- AIG Manufacturing Index: Sunday, 21:30. The index slipped to 51.1 in October, which points to stagnation in the manufacturing sector. No significant movement is likely in the November release.

- MI Inflation Gauge: Monday, 0:00. This indicator is released on a monthly basis and mimics the quarterly CPI release. Inflation has been at low levels, as the MI gauge has posted two straight gains of 0.1%.

- Building Approvals: Monday, 0:30. This key construction indicator bounced back with a gain of 7.6% in September, after two straight declines. The strong reading marked a 7-month high. Investors are braced for a decline of 1.0% in October.

- Company Operating Profits: Monday, 0:30. Business profits jumped 4.5% in Q2, crushing the estimate of 2.1%. This was the strongest gain since Q1 of 2018. A gain of 1.0% is expected in the Q3 release.

- Chinese Caixin Manufacturing PMI: Monday, 1:45. The manufacturing sector has been hit hard by the trade war with the U.S, but the Caixin PMI has managed to stay just above the 50-line since September, which points to stagnation. The index came in at 51.7 in October and the estimate for 51.5 stands at 51.7 pts.

- Current Account: Tuesday, 0:30. After a string of deficits, Australia produced a current account surplus in Q2, with a reading of $A5.9 billion. This easily beat the estimate of $A1.5 billion. The forecast for the third quarter stands at A$6.1 billion.

- RBA Rate Decision: Tuesday, 3:30. The RBA lowered the benchmark rate to 0.75% in October and is expected to maintain this level at the upcoming meeting. The tone of the rate statement could have a significant impact on the movement of the Aussie.

- AIG Services Index: Tuesday, 21:30. The index improved to 54.2 in October, pointing to expansion in the services sector. This was the index’s highest level since November 2018.

- GDP: Wednesday, 0:30. GDP is one of the most important economic indicators should be treated as a market-mover. In Q2, GDP improved to 0.5%, up from 0.4% in Q1. An identical figure is projected for the Q3 release.

- Retail Sales: Thursday, 0:30. Retail sales is the primary gauge of consumer spending. The indicator dropped to 0.4% in September, down from 0.2% a month earlier. The October estimate stands at 0.3%.

- Trade Balance: Thursday, 0:30. Australia continues to record trade surpluses. The surplus widened to A$7.18 billion in September, well above the forecast of A$5.10 billion in the previous release. Analysts expect the trade surplus to widen in October, with a forecast of A$6.50 billion.

- AIG Construction Index: Thursday, 21:30. The construction sector continues to contract, as the index remains mired below the 50-level, which separates contraction from expansion. In October, the index showed some improvement, rising to 43.9 pts. The upcoming release will likely remain deep in contraction territory.

*All times are GMT

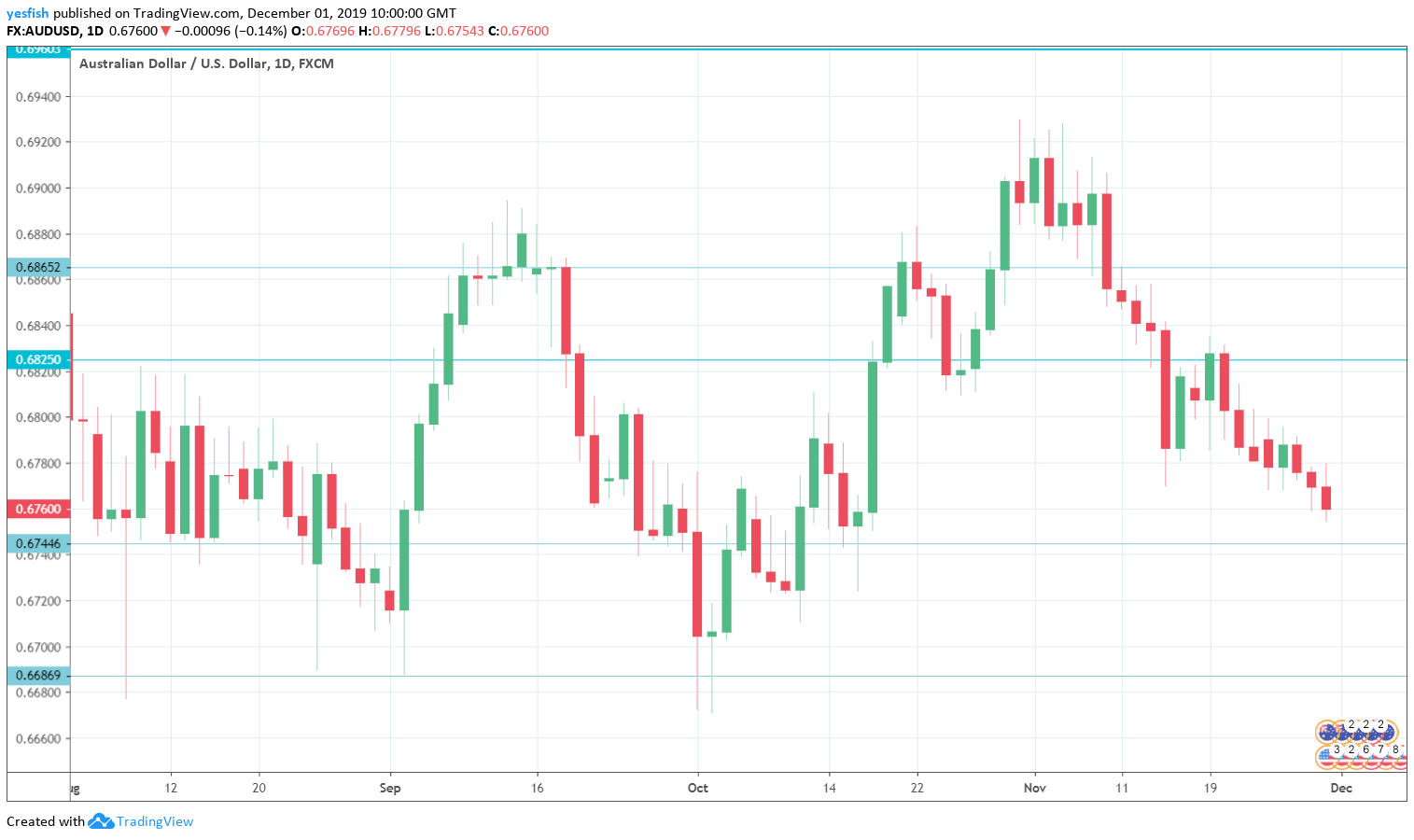

Technical lines from top to bottom:

0.7165 has held firm since early April.

0.7085 has held since July. This is followed by 0.7022.

0.6960 is protecting the symbolic 70 level.

0.6865 (mentioned last week) is next.

0.6744 is an immediate support level.

0.6686 was tested in early November.

0.6627 has held in support since March 2009. This is followed by 0.6532.

0.6456 is the final support level for now.

.

I remain bearish on AUD/USD

The rash of rate cuts earlier in the year have not yet trickled down and boosted the Australian economy, leaving consumers and the business sector apprehensive. A trade deal between the U.S. and China remains elusive, which is weighing on investor risk appetite and making the Aussie less attractive to investors.

Follow us on Sticher or iTunes

Further reading:

- EUR/USD forecast – for everything related to the euro.

- GBP/USD forecast – Pound/dollar predictions

- USD/JPY forecast – projections for dollar/yen

- USD/CAD forecast – Canadian dollar analysis

- Forex weekly forecast – Outlook for the major events of the week.

Safe trading!