EUR/USD has edged lower in Wednesday trading, after the pair pushed above the 1.39 a day earlier. In the European session, the pair is trading slightly above the 1.39 line. Taking a look at Wednesday’s releases, French and German indicators both posted declines and missed expectations. In the US, the Federal Reserve will be in the spotlight as Janet Yellen testifies before Congress on Wednesday and Thursday.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

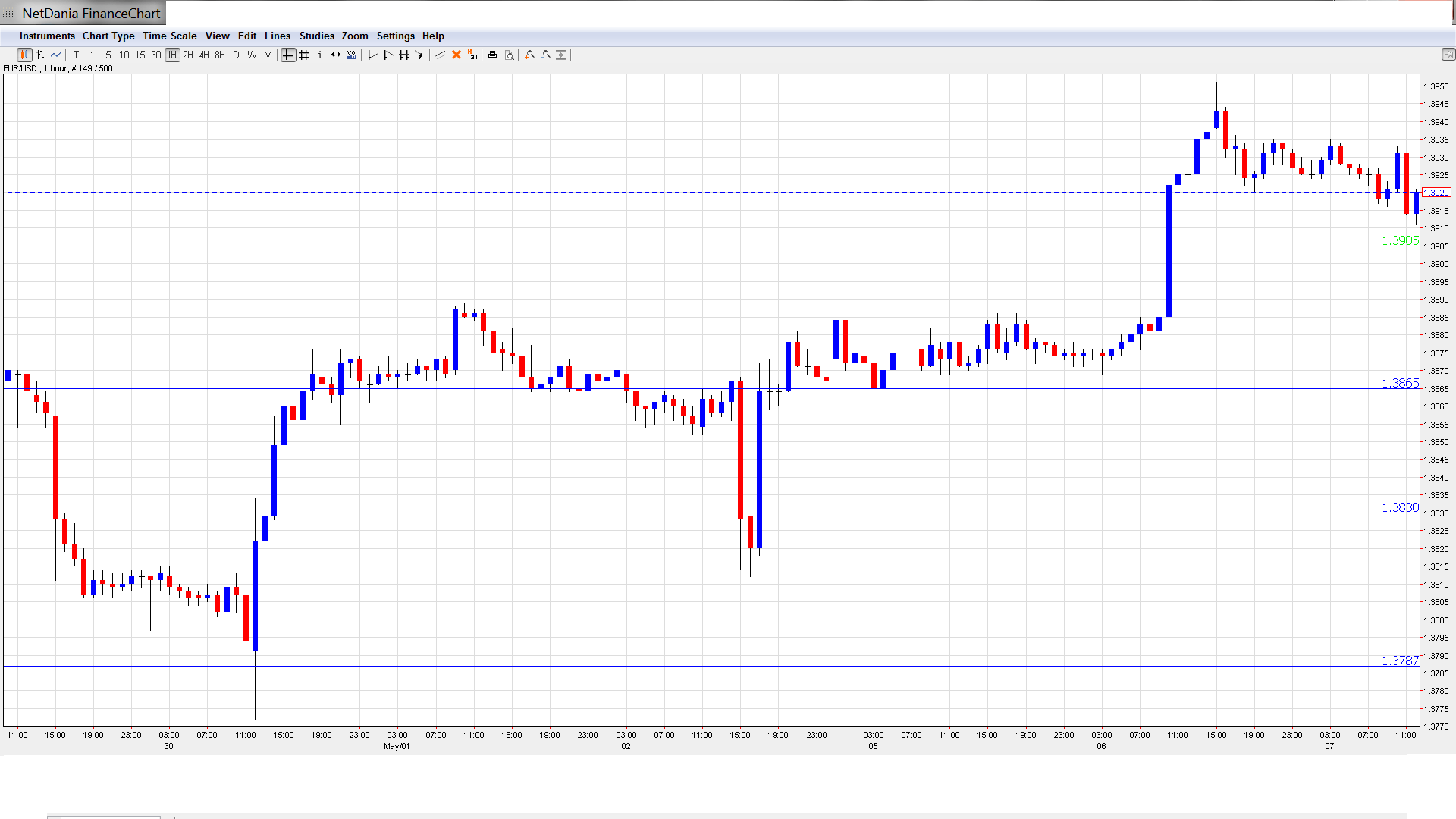

EUR/USD Technical

- EUR/USD was flat in the Asian session, trading around 1.3930. The pair has edged lower in the European session.

