EUR/USD has edged lower in Thursday trading, as the pair trades in the mid-1.34 range. It’s been a very quiet week until now, but the markets will have plenty of data to sift through on Thursday. Eurozone GDP disappointed, posting a weak gain of just 0.1% in October. Over in the US, there are two key releases – Trade Balance and Unemployment Claims. As well, incoming Federal Reserve Chair Janet Yellen will testify before the Senate Banking Committee.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

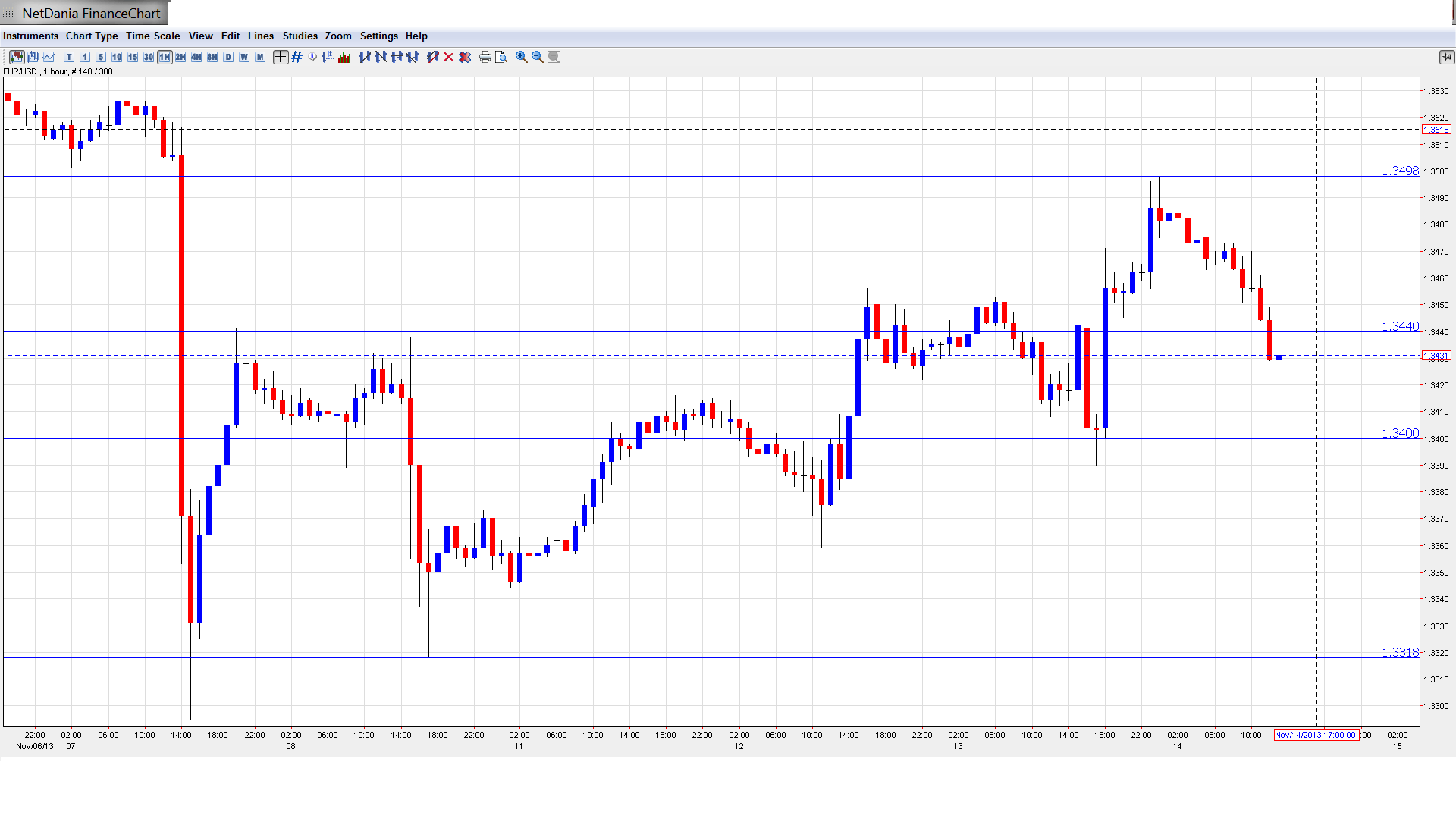

EUR/USD Technical

- In the Asian session, EUR/USD lost ground. The pair touched a high of 1.3498 early in the session but then retracted, consolidating at 1.3456. The pair is steady in the European session.

- Current range: 1.3440 to 1.3500.

