No big surprises in the UK inflation report: CPI m/m is down 0.1% as expected, year over year it is 0.6%, 0.1% above expectations and core CPI is at 1.3%, as expected. But PPI data is higher: PPI Input jumped 3.3% instead of 0.6% predicted. PPI Output is up 0.3% as predicted and the Retail Price Index (RPI) is up 1.9%, higher than 1.7% predicted.

So, if producer prices are rising, will it reach consumer prices? At the moment, we do not see this. Nevertheless, GBP/USD is up some 40 pips, extending the rise that began earlier. All in all, the pair is now enjoying a range of 100 pips.

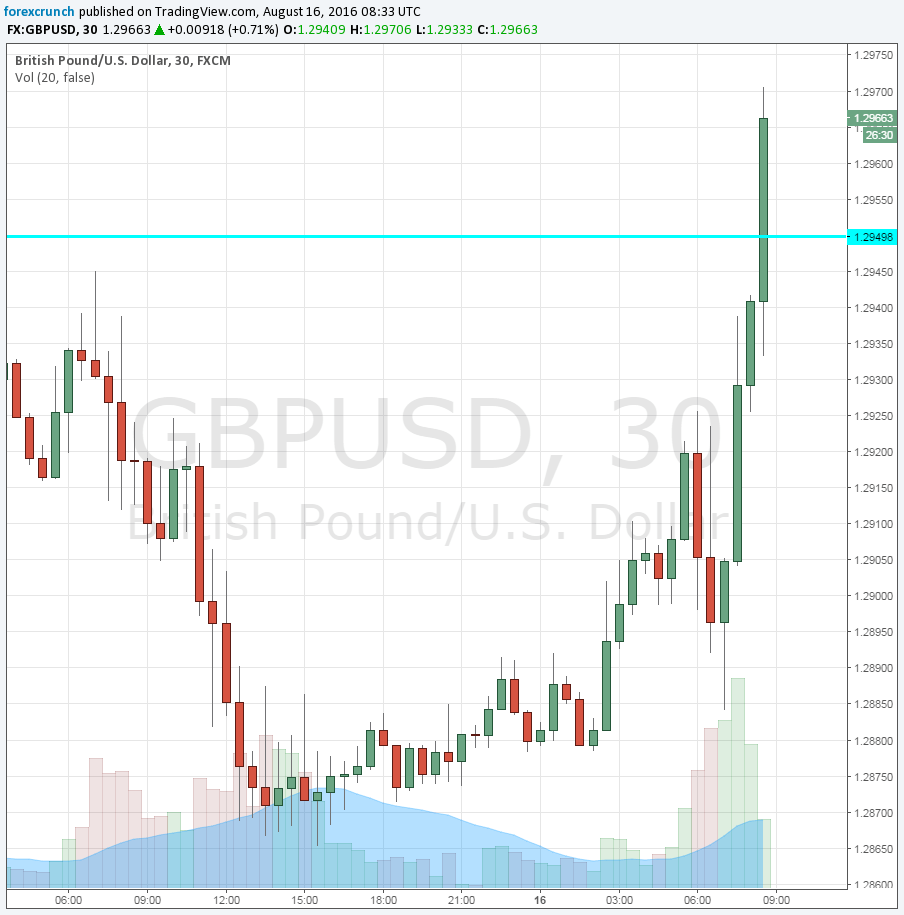

Can GBP/USD break above 1.30?

The rise in PPI is the highest in around two years. Higher inflation could slow down the pace of stimulus from the central bank, potentially holding back the bank in its expected rate hike in November. However, Carney already said that inflation that is the result of the weaker pound will be seen as transitory.

The UK was expected to report an annual increase of 0.5% in the headline Consumer Price Index year over year in July. Month over month, a drop of 0.1% was predicted. This is the first full month after the historic Brexit vote. Some suspect that prices will rise at a quicker pace due to to the fall of the exchange rate. However, changes don’t occur that quickly in developed economies. Core CPI was expected to rise 1.3% y/y after 1.4% beforehand.

GBP/USD was bouncing higher before the release, recapturing the 1.29 level it slipped under yesterday. 1.2930 was the pre-release level.

The Bank of England hit the pound hard with its comprehensive stimulus package. Tomorrow we will get the jobs report from the UK. This consists of both data for July and from June so that it could be somewhat confusing. Perhaps the biggest test of all comes on Thursday with the retail sales report. This will show how consumers actually reacted to the vote.

More: Textbook-like GBP weakness – Morgan Stanley.