Current range: 1.3905 to 1.3964.

Further levels in both directions:

- Below: 1.3905, 1.3865, 1.3830, 1.3785, 1.3740, 1.37, 1.3650 and 1.3560, 1.3515 and 1.3450

- Above: 1.3964, 1.40, 1.4055 and 1.4105

- 1.3964 is the next line of resistance. The key level of 1.40 is next.

- 1.3905 is providing weak support. 1.3865 is stronger.

EUR/USD Fundamentals

- 6:00 German Factory Orders. Exp. +0.3%. Actual -2.8%.

- 6:45 French Industrial Production. Exp. +0.3%. Actual -0.7%.

- 6:45 French Trade Balance. Exp. -4.0B. Actual -4.9B.

- 8:10 Eurozone Retail PMI. Actual 51.2 points.

- 12:30 US Preliminary Nonfarm Productivity. Exp. -0.9%.

- 12:30 US Preliminary Unit Labor Costs. Exp. 2.3%.

- 14:00 US Federal Reserve Chair Janet Yellen Testifies Before Joint Economic Committee of Congress.

- 14:30 US Crude Oil Inventories. Exp. 0.9M.

- 17:01 US 10-year Bond Auction.

- 19:00 US Consumer Credit. Exp. 15.4B.

*All times are GMT

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Yellen visits Congress: All eyes are on Federal Reserve head Janet Yellen, who testifies before the Joint Economic Committee of Congress later on Wednesday. Although recent US employment data has been positive, Yellen continues to be guarded about the economic recovery, and if she repeats these sentiments before Congress, the dollar could be the main loser. Meanwhile, the Federal Reserve trimmed its QE program by $10 billion last week. This marks the fourth cut since December, reducing the asset purchase scheme to $45 billion/month. The tapers are no longer moving markets as they were just a few months ago. The Fed is expected to wind up QE before the end of the year, so we could see a rate hike in early 2015, depending of course, on the strength of the US economy and the job market.

- Spanish data impresses markets: Spanish data often lags well behind the Eurozone leaders, but Spanish data looked superb on Tuesday. Unemployment Change dropped by 111.6 thousand, crushing the estimate of -49.1 thousand. We tend to see sharp drops in unemployment during the busy tourist season, but the April slide was clearly much sharper than the markets had anticipated. Spanish Services PMI continues to improve, and the reading of 56.5 marked its highest level since March 2007. The estimate stood at 54.3 points. Also on Tuesday, there was positive news from Eurozone Retail Sales, the primary gauge of consumer spending. The indicator posted a gain of 0.3%, beating the estimate of -0.2%.

- Will ECB make a move?: The ECB has done its best to allay concerns about deflation, but Eurozone inflation indicators continue to point downwards. Eurozone PPI posted its third straight decline in April, coming in at -0.2%. Last week, German Preliminary CPI did no better, also declining by 0.2%. Will the ECB announce any action at Thursday’s policy meeting? ECB head Mario Draghi has stated that negative deposit rates or even QE are on the table, but the markets have heard this often before and these remarks have not had much effect, as the euro remains at high levels against the US dollar. However, with EUR/USD approaching the 1.40 line, Draghi will be under pressure to show that he is serious about tackling low inflation. Here are some scenarios as we await the ECB announcement.

- US economy: High hopes for Q2: The narrative of a weak US economy in Q1 due to the harsh winter (mentioned also by the Fed) versus a rebound in Q2 is strengthening: Q1 GDP was a shocking 0.1% and could be revised to contraction. On the other hand, Friday’s employment data bodes well for Q2, as Nonfarm Payrolls soared and the Unemployment Rate dropped significantly. As well, higher manufacturing and services PMIs and strong consumer confidence could signify improvement in Q2.

- QE taper train keeps chugging: As widely expected, the Federal Reserve trimmed its QE program by $10 billion on Wednesday. This marks the fourth cut since December, reducing the asset purchase scheme to $45 billion/month. The tapers are no longer creating headlines as they did just a few months ago, and the dollar didn’t get any lift against its major rivals. The Fed acknowledged the winter effects and left the fireworks for the June decision.