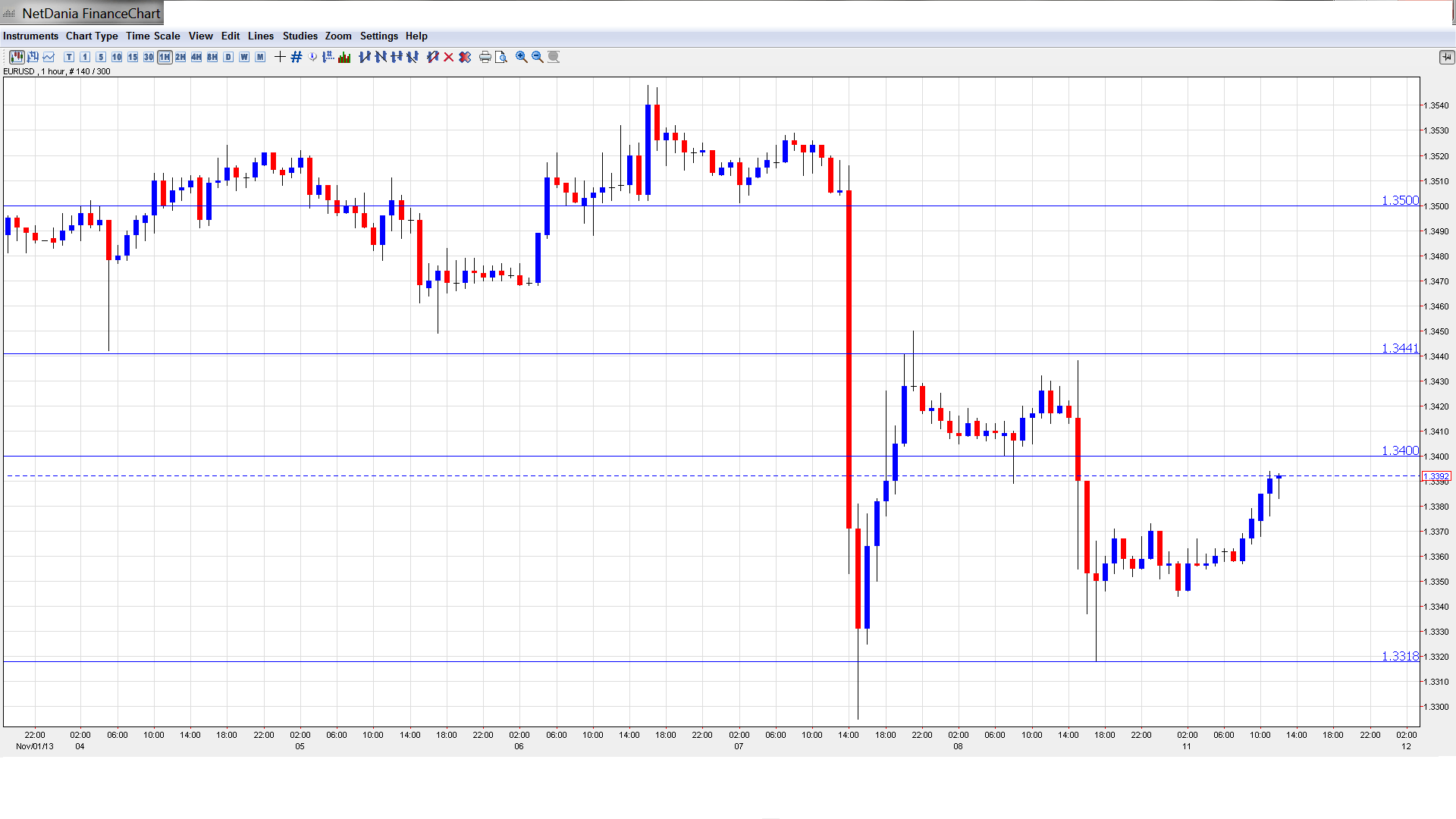

EUR/USD Technical

- In the Asian session, EUR/USD was steady, trading close to the 1.3360 line. The pair has moved higher in the European session.

- Current range: 1.3320 to 1.3400.

Further levels in both directions:

- Below: 1.3320, 1.3240, 1.3175, 1.31, 1.3050 and 1.3000, 1.2940, 1.2890 and 1.2840.

- Above: 1.3400, 1.3440, 1.3500, 1.3570, 1.3650, 1.3710, 1.3800 and 1.3870

- 1.3320 is the next support level. 1.3240 is stronger.

- On the upside, 1.3400 is under strong pressure. 1.3440 is next.

EUR/USD Fundamentals

- 9:00 Italian Industrial Production. Exp. 0.2%, Actual 0.2%.

- 17:00 German Buba President Jens Weidmann Speaks.

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Non-Farm Payrolls Soars: The markets had very low expectations from the October NFP, with an estimate of just 121 thousand. However, the indicator jumped to 204 thousand, its highest level in eight months. The sparkling NFP figure gave a boost to the US dollar, and has increased speculation that the Fed might press the tapering trigger in December. Such talk could bolster the US currency, as a reduction in QE is bullish for the dollar.

- ECB surprises with rate cut: The ECB surprised the markets on Thursday when it reduced its benchmark interest rates by 0.25%, to a record low rate of 0.25%. The marginal rate was cut to 0.75% from 1.0%, while the deposit rate was left at unchanged at 0.0%. ECB head Mario Draghi noted that inflation in the Eurozone remains very low and said that this would likely continue in the coming months. He added that further monetary easing was an option until conditions improved. The markets had expected the benchmark rate to remain at 0.50%, but the combination of weak growth and very low inflation led to the ECB making the surprise move.

- Euro takes a dive: The surprise ECB rate cut and superb Non-Farm Payrolls are the latest setbacks for the struggling euro. The currency looked sharp just a couple of weeks ago, when it was trading above the 1.38 line. Since then, the euro has taken a sharp turn downwards, shedding over four cents against the US dollar. With increasing talk of a Dectaper from the Federal Reserve, there is more room for the euro to fall.

- French data disappoints: The French economy continues to disappoint, as Industrial Production declined 0.5%, well off the estimate of a 0.4% gain. This marked the fourth decline for the manufacturing indicator in five releases. The trade surplus widened to -5.8 billion euros in October, a four-month high. This was well off the forecast of -4.7 billion. To add to the bad news, the Standard and Poor’s credit rating agency downgraded France’s sovereign rating from AA+ to AA. However, the outlook has improved from negative to stable, meaning we’re unlikely to see another downgrade to France’s rating for quite some time.

- Mixed data out of Germany: Germany is the Eurozone’s largest economy, so German data has a strong impact on the Eurozone as well as the euro. Last week’s data was a mixed bag, making it difficult to predict in which direction the German economy is headed. Factory Orders jumped 3.3% in October, bouncing back from a decline of 0.3% in September. This was well above the estimate of 0.6%. However, Industrial Production failed to keep pace, posting a decline of 0.9%, compared to a strong 1.4% the month before. The estimate stood at 0.2%. The week ended on a bright note, as the trade surplus jumped from 15.6 billion euros to 18.8 billion, its highest level since December 2007. This easily beat the estimate of 17.2 billion.