EUR/USD dropped sharply on Thursday, as the ECB unexpectedly cut rates by 0.25% at its policy meeting. The euro dropped over a cent, closing just above the 1.34 line. The pair has steadied in Friday trading. In economic news, the news was not good out of France, as Industrial Production declined and the trade deficit widened. However, Germany’s trade surplus surged to its highest levels in almost six years. Over in the US, the highlight of the day is Non-Farm Payrolls, with the markets braced for a weak reading. Other key events include the Unemployment Rate and Preliminary UoM Consumer Sentiment. The week wraps up with Federal Reserve head Bernard Bernanke addressing an IMF event in Washington.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

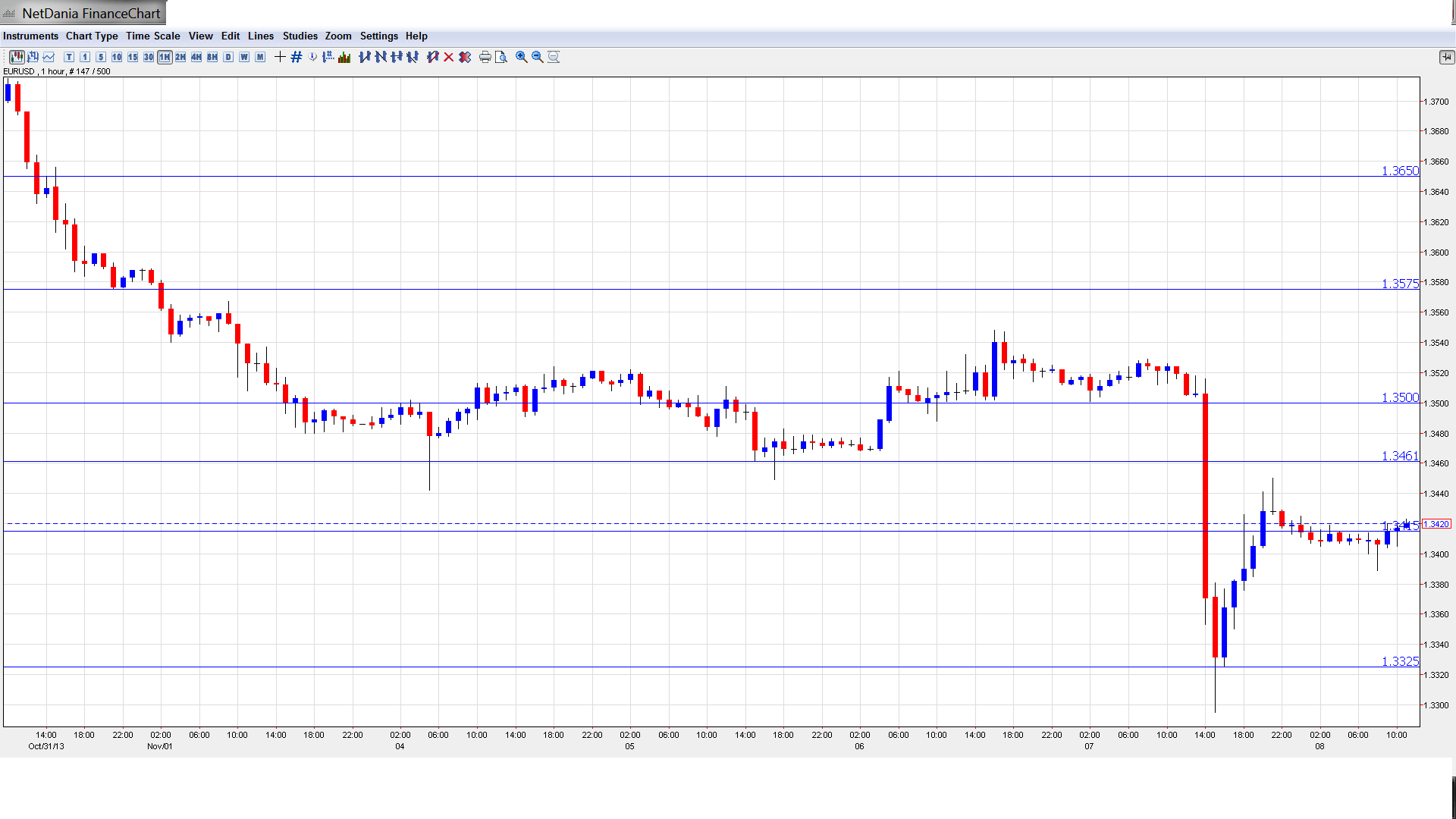

EUR/USD Technical

- In the Asian session, EUR/USD was steady. The pair dipped to a low of 1.3389 before crossing back above 1.34 and consolidated at 1.3416. EUR/USD is steady in the European session.

