Draghi didn’t deliver: The president of the European Central Bank created huge expectations for further easing and delivered very very little. This caused a massive rally in EUR/USD, lifting it around 400 pips in a dramatic day that will be remembered for a long time.

Here are 10 points on this huge move. Will it extend further or will we see a reversal?

- Preliminary fake disappointment: The Financial Times mistakenly reported a “no change” outcome for rates. It may have well been a fat finger and the story was retracted quickly. The result was an initial rise in EUR/USD that was quickly followed by a dip, but it had its impact on the news, creating an atmosphere of disappointment, even if it was a wrong report.

- Small cut: The negative deposit was cut by 10 basis points to -0.30%. This was the minimum of expectations, especially with two other European countries already presenting a rate of -0.75%. In addition, the interest rate was the path of least resistance in political terms: less German resistance.

- No new QE: From 60 billion euros per month, the ECB was expected to move to 75 billion or more. The minimum of expectations was 70 billion. And yet we had nothing. That was the biggest blow.

- New stuff on the shopping list priced in: The ECB will now also buy municipal ones but that was already priced in, and in any case, not that necessary with no new monthly buys. Going into corporate bonds would be a more far-reaching step.

- Limited extension of QE: This was supposed to be the easier part of QE: it’s forward guidance and not a commitment for imminent action. Draghi could have announced QE-Infinity, like in the US. The 6 month extension also seemed quite minimal.

- Re-investing proceeds ignored by markets: When a bond matures, the ECB commits to buy another bond instead. Draghi and his colleagues thought that this would be a substitute to more QE, as it implies buying more bonds and committing to a higher balance sheet, just like the Fed. It also implies a program lasting longer. However, it is currently hard to assess the impact and this is by no means a long term move. The markets could still change their minds about this, but it will take quite a lot of time.

- More later?: In October, Draghi opened the door to lowering the deposit rate after having said it had reached its lower bound beforehand. And now, there was no such commitment, meaning the ECB can still do more. This triggered a small sell off, but very short lived and actually a buy opportunity. But after failing to meet expectations and also refraining from the use of “vigilance”, Draghi’s words are certainly less powerful.

- Lower forecasts: The ECB staff projections published every quarter, showed lower inflation expectations for 2016, contrary to reports about leaving them unchanged. So, if this is all the ECB does when it lowers its own forecasts, there is little room for more if these modest forecasts are realized.

- Short squeeze: Once the expectations weren’t met, this triggered a massive short covering that just exacerbated the move. Also the sell off in bonds and stocks contributed to a darker mood.

- Swiss support?: The Swiss National Bank has intervened in the past and pledged to work in currency markets to weaken the franc. The euro, which is the currency in all the countries around Switzerland, was the primary target. They may have joined the bandwagon, buying euros to push EUR/CHF even higher, also pushing EUR/USD higher on the way.

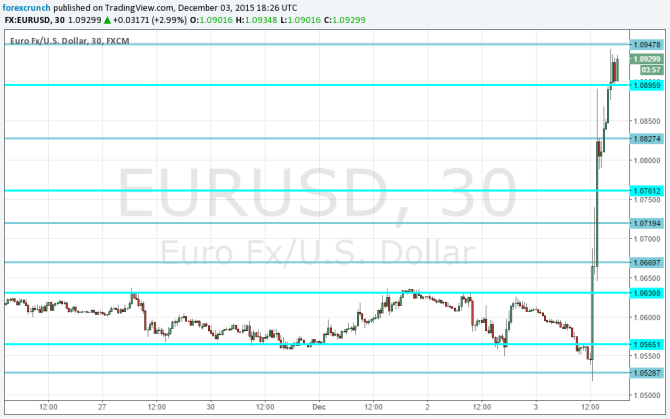

From levels of 1.0540 before the news and 1.0520 during the messy trading, EUR/USD trades at 1.0924 at the time of writing after having reached a high of 1.0942.

A move you don’t see every day:

And the week isn’t over: see how to trade the Non-Farm Payrolls with EUR/USD