Idea of the Day

The deal was done late yesterday, ending the US government shutdown and extending the debt ceiling to the early part of next year. For the dollar, it’s been very much a case of “buy the rumour, sell the fact”, most evident on USDJPY over the past 24 hours, where the gains seen in the run-up have mostly been eroded during the Asia session. Estimates suggest a 0.3-0.4% hit to annual GDP. Tapering from the Fed is now looking unlikely for this year, but a further downgrade of the US credit rating is looking more likely and not only from Fitch who have put their AAA rating under review. The uncertainty could weight on the dollar further in the bigger picture, the dollar positive arguments that have struggled to assert themselves in the second half of this year (tapering, relative growth differentials) having faded further.

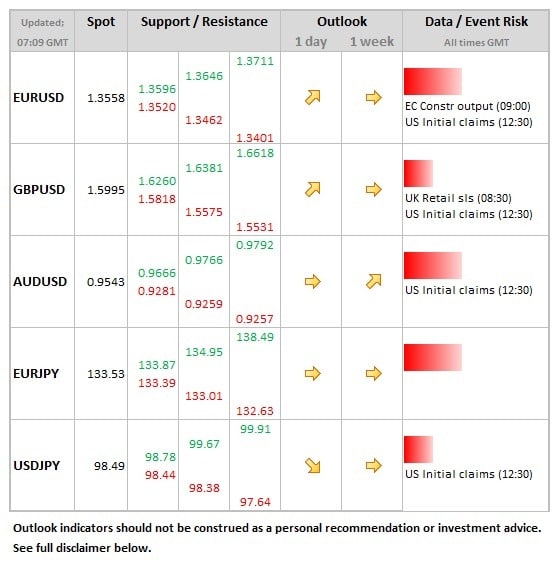

Data/Event Risks

GBP: The last of the key data releases this week is retail sales today. The market looks for a small recovery from the 1.0% MoM decline seen in the previous month. Sterling could do with some better than expected data to allow for a more concerted push above the 1.60 level on cable.

USD: Just claims data today, but even that is riddled with uncertainties and distortions owing the government shut-down, meaning that the moment the dollar is not sure what to think even in relation to the current state of the economy, let alone the future outlook.

Latest FX News

EUR: The week’s high of 1.3598 taken out in early European trade, as the dollar looks tired. US downgrade chatter also supporting the move.

AUD: Probing new territory overnight, but also looking a little tired with it, AUDUSD having risen for the past 6 consecutive sessions.

GBP: The labour market data showed some mixed messages, so sterling struggled for a sustained push above the 1.60 level against the US dollar.

Further reading:

US government open for business for the next 3 months – huge damage done