Idea of the Day

We wrote yesterday about the obsession with central banks and how this may impact FX, but it’s not always obvious. Six months ago, investors were convinced that the dollar was going to rise because of tapering. Meanwhile both the ECB and Bank of England issued specific forward guidance to kill any doubts about rates remaining low and in turn seen keeping their currencies weaker against the dollar. It could not have gone more wrong, with sterling of the strongest performing currencies in the second half and the euro being one the strongest performers in the last quarter, even though the ECB cut rates and the Fed started tapering asset purchases. In FX, as in many other areas, you have to be careful what you wish for.

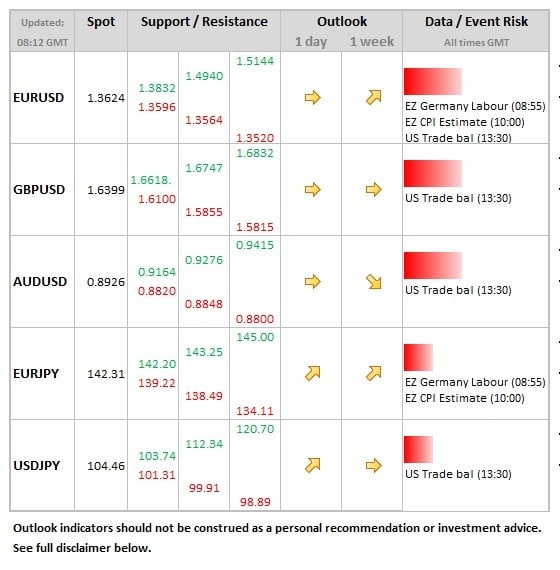

Data/Event Risks

EUR: The Eurozone ‘flash’ estimate of inflation two months ago was one of the factors that pushed the European Central Bank into cutting rates, but as we’ve said before that did not prove to be a factor which has pushed down the euro. Data seen falling from 0.9% to 0.8%. What is problematic for the ECB are the negative inflation rates prevailing in many peripheral countries. So a weaker number could weigh on the euro ahead of Thursday’s ECB meeting.

Latest FX News

EUR: The single currency has been dragging its feet a little so far this year, which should not surprise given the extent of the gains going into the end of 2013 and the fact that some of this was based on temporary year end factors.

AUD: The link between what goes on in China and the Aussie is a lot weaker than it once was, but they have far from de-coupled. China starts the year with continued concerns regarding credit and the Aussie is not immune to such concerns. The Aussie moved towards the 0.89 level yesterday, but remains devoid of strong fundamental influences for now.

Gold: Continues to be well supported in the early part of the year, thanks to reports of decent physical demand from Asia. Sentiment matters in gold, so the fact that it’s got off to a decent start to the year is more notable than for other asset markets, especially after last year’s losses.

Further reading:

Webinar today: 2014 outlook – a guide to currency movements

Exciting week ahead after holiday season