GBP/USD recorded another strong week, with gains of 2.5 percent. There are six events on the schedule, including the monthly GDP report. Here is an outlook for the highlights and an updated technical analysis for GBP/USD.

In the U.K., May PMIs remained well below the 50-level, which separates contraction from expansion. Final Manufacturing PMI came in at 40.7 in May, close to the initial read of 40.6 points. Final Services PMI pointed to a steep downturn in services, with a reading of 29.0. This was revised upwards from the initial reading of 27.8 points. Consumer confidence dipped to -36, down from -34 beforehand. This marked the lowest confidence level since January 2009.

In the U.S., ISM Manufacturing PMI improved to 43.1, up from 41.1 beforehand. The PMI has indicated contraction for three straight months, as the manufacturing sector has been hit hard by the economic crisis. The services sector also finds itself in contraction territory, as the ISM Non-Manufacturing PMI came in at 45.4 in May within expectations. Nonfarm payrolls shocked with a huge gain of 2.5 million in May, defying the estimate of -7.7 million. In April, the economy shed a staggering 20.5 million jobs. The unemployment rate fell to 13.3%, down from 14.7% beforehand. The forecast stood at 19.4 percent.

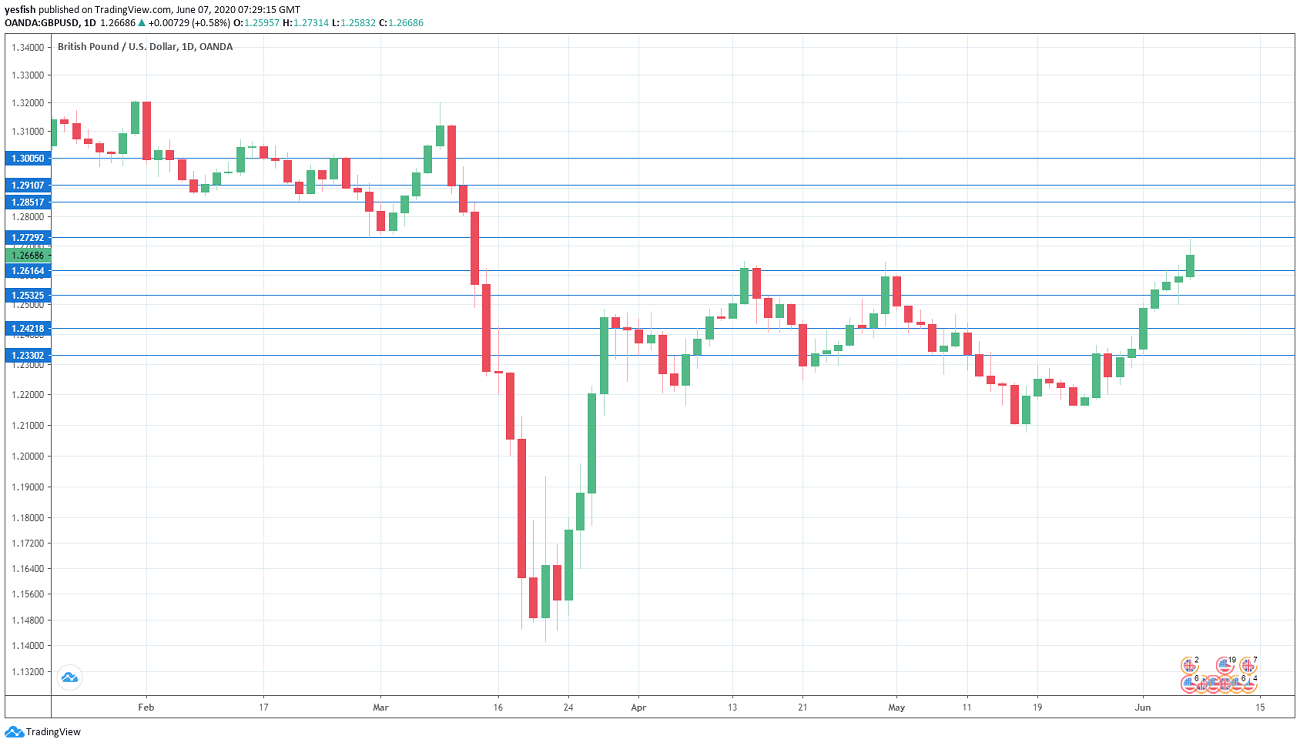

GBP/USD daily graph with resistance and support lines on it. Click to enlarge:

- BRC Retail Sales Monitor: Monday, 23:01. The British Retail Consortium gauge posted a gain of 5.7% in April, crushing the estimate of -15.0 percent. Will the upturn continue in May?

- RICS House Price Balance: Wednesday, 23:01. The Royal Institution of Chartered Surveyors survey in May showed 21% more surveyors reported a decrease in prices over those reporting an increase. Another soft read is expected, with an estimate of 24% more surveyors reporting a decrease.

- GDP: Friday, 6:00. The British economy plunged 5.8% in March, as the economy buckled under the weight of the Covid-19 pandemic. Still, this was better than the forecast of 7.9 percent. Analysts are projecting a staggering -18.0% reading in April. If the economy does hit a double-digit decline, we could see the pound react negatively.

- Manufacturing Production: Friday, 6:00. After three straight gains, the indicator sank in March, with a reading of -4.6 percent. The estimate stood at -6.0 percent. Investors are braced for a free-fall in May, with a forecast of -15.5 percent, as the manufacturing sector appears in deep trouble.

- Consumer Inflation Expectations: Friday, 8:30. The indicator is closely watched, as inflation expectations can translate into actual inflation figures. The indicator dipped to 3.0% in Q4 of 2019, its lowest level since Q2 of 2018. We now await the Q1 data.

- CB Leading Index: Friday, 13:30. The Conference Board composite index uses seven different indicators. In March, the index showed a decline of 1.3%. Another slide cannot be ruled out in April.

Technical lines from top to bottom:

With the GBP/USD posting sharp gains last week, we start at higher levels:

The round number of 1.3000 has psychological significance. This line has held since mid-May. 1.2910 is next.

1.2850 has held in support since mid-March.

1.2728 was tested at the end of the week and could see further action early this week.

1.2616 switched to a support role after sharp gains by GBP/USD last week.

1.2420 (mentioned last week) has some breathing room in support.

1.2330 is the last support level for now.

I remain neutral on GBP/USD

The pound is at 11-week highs, but this is due more to U.S. dollar weakness than strength in the British economy. With grim economic conditions in the UK, we could see a downward correction from GBP/USD in the near term.

Further reading:

- EUR/USD forecast – for everything related to the euro.

- USD/JPY forecast – projections for dollar/yen

- AUD/USD forecast – predictions for the Aussie dollar.

- USD/CAD forecast – Canadian dollar analysis

- Forex weekly forecast – Outlook for the major events of the week.

Safe trading!