Idea of the Day

As the US has moved towards and now through a partial shutdown of the government, the dollar has fought a losing battle. In the prior debt ceiling crisis of August 2011 there was a strong tendency for the dollar to appreciate as the risk-off/safe haven angle dominated. Not so this time (see yesterday’s blog “Does the dollar care?” for more). The Swissie, yen, euro and sterling have all been outperforming the dollar, with the latter two doing so against forces that would have normally pushed them lower. The fact that markets are putting the dollar’s liquidity and supposed safety second to its budgetary risks is not that surprising (given there is also an impending debt ceiling deadline in around 2 weeks) but may also be a good thing if it spurs politicians into action. But we may need to see more of it for that to happen.

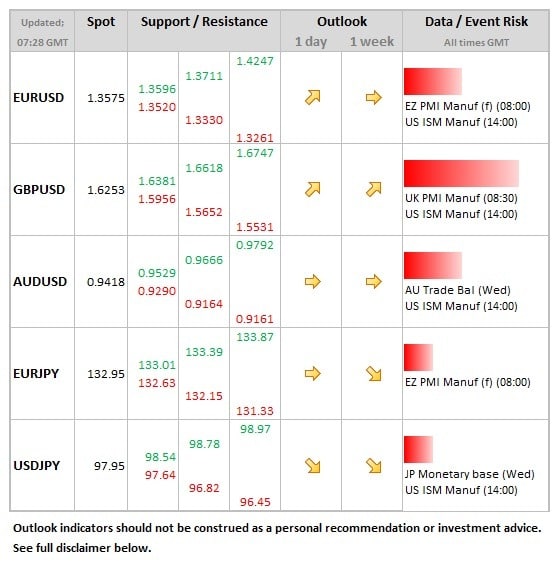

Data/Event Risks

EUR: Final manufacturing data could impact the euro if revisions are seen but only limited risk of this

GBP: The manufacturing PMI data has been moving ever higher recently and is expected to do so again today, from 57.2 to 57.5. The potential for big upward surprise is more limited now the series has recovered so strongly. If weaker, sterling would fall but should find decent underlying support from global factors.

Latest FX News

GBP: Cable reaching a near 10 month high of 1.6247 as the dollar retreated on the back budget deadline developments. We noted in our blog yesterday how sterling was one of the currencies benefitting from the budget rated dollar wobbles. EURGBP modestly lower over the past 24 hours to 0.83440.

JPY: The Tankan survey is a key release for Japan, gauging sentiment across a broad range of industries. The measure for big manufactures rose from 4 to 12, the highest seen for nearly 5 years. USDJPY pushed up to an overnight high of 98.73 but the yen subsequently recovered as safe haven sentiment took over. No surprise with Abe’s announcement of sales tax increase for April next year, with fiscal package to cushion the impact..

AUD: No surprise to see the RBA keeping rates steady at 2.50% overnight. The language of their statement changed last month to indicate that the potential for future rate cuts was less. This and the combination of slightly firmer retail sales (rising 0.4%) allowed the Aussie to push up from 0.9340 to 0.9400.

Further reading:

US government closed for business – 4 implications – USD crashing