Mario Draghi and his colleagues meet in less than 24 hours in the first decision since announcing the big stimulus package. Will they try to talk down the euro? Or perhaps re-open the door to more cuts? And what’s next for the euro?

Here is their view, courtesy of eFXnews:

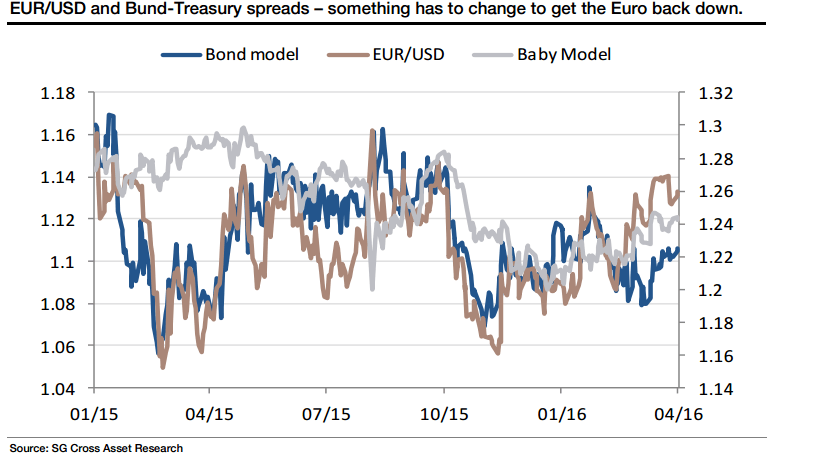

As EUR/USD skips towards 1.14, the fact that it’s doing so despite huge outflows of long-term capital and wholesale abandon of European bonds by foreigners, doesn’t really help. The Euro is going up despite the ECB.

The yield-spread-based model of EUR/USD I’ve been using for just over a year now suggests that EUR/USD a ‘a bit’ high, but it also suggests it’s going in the right direction. My old ‘baby model’ based on vol, peripheral European spreads and 2-year rate differentials, is so out of touch it gets its own axis, but even so, it too points upwards. Relative rate and yield trends are trumping the balance of payments and the effects of QE/ECB.

Back in December, when EUR/USD trade below 1.06 ahead of fed tightening, 10yearn Treasury yields were at 2.15% and the EU/US spread at 177bp. Today, those numbers are 1.78% and 160bp. A weaker Euro needs something in this mix to change.

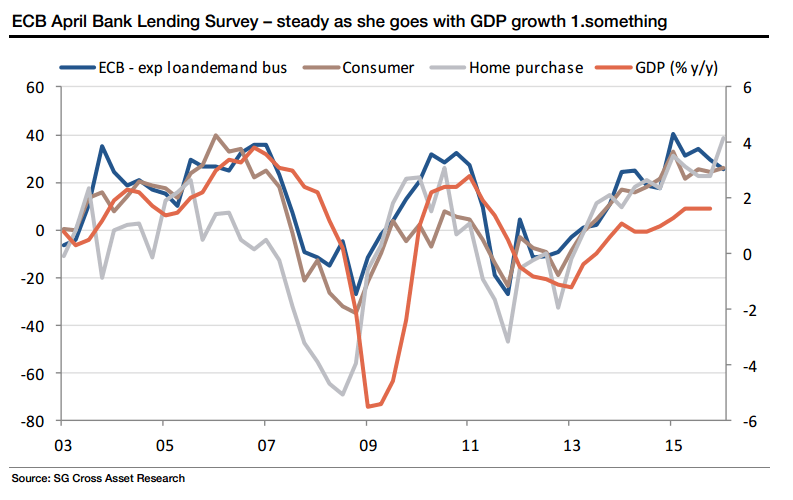

Finally, a bonus chart because the ECB also released the April Bank Lending Survey. This showed an that demand for home loans is expected to pick up, while demand for consumer loans remains steady and demand for loans to business is expected grow, but more slowly in the months ahead. The chart plots all that against the year-over-year GDP growth rate, and ‘steady as she goes’ seems to sum it up.

The ECB isn’t about to change policy any time soon. This really won’t be the driver of Bund yields, anchored by the ECB, peripheral spreads (anchored by the ECB), or the Euro (supported by the Fed).

For lots more FX trades from major banks, sign up to eFXplus

By signing up to eFXplus via the link above, you are directly supporting Forex Crunch.