Further levels in both directions:

- Below: 1.3440, 1.3400, 1.3320, 1.3240, 1.3175, 1.31, 1.3050 and 1.3000, 1.2940, 1.2890 and 1.2840.

- Above: 1.3500, 1.3570, 1.3650, 1.3710, 1.3800 and 1.3870

- 1.3440 is providing the pair with weak support. 1.3400 is next.

- On the upside, 1.3500 is the next line of resistance. 1.3570 follows.

EUR/USD Fundamentals

- 00:00 Federal Chairman Bernard Bernanke Speaks.

- 6:30 French Preliminary GDP. Exp. 0.1%, Actual -0.1%.

- 7:00 German Preliminary GDP. Exp. 0.3%, Actual 0.3%.

- 7:45 French Preliminary Non-Farm Payrolls. Exp. -0.1%, Actual -0.1%.

- 7:45 French CPI. Exp. 0.0%, Actual -0.1%.

- 9:00 ECB Monthly Bulletin.

- 9:00 Italian Preliminary GDP. Exp. -0.2%, Actual -0.1%.

- 10:00 Eurozone Flash GDP. Exp. 0.2%. Actual 0.1%.

- All Day – Eurogroup Meetings.

- 13:30 US Trade Balance. Exp. -38.7B.

- 13:30 US Unemployment Claims. Exp. 331K.

- 13:30 US Preliminary Non-Farm Productivity. Exp. 1.3%.

- 13:30 US Preliminary Unit Labor Costs. Exp. 1.1%.

- 15:00 Federal Reserve Chairperson-Designate Janet Yellen Testifies. Yellen will testify before the Senate Banking Committee.

- 15:30 US Natural Gas Storage. Exp. 21B.

- 16:00 US Crude Oil Inventories. Exp. 0.7M.

- 18:01 US 30-year Bond Auction.

*All times are GMT

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Eurozone GDP releases disappoints: Eurozone GDP releases point to continuing weak growth in the region. Eurozone Flash GDP gained just 0.1%, shy of the estimate of 0.2%. French and Italian Preliminary GDP both declined by 0.1%, missing their estimates. German Preliminary GDP matched the forecast of 0.3%, but this figure was sharply lower than the September reading, which posted a gain of 0.7%. The ECB lowered interest rates last week in an attempt to improve economic growth, and we’ll have to wait and see if next month’s GDP numbers respond positively to the rate cut.

- Eurozone manufacturing data disappoints: Weak economic growth in the Eurozone was one of the factors that precipitated the ECB’s rate cut last week. The manufacturing sector is one sore spot in the economy, as underscored by a weak Eurozone Industrial Production release on Wednesday. The important indicator declined 0.5%, short of the estimate of -0.2%. It was the second decline in the past three readings. Earlier this week, Italian Industrial Production posted a weak gain of 0.2%, matching the estimate. If Eurozone releases continue to point to sluggish growth, we can expect the euro to remain under strong pressure from the US dollar.

- Greece and troika spar over Greek budget: Greece has imposed sharp austerity measures to get its fiscal house in order, but stumbling blocks remain on the bumpy road to economic recovery. The troika has promised Greece another installment of aid worth 1 billion euros, but wants to see the country plug a 2 billion euro hole in its 2014 budget. The Greek government has rejected tax hikes or cuts in wages or pensions, which will make it difficult to eliminate this deficit. The troika has already provided Greece with some 240 billion euros in aid since 2010 and is insisting that the government stay within its 2014 budget, and has threatened to suspend the next installment until Athens takes further steps to keep costs under control. The tug-of-war between the sides will likely continue for some time.

- Yellen to testify at Senate hearing: Incoming Federal Reserve head Janet Yellen will testify before the powerful Senate Banking Committee on Thursday. The hearing could be a rough one for Yellen, as Republicans are expected to grill her on the Fed’s QE program, which they oppose. Yellen is considered dovish in her monetary outlook and supported Bernard Bernanke in implementing QE, which currently stands at $85 billlion each month. On Wednesday, Yellen said that the economy is not performing up to its potential and unemployment remains too high.

- Euro remains under pressure: Weak growth in the Eurozone and the surprise ECB rate cut last week have hurt the euro, and the superb Non-Farm Payrolls has given the dollar a big boost. The euro looked sharp just a couple of weeks ago, when it was trading above the 1.38 line. Since then, the euro has taken a sharp turn downwards, shedding about four cents against the US dollar. With increasing talk of a Dectaper from the Federal Reserve, which would be bullish for the dollar, we could see the struggling euro continue to point downwards.