The British pound’s woes continue as GBP/USD, shed another 300 points for the second week running. The pair closed at 1.5162. This week’s major events include GDP and Manufacturing PMI. Here is an outlook of the events and an updated technical analysis for GBP/USD.

The markets continue to be concerned about the UK economy, which recorded a decline in Q4 of 2012. As well, the Bank of England released a pessimistic Inflation Report, waring that inflation will be above the central bank’s target of 2.0% until 2015. The pound took another jab on Friday, as the Moody’s rating agency downgraded the UK credit rating to AA1 from AAA.

Updates: The pound continues to struggle following the Moody’s downgrade of UK debt. The credit agency reduced the UK by one notch, from Aa1 to Aaa. The downgrade underscores the market’s concern about the health of the British economy. BBA Mortgage Approvals came in at 32.3 thousand, well below the estimate of 34.2K. Chancellor George Osborne spoke in the House of Commons, trying to reassure the markets about the UK economy. BOE Governor Mervyn King spoke in Tokyo. Members of the MPC testified before Parliament’s Treasury Committee. CBI Realized Sales looked awful, coming in at 8 points. This was way below the forecast of 15. Corporate Profits will be released later on Tuesday. BOE Executive Director Paul Fisher will deliver remarks in Bristol. GBP/USD was trading at 1.5146. MPC Member Paul Fisher spoke at the University of Bristol. BOE Deputy Governor Charles Bean delivered remarks at an economic conference in London. Preliminary GDP declined 0.3%, matching the forecast. Preliminary Business Investment dropped 1.2%, surprising the markets, which had anticipated a robust gain of 2.2%. Index of Services declined 0.1%. The estimate stood at 0.1%. GfK Consumer Confidence came in at -26 points, matching the estimate. Manufacturing PMI, a key release, will be published on Friday. GBP/USD was trading at 1.5176.

