After climbing to eight-month highs last week, EUR/USD is showing very little movement as we start the new trading week. The pair is trading in the mid-1.36 range in Monday’s European session. With the crisis in Washington over, the markets can focus on economic releases. On Monday, German PPI posted a gain of 0.3%, beating the estimate. Today’s highlight is US Existing Home Sales. The markets will also be keeping a close eye on Non-Farm Payrolls, which will be released on Tuesday.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

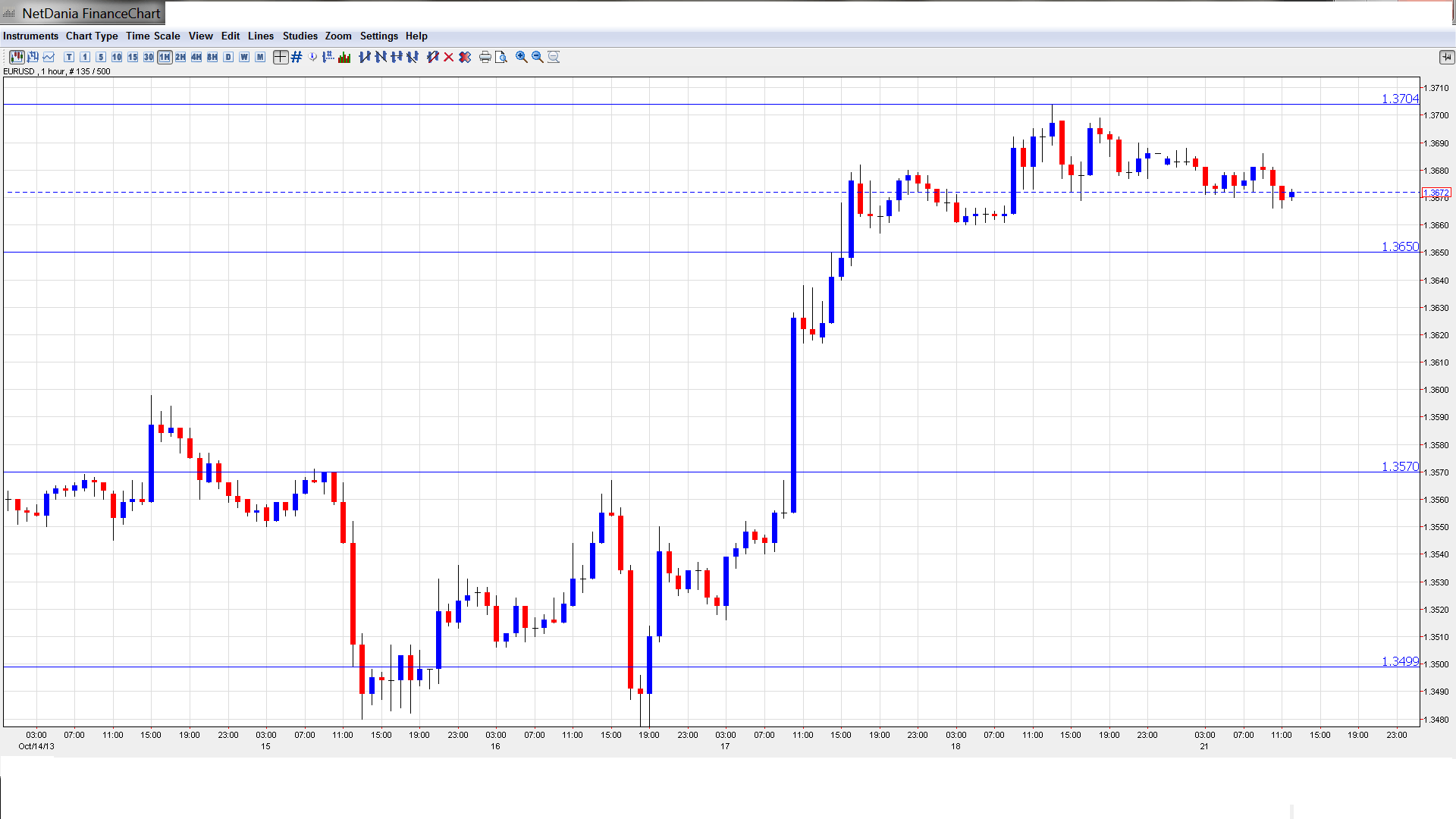

EUR/USD Technical

- In the Asian session, EUR/USD was uneventful, touching a high of 1.3685 and consolidating at 1.3682. The pair has edged lower in the European session.

- Current range: 1.3650 to 1.3710.

Further levels in both directions:

- Below: 1.3650, 1.3570, 1.3500, 1.3460, 1.3415, 1.3325, 1.3240, 1.3175 and 1.3100.

- Above: 1.3710, 1.3800, 1.3870, 1.3940 and 1.4036.

- 1.3650 is providing weak support. 1.3570 follows.

- On the upside, 1.3710 continues to face pressure. The round number of 1.3800 is next.

EUR/USD Fundamentals

- 6:00 German PPI. Exp. 0.1%, Actual 0.3%.

- Tentative – German Buba Monthly Report.

- 12:00 FOMC Member Charles Evans Speaks.

- 14:00 US Existing Home Sales. Exp. 5.31M.

- 14:30 US Crude Oil Inventories. Exp. 3.4M.

* All times are GMT.

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Eurozone inflation remains low: Inflation in the Eurozone continues to be subdued, as underscored by German PPI which posted a modest gain of 0.3%. This was the indicator’s first gain since January. Other inflation indicators have been weak, pointing to sluggish economic activity. ECB President Mario Draghi has voiced his concern about weak inflation, but there seems little that the ECB can do to tackle the problem.

- Debt ceiling averted, but dollar loses ground: With the US staring at a sovereign default for the first time in its history, the Republicans and Democrats finally reached an agreement last week to reopen the government and raise the debt ceiling. However, the deal provides short-term relief only – the government will be funded until January 15, while the debt limit will be raised until February 7. Both sides agreed to discuss budget issues and try to reach a long-term agreement before December 13. So we could be right back where we started in just a few months. The Republicans appear to be the big losers in this saga, as they failed to obtain any concessions regarding the Obama Health Care Act and are blamed by most of the public for precipitating an unnecessary political and fiscal crisis. The dollar initially gained ground after the agreement was announced, but was broadly lower as optimism faded. On Friday, EUR/USD touched above the 1.37 line, an eight-month high.

- Markets Eye Non-Farm Payrolls: The recent government shutdown cancelled some US economic releases, notably Non-Farm Payrolls, one of the most important employment releases. The September report was supposed to be released in early October, but has been rescheduled for release on Tuesday. The NFP release could have a major impact on EUR/USD. Meanwhile, last week’s Unemployment Claims came in at 357 thousand, very close to the estimate of 358 thousand. This figure was an improvement from last week, but still well above previous releases. The shutdown inflated the release, as hundreds of thousands of Federal employees were laid off. This week’s claim is lower, with an estimate of 341 thousand.

- Fed unlikely to taper QE: The crisis mood in Washington has cleared for now, but the agreement hammered out in Congress provides short-term relief only, as it raises the debt ceiling until early February and funds the government until mid-January. The underlying budgetary issues remain unresolved, and in this tense situation, the Fed is unlikely to push the taper trigger until some time in 2014. Ongoing QE is the main factor weighing on the dollar and we can expect this situation to continue for a while yet.