USD/JPY lost some value but the 100 level is proving to be a magnate. The team at Credit Agricole marks a very specific date for the pair to move big, and explains:

Here is their view, courtesy of eFXnews:

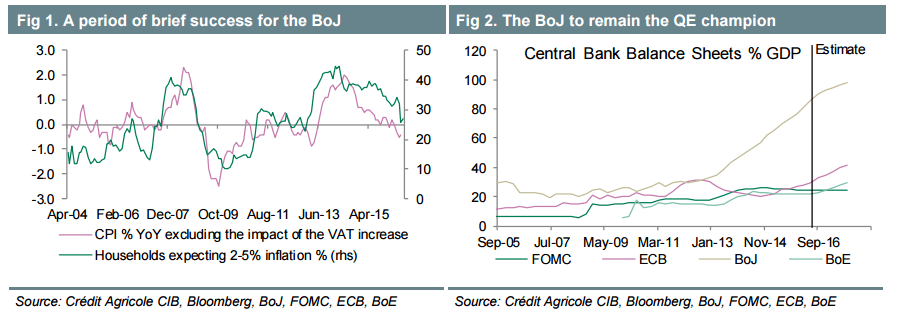

When the BoJ started Quantitative and Qualitative Easing (QQE), the Governor, Haruhiko Kuroda, said that the BoJ would achieve its 2% inflation target by doubling the size of its balance sheet. Currently the BoJ has nearly tripled its balance sheet, however YoY CPI inflation is at -0.4% (where it was when QQE started) after having briefly reached 2% excluding the impact of the VAT increase.

The BoJ is also arguably close to reaching the limits of its QQE. Crédit Agricole CIB’s Japan economist, Kazuhiko Ogata, estimates that at its current rate of asset purchases the BoJ will own over half of the outstanding JGBs by end FY17 and all of the ETFs in about a year. So it is little wonder that the BoJ will be announcing the results of a policy rethink on 21 September, which will be a big event for the JPY, even putting aside any potential action by the FOMC later that same day.

Ogata is doubtful of the Board’s willingness to expand asset purchases into the realm of individual equities (in proportion to their market capitalization, for example) or any form of ‘helicopter money’. Indeed, post its monetary policy review on 20-21 September,our Japan economist expects the BoJ to announce a gradual tapering of its annual expansion of the monetary base from JPY80trn to JPY40trn, to be reduced by JPY10trn per meeting between now and January next year . One of the reasons given for this action, according to Ogata, is so that the BoJ can lengthen the period of its easing process.

Would tapering be positive or negative for USD/JPY?

It is worth noting at this point that a tapering of asset purchases by the BoJ would not be a tightening in monetary policy, as the BoJ’s balance sheet would still be expanding, just at a slower pace. Indeed, the BoJ would remain the QE champion amongst major Central Banks (Figure 2). So while the knee-jerk reaction by investors to a decision by the BoJ to taper would be to buy the JPY, we think that in the medium-term, the direction of the JPY will be determined more by the FOMC than the BoJ. History provides examples of the impact on USD/JPY of both BoJ and FOMC tapering of asset purchases. The BoJ undertook a ‘hard tapering’ of its QE when it reduced the size of its balance sheet after pioneering QE in the early 2000s. However, this hard tapering had little impact on USD/JPY as the FOMC was raising interest rates at the same time . So at least part of the BoJ’s decision on 21 September will be impacted by what it thinks the FOMC will do.

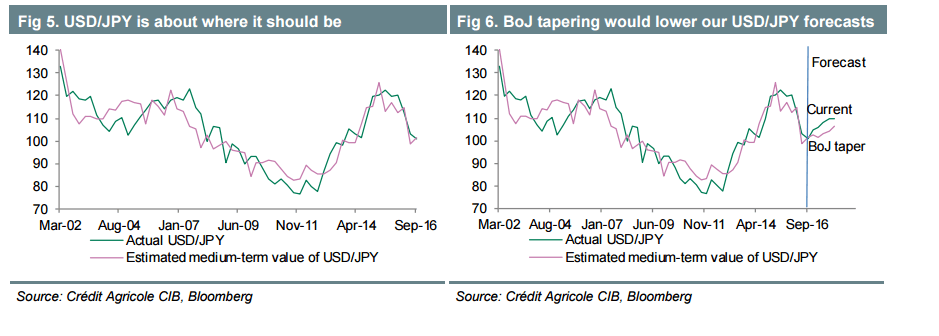

….Using our model, we estimate that a tapering of asset purchases by the BoJ of the magnitude forecast by Ogata would lower our USD/JPY projections by 2.5- 5% over the coming year, but the USD/JPY’s upward track would remain. Rescuing the USD/JPY from a large decline is our US Rates Strategist’s, David Keeble, forecast for about 50bp widening in the US-Japan 10Y interest rate differential over the coming year, which is in line with Crédit Agricole CIB’s forecast for the three 25bp rate hikes forecast by the FOMC over the coming year including a 25bp rate hike in December 2016. We also note that while the BoJ’s balance sheet would be expanding at a slower pace, it would still be expanding relative to a stable FOMC balance sheet and the model interprets this as a positive for the USD/JPY.

For lots more FX trades from major banks, sign up to eFXplus

By signing up to eFXplus via the link above, you are directly supporting Forex Crunch.