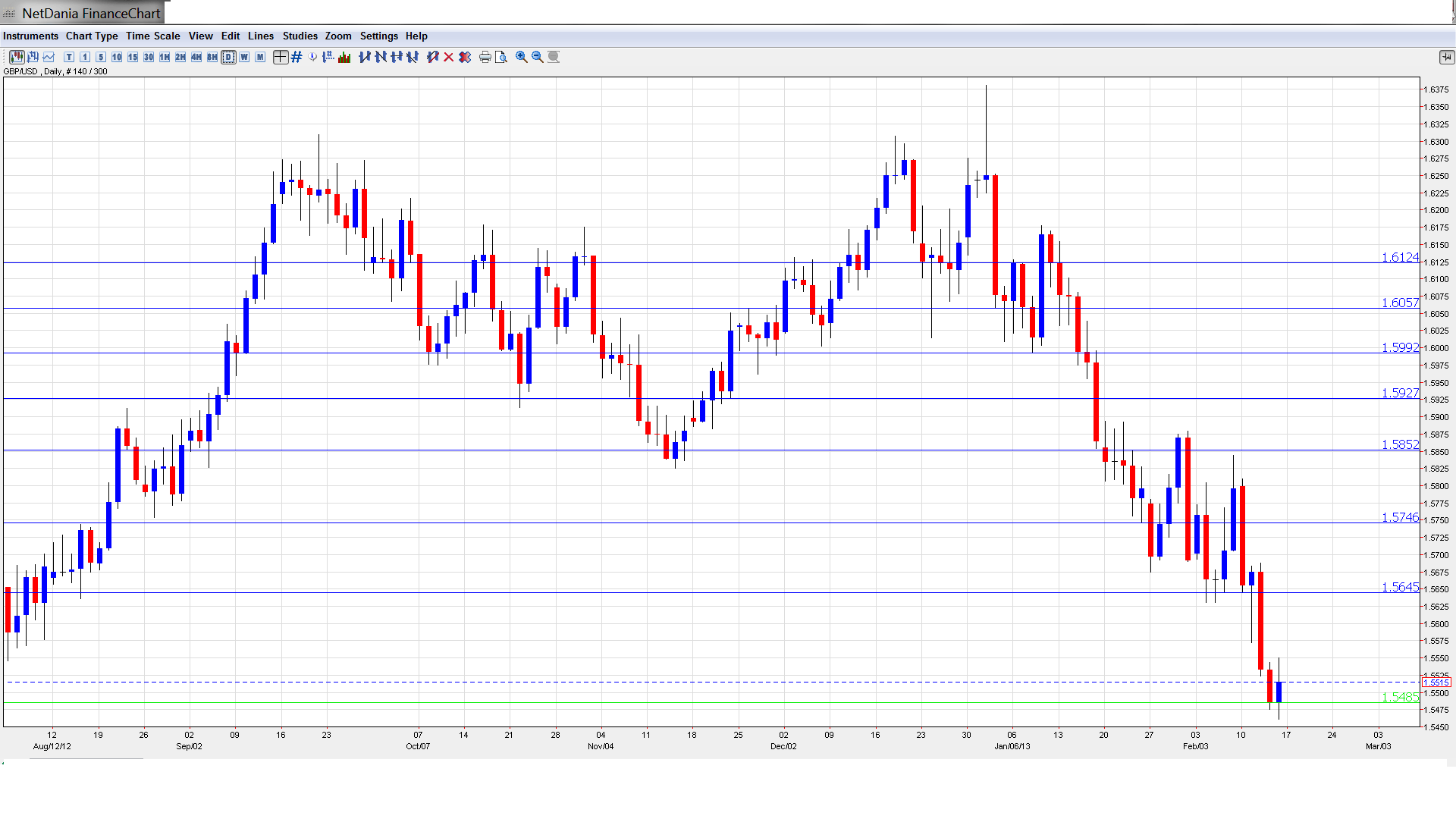

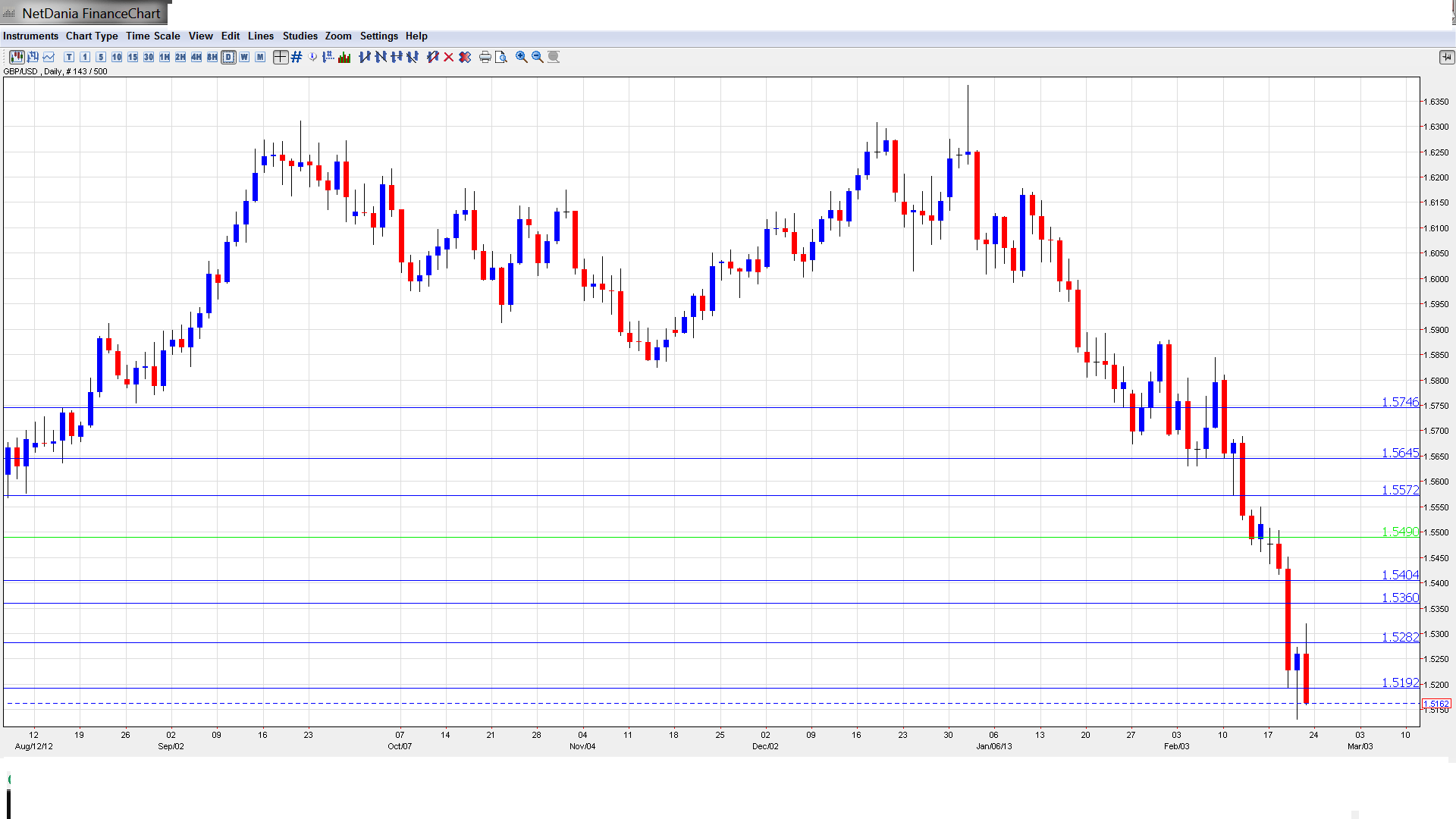

GBP/USD graph with support and resistance lines on it. Click to enlarge:

- BBA Mortgage Approvals: Monday, 9:30. Mortgage Approvals is a leading indicator of housing demand, since most homes are purchased with a mortgage. The indicator has been fairly steady in recent releases, and posted identical readings of 33.6 thousand over the past two months. The markets are expecting a slight improvement in February, with an estimate of 34.2 thousand.

