The UK and the EU were close to a Brexit breakthrough, but the unsuccessful election campaign in June came to haunt Theresa May. The compromise that Ireland reached with the UK was a “regulatory alignment” between the Republic of Ireland and Northern Ireland, which is part of the UK.

Yet giving Northern Ireland a special status that put it further away from the UK was frowned upon by the DUP – a unionist party that May’s government relies upon. They upped their ante on the threats to bring down the government. An agreement was almost signed until PM Theresa May took a phone call from DUP leader Arlene Foster, and everything collapsed.

Sure, there is still time until the EU Summit of December 14-15. And sure, that deadline is not set in stone either. However, with every day that passes by, the chances of a hard Brexit rise.

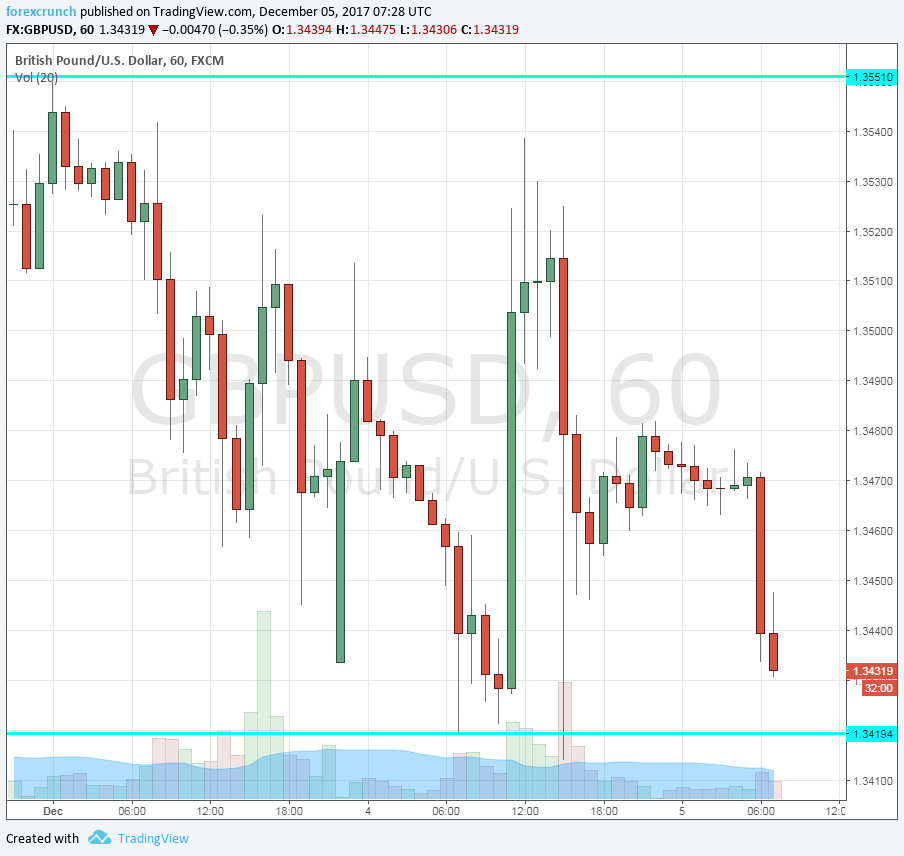

GBP/USD was challenging resistance at the highs of 1.3550 yesterday and fell back to the 1.34 handle when a No-deal became clear.

And now, with the British papers slamming the government, the pound seems to take another drop, reaching 1.3430. The Irish government insists that the agreement is here to stay and they are not budging. It is hard to be optimistic at this moment. In addition, this is not the only sticking point: the divorce bill and citizens’ rights (including the Tory taboo of the ECJ) are not 100% resolved.

Support awaits at 1.3420, followed by 1.3340. Even lower, we find 1.3270 and 1.3220. Above 1.3550, high resistance is at 1.3615.

Will the pound extend its falls? We still have the services PMI coming up later today, but any Brexit news will likely have the upper hand.