The US dollar is looking for a new direction after the first few turbulent weeks in office for Donald Trump. What’s next?

Here is their view, courtesy of eFXnews:

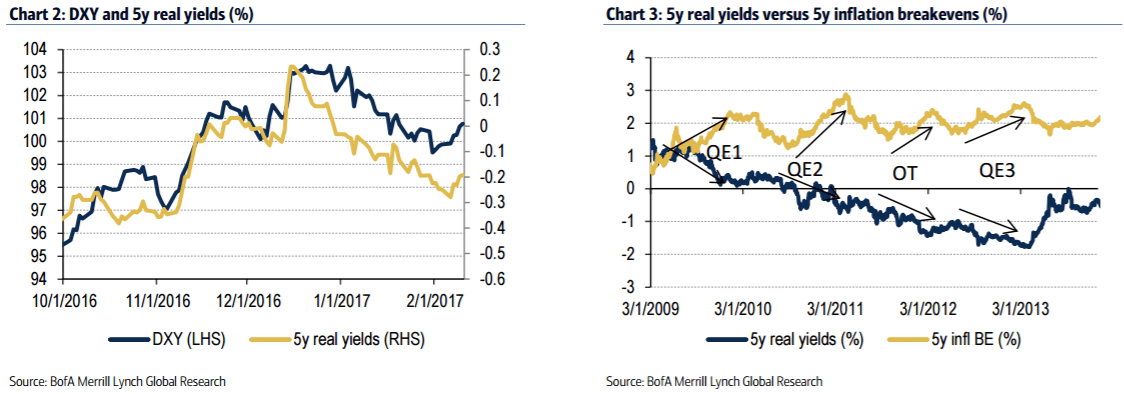

Concerns over stagflation return: In our view, the most interesting and important development in the global financial market so far this year has been the divergence between rising US inflation breakevens and falling US real yields. Rightly or wrongly, investors appear to have become concerned about upside risk to inflation and downside risk to growth.

The Trump risk premium: Informal surveys of our clients suggest that stagflation concerns are being fed by growing pessimism about the new Trump administration. Investors seem to think that potential trade wars and a border adjustment tax (BAT) would boost inflation while repealing Obamacare and the controversy regarding the BAT could delay the highly anticipated tax reform.

Perception versus reality: In this report, we argue why the Trump risk premium may be too high. The administration’s dealing with both China and Mexico in recent weeks suggests to us that the near-term risk of open trade wars has abated. We are also less concerned that Obamacare will take precedence over tax reform. Most crucially, we think the overall tax reform is less dependent on the BAT than usually thought. Our scenario analysis shows that what has been getting priced into the market since January (higher inflation, lower USD) may be actually the least likely path for the BAT. In more plausible scenarios, the USD does quite well and inflation breakevens should be either unchanged or lower.

For lots more FX trades from major banks, sign up to eFXplus

By signing up to eFXplus via the link above, you are directly supporting Forex Crunch.

How to trade it? We could get details on the tax reform as early as the new president’s speech to joint session of Congress on February 28, 2017. We think this could validate our view of a stronger USD.

We think the market is underpricing the risk of a Fed hike in March and better-thanexpected results by the Freedom Party in the Dutch election could intensify concerns of a second-round Le Pen win in May. The latter suggests that over the next 2-3 months it may be easier to buy the USD than to pay US rates and easier to sell EUR/USD than to buy USD/JPY*.

BofA maintains a long USD/JPY position in its portfolio targeting 120.