- BOE Deputy Governor Charles Bean Speaks: Tuesday, 10:00. The Deputy Governor will be testifying along with other MPC members in front of Parliament’s Treasury Committee in London. Anlaysts will be looking for clues regarding the BOE’s future monetary policy.

- CBI Realized Sales: Tuesday, 11:00. This index is based on a survey of wholesalers and retailers. It is an leading indicator of consumer spending in the UK. The index has been fairly steady over the past couple of months, pointing to higher sales volume. Little change is anticipated in the February release.

- BOE Executive Director Paul Fisher Speaks: Tuesday, 18:30. Fisher will be speaking at the University of Bristol in London. Analysts monitor public appearances by members of the BOE, looking for any hints as to steps the central bank may consider taking with regard to interest rates or inflation.

- BOE Deputy Governor Charles Bean Speaks: Wednesday, 9:20. The Deputy Governor will be speaking at an economics conference in London. Analysts will be looking for clues regarding the BOE’s future monetary policy.

- Second Estimate GDP: Wednesday, 9:30. GDP is one of the most important fundamental releases, and often affects the movement of GDP/USD. After posting a string of declines, the indicator improved nicely in Q3 of 2012, posting a respectable gain of 1.0%. However, the markets are bracing for a weak reading in Q4, with an estimate of -0.3%. Will the indicator surprise the markets and post another gain?

- Preliminary Business Investment: Wednesday, 9:30. This indicator, released each quarter, has shown a lot of volatility in recent releases. The Q4 for 2012 reading was excellent, with a gain of 3.7%. The markets are expecting a more modest incease for Q1, with a forecast of 2.2%.

- GfK Consumer Confidence: Thursday, 00:01. Analysts are always interested in consumer confidence, as increased positive sentiment translates into more consumer spending, which is an important engine for economic growth. The indicator has been mired in a deep-freeze, pointing to ongoing pessimism about the state of the British economy. The markets are expecting more of the same in the upcoming reading.

- Nationwide HPI: Friday, 7:00. This housing inflation indicator is released early in the month, and provides analysts with a snapshot of activity in the UK housing sector. The index posted a respectable gain of 0.5% in January. The markets are expecting a smaller gain in February, with an estimate of 0.2%.

- Manufacturing PMI: Friday, 9:30. One of this week’s major releases, Manufacturing PMI should always be treated as a market-mover, as an unexpected reading can quickly affect the movement of GDP/USD. This PMI has managed to pull above the 50 level for the past two releases, indicating slight expansion in the British manufacturing industry. The markets are expecting another release in positive territory, with a forecast of 51.0 points.

- Net Lending to Individuals: Friday, 9:30. This indicator measures the change in new credit issued to consumers. There has been a lot of press in the UK about weak borrowing conditions, but the previous reading showed a strong improvement, climbing to 1.7 billion pounds. Increased debt levels are an important indicator of economic growth, as they point to the readiness of financial institutions to lend, as well as consumers feeling comfortable in spending. The markets are expecting another respectable release in February, with an estimate of 1.1 billion.

GBP/USD Technical Analysis

GBP/USD opened the week at 1.5476. The pair touched a high of 1.5508, but it was all downhill for the rest of the week. The pair dropped all the way to 1.5131, crashing through support at 1.5189 (discussed last week). The pair recovered slightly, closing at 1.5162.

Technical lines from top to bottom:

With the pound dropping sharply, we again start from lower levels. We start with resistance at 1.5750. This line saw a lot of activity in the first half of February, before the pound began its recent slump. This is followed by resistance at 1.5648. We next encounter resistance at 1.5567. This line last saw activity in mid-February. Below, there is resistance at 1.5484.

Moving lower, we encounter support at 1.5406, which had held firm since July 2012, before the pair broke past it this week. Next, 1.5361 has reverted to a resistance role, after providing support since last June. The next line of resistance is at 1.5282. This is followed by 1.5189, which had remained intact as a support level since July 2010. It is now providing weak resistance.

GBP/USD is receiving support at 1.5061. This followed by 1.5010, which is protecting the psychologically significant level of 1.50. Next, there is support at 1.4896, just below the round number of 1.49. We next encounter support at 1.4765, which has remained intact since June 2010. This is followed by support at 1.4665. The final support line for now is at 1.4540.

I remain bearish on GBP/USD.

The pound has proved no match for the US dollar and has lost a staggering 11 cents since the beginning of the year. The UK economy continues to stumble, and a credit rating downgrade last week has only worsened matters. The pound has not been able to stem the steep decline, and we could see the downward momentum continue into next week.

Further reading:

- For a broad view of all the week’s major events worldwide, read the USD outlook.

- For EUR/USD, check out the Euro to Dollar forecast.

- For the Japanese yen, read the USD/JPY forecast.

- For the Australian dollar (Aussie), check out the AUD to USD forecast.

- For USD/CAD (loonie), check out the Canadian dollar forecast