- Current range: 1.3325 to 1.3415.

Further levels in both directions:

- Below: 1.3325 and 1.3240, 1.3175, 1.31, 1.3050 and 1.3000.

- Above: 1.3415, 1.3460, 1.3500, 1.3570, 1.3650, 1.3710, 1.3800, 1.3870 and 1.3940.

- 1.3325 is providing strong support.

- On the upside, 1.3415 is under strong pressure. It is followed by 1.3460.

EUR/USD Fundamentals

- 7:00 German Trade Balance. Exp. 17.2 B, Actual 18.8B.

- 7:45 French Industrial Production. Exp. 0.4%., Actual -0.5%.

- 7:45 French Government Budget Balance. Actual -80.8B.

- 7:45 French Trade Balance. Exp. -4.7B, Actual -5.8B.

- 13:30 US Non-Farm Employment Change. Exp. 121K.

- 13:30 US Unemployment Rate. Exp. 7.3%.

- 13:30 US Average Hourly Earnings. Exp. 0.2%.

- 13:30 US Personal Spending. Exp. 0.3%.

- 13:30 US Core PCE Price Index. Exp. 0.1%.

- 13:30 US Personal Income. Exp. 0.3%.

- 14:55 US Preliminary UoM Consumer Sentiment. Exp. 74.6 points.

- 14:55 US Preliminary UoM Inflation Expectations.

- 18:10 President Barak Obama Speaks.

- 20:30 Fed Chairman Bernard Bernanke Speaks. Bernanke will address an IMF conference in Washington.

* All times are GMT.

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- ECB reduces rates to record low: The ECB surprised the markets on Thursday when it reduced its benchmark interest rates by 0.25%, to a record low rate of 0.25%. The marginal rate was cut to 0.75% from 1.0%, while the deposit rate was left at unchanged at 0.0%. ECB head Mario Draghi noted that inflation in the Eurozone remains very low and said that this would likely continue in the coming months. He added that further monetary easing was an option until conditions improved. The markets had expected the benchmark rate to remain at 0.50%, but the combination of weak growth and inflation way below the ECB’s target of 2% led to the ECB making the surprise move.

- French data disappoints: The French economy continues to disappoint, as Industrial Production declined 0.5%, well off the estimate of a 0.4% gain. This marked the fourth decline for the manufacturing indicator in five releases. The trade surplus widened to -5.8 billion euros in October, a four-month high. This was well off the forecast of -4.7 billion. To add to the bad news, the Standard and Poor’s credit rating agency downgraded France’s sovereign rating from AA+ to AA. However, the outlook has improved from negative to stable.

- Mixed data out of Germany: Germany is the Eurozone’s largest economy, so German data has a strong impact on the Eurozone as well as the euro. This week’s data has been a mixed bag, making it difficult to predict in which direction the German economy is headed. Factory Orders jumped 3.3% in October, bouncing back from a decline of 0.3% in September. This was well above the estimate of 0.6%. However, Industrial Production failed to keep pace, posting a decline of 0.9%, compared to a strong 1.4% the month before. The estimate stood at 0.2%. The week ended on a bright note, as the trade surplus jumped from 15.6 billion euros to 18.8 billion, its highest level since December 2007. This easily beat the estimate of 17.2 billion.

- All eyes on Non-Farm Payrolls: US employment numbers will be the focus on Friday. Non-Farm Payrolls, a critical event which could move EUR/USD, is expected to fall to 121 thousand in October. However, it should be noted that the government shutdown in October resulted in some workers being removed from payrolls, which would explain the low October forecast. On Thursday, Unemployment Claims looked solid, coming in at 336 thousand, matching the forecast. An unexpectedly strong NFP release would likely fuel speculation of a possible QE tapering in December.