EUR/USD is trading quietly on Friday, as the pair trades in the high-1.34 range in European trading. Thursday was a busy day for US releases, highlighted by a strong Unemployment Claims release. On the downside, PPI posted another decline and the Philly Fed Manufacturing Index looked awful. Taking a look at Friday’s events, German Ifo Business Climate, a market-mover, will be released later on Friday. ECB head Mario Draghi will speak at a banking conference in Frankfurt. In the US, there’s a pause in the action after two busy days. Today’s highlight is JOLTS Job Openings.

EUR/USD is trading quietly on Friday, as the pair trades in the high-1.34 range in European trading. Thursday was a busy day for US releases, highlighted by a strong Unemployment Claims release. On the downside, PPI posted another decline and the Philly Fed Manufacturing Index looked awful. Taking a look at Friday’s events, German Ifo Business Climate, a market-mover, will be released later on Friday. ECB head Mario Draghi will speak at a banking conference in Frankfurt. In the US, there’s a pause in the action after two busy days. Today’s highlight is JOLTS Job Openings.

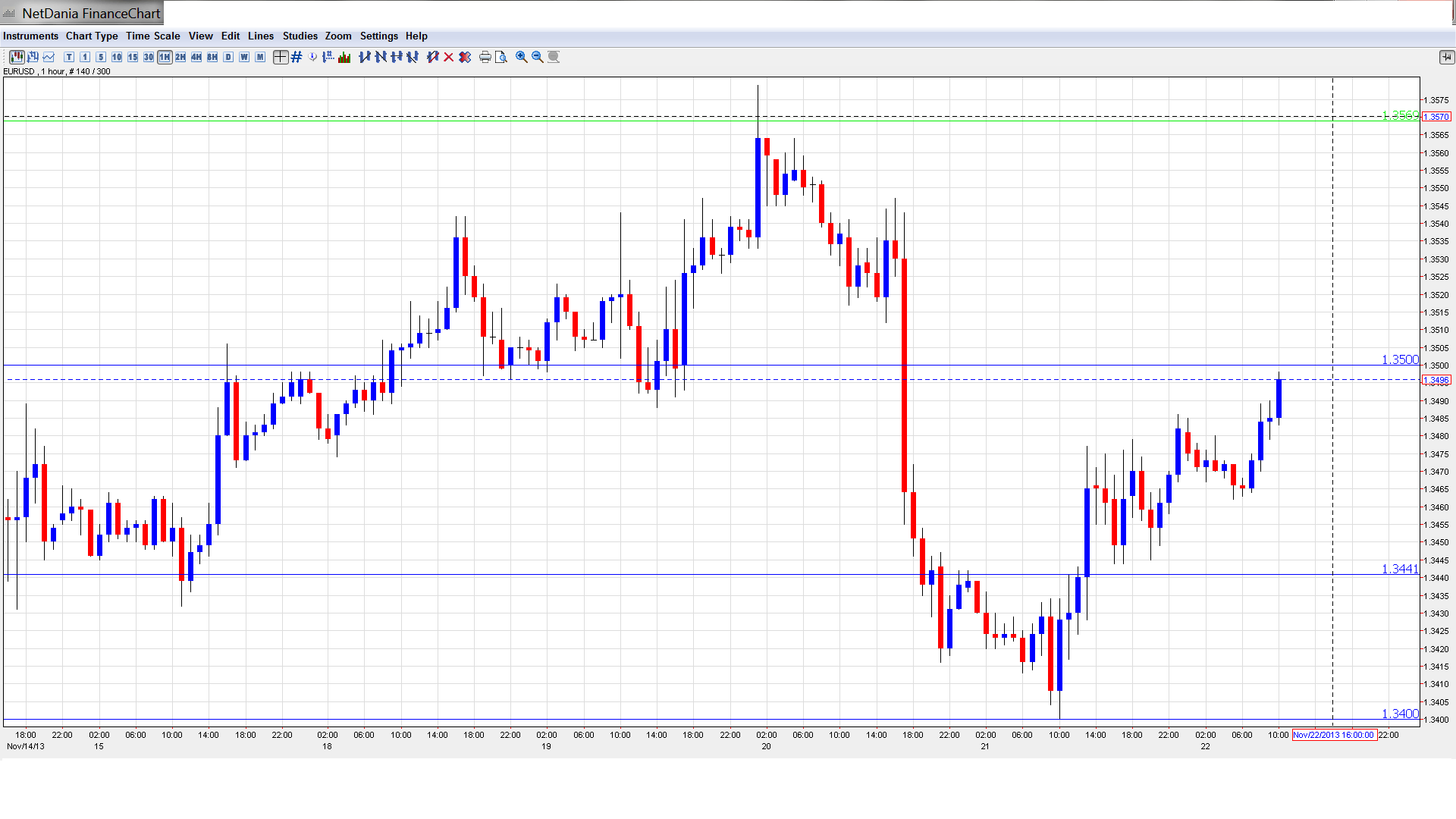

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

EUR/USD Technical

- In the Asian session, EUR/USD moved higher late in the session, touching a high of 1.3490 and consolidating at 1.3485. There is no changed in the European session.

- Current range: 1.3440 to 1.3500.

Further levels in both directions:

- Below: 1.3440, 1.34, 1.3320, 1.3240, 1.3175, 1.31, 1.3050, 1.3000, 1.2940, 1.2890 and 1.2840.

- Above: 1.35, 1.3570, 1.3650, 1.3710, 1.3800 and 1.3870.

- 1.3440 is providing weak support. 1.3400 follows.

- 1.3500 is the next line of resistance. This is followed by 1.3570.

EUR/USD Fundamentals

- 7:00 German Final GDP. Exp. 0.3%. Actual 0.3%.

- 9:00 German Ifo Business Climate. Exp. 107.9 points.

- 9:00 Italian Retail Sales. Exp. 0.4%.

- 9:30 ECB President Mario Draghi Speaks.

- All Day – Eurogroup Meetings.

- 13:40 US FOMC Member Esther George Speaks.

- 14:00 Belgian NBB Business Climate. Exp. -6.9 points.

- 15:00 US JOLTS Job Openings. Exp. 3.89M.

- 17:15 US FOMC Member Daniel Tarullo Speaks.

*All times are GMT

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Unemployment claims drop: There was good news on the employment front, as Unemployment Claims dropped to 323 thousand, a seven-week low. This was well below the estimate of 333 thousand. The strong figure will likely increase speculation about when the Fed will step in and taper QE, although such a dramatic move is not considered likely before early 2014. The markets will be keeping a close eye on JOLTS Job Openings, which will be released later on Friday.

- US inflation remains weak: Low inflation indicators have been a major concern in Japan and the Eurozone, and this problem is affecting the US economy as well. The Producer Price Index continues to sputter, posting a decline of 0.2%. This was the index’s second straight decline. Earlier this week, Core CPI showed a paltry gain of 0.1%, and CPI dipped to -0.1%. These weak numbers point to slow economic activity and weak economic growth in the US.

- Dollar jumps after Fed minutes: The Federal Reserve released the minutes of its most recent policy meeting on Wednesday. Policymakers said the current QE level of $85 billion monthly purchases of bonds could taper “in coming months” if the economy continued to improve. The dollar was up sharply after the minutes were released. Earlier in the week, Fed chair Bernard Bernanke said that the employment market improvement was “meaningful” and that interest rates would likely remain low even after QE ends.

- European PMIs provide mixed results: European Manufacturing and Services PMIs pointed to a mixed picture in the Eurozone. In France, both PMIs came in below 50, pointing to contraction. Eurozone Manufacturing PMI was within expectations, while Services PMI stayed above 50 but fell short of the estimate. The news was better out of Germany, as both PMIs beat the estimates and remained comfortably above the 50-point level. The euro will have trouble holding its own against the US dollar if the region doesn’t produce stronger numbers.

- Negative rates for ECB?: With inflation remaining very weak despite recent rate cuts, the ECB is considering cutting the deposit rate, which currently stands at 0.0%. However, a move into negative territory would represent unchartered territory and could have negative consequences for the economy. So if the ECB does go ahead and reduce to deposit rate, we could see a “mini cut” of less than 0.25%. The OECD is also expressing concern about the dangers of deflation in the Eurozone and is urging the ECB to consider implementing quantitative easing. QE, a non-conventional monetary policy tool, is an important component in the monetary policy of central banks such as the Federal Reserve and the Bank of England.