The euro continues to post gains against the US dollar in Friday trading. EUR/USD jumped about 160 points on Thursday, and is trading close to the 1.37 line in Friday’s European session. These are the highest levels we have seen since February. Congress has agreed to fund the government and raise the debt limit, but only for a few months, so the dollar’s struggles continue. In economic news, US Unemployment Claims fell from the previous week, while the Philly Fed Manufacturing Index easily beat the estimate. The week is ending on a very quiet note, as there are no economic releases out of Europe or the US. The only events on today’s schedule are speeches from four FOMC members.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

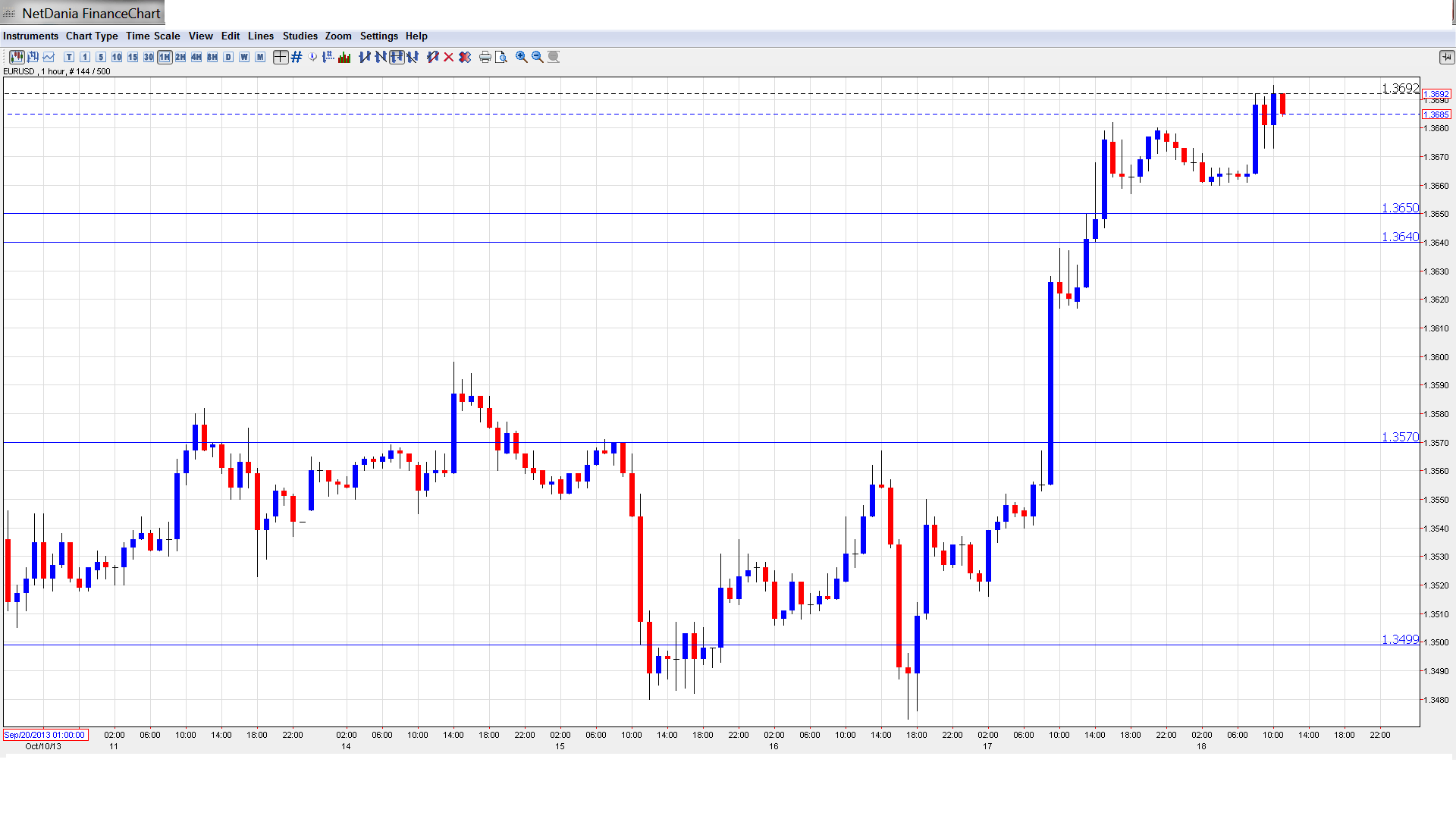

EUR/USD Technical

- In the Asian session, EUR/USD was quiet, touching a low of 1.3660. The pair has edged higher in the European session.

- Current range: 1.3650 to 1.3710.

Further levels in both directions:

- Below: 1.3650, 1.3570, 1.3500, 1.3460, 1.3415, 1.3325, 1.3240, 1.3175, 1.31, 1.3050 and 1.3000.

- Above: 1.3710, 1.3800, 1.3870, 1.3940 and 1.40.

- 1.3650 is providing weak support. 1.3570 follows.

- On the upside, 1.3710 is facing strong pressure. 1.3800 is next.

EUR/USD Fundamentals

- 16:30 US FOMC Member Daniel Tarullo Speaks.

- 18:00 US FOMC Member Charles Evans Speaks.

- 19:40 US FOMC Member William Dudley Speaks.

- 20:30 US FOMC Member Jeremy Stein Speaks.

* All times are GMT.

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Debt ceiling averted: With the US staring at a sovereign default for the first time in its history, the Republicans and Democrats finally reached an agreement on Wednesday to reopen the government and raise the debt ceiling. The agreement passed by wide margins in both the Senate and House. However, the deal provides short-term relief only – the government will be funded until January 15, while the debt limit will be raised until February 7. Both sides agreed to discuss budget issues and try to reach a long-term agreement before December 13. So we could be right back where we started in just a few months. The Republicans appear to be the big losers in this saga, as they failed to obtain any concessions regarding the Obama Health Care Act and are blamed by most of the public for precipitating an unnecessary political and fiscal crisis.

- Crisis over, but US economy, credibility takes hit: After weeks of finger pointing and political brinkmanship, Congress finally got its act together and voted to fund the government and raise the debt ceiling. The shutdown, which lasted for over two weeks and temporarily threw hundreds of thousand of federal employees out of work, is estimated to have cost the economy $24 billion. The cost of the debt crisis is harder to quantify, but has certainly eroded faith in the US economy. This was underscored by a warning from Fitch Ratings on Tuesday, when the agency put US debt on a negative watch. Fitch stated that the crisis had cast doubt over the credit of the United States and had undermined confidence “in the role of the US dollar as the pre-eminent global reserve currency”.

- US Unemployment Claims Fall: With the crisis in Washington finally over, the markets can shift their attention to US economic data. Unemployment Claims came in at 357 thousand, very close to the estimate of 358 thousand. This figure was an improvement from last week, but still well above previous releases. The shutdown inflated the release, as hundreds of thousands of Federal employees were laid off. The markets will be eagerly waiting for other employment data, such as Non-Farm Payrolls, which was not published during the shutdown and is scheduled to be released on Tuesday.

- Fed unlikely to taper QE: The crisis mood in Washington has cleared for now, but the agreement hammered out in Congress the day before a possible default is only temporary – it raises the debt ceiling until early February and funds the government until mid-January. The underlying budgetary issues remain unresolved, and in this tense situation, the Fed is unlikely to push the taper trigger until some time in 2014. Ongoing QE is the main factor weighing on the dollar and we can expect this situation to continue for a while yet.

- Eurozone inflation remains low: This week’s inflation indicators continue to point to weak inflation in the Eurozone. Eurozone CPI dropped from 1.3% to 1.1% in September, while Eurozone Core CPI edged lower, from 1.1% to 1.0%. Both indexes matched expectations. The inflation numbers point to sluggish economic activity and continue to be a source of concern for Eurozone